Investor Market Analysis – 2026-05-10

Prime Property Funding Market Analysis for 2026-05-10. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

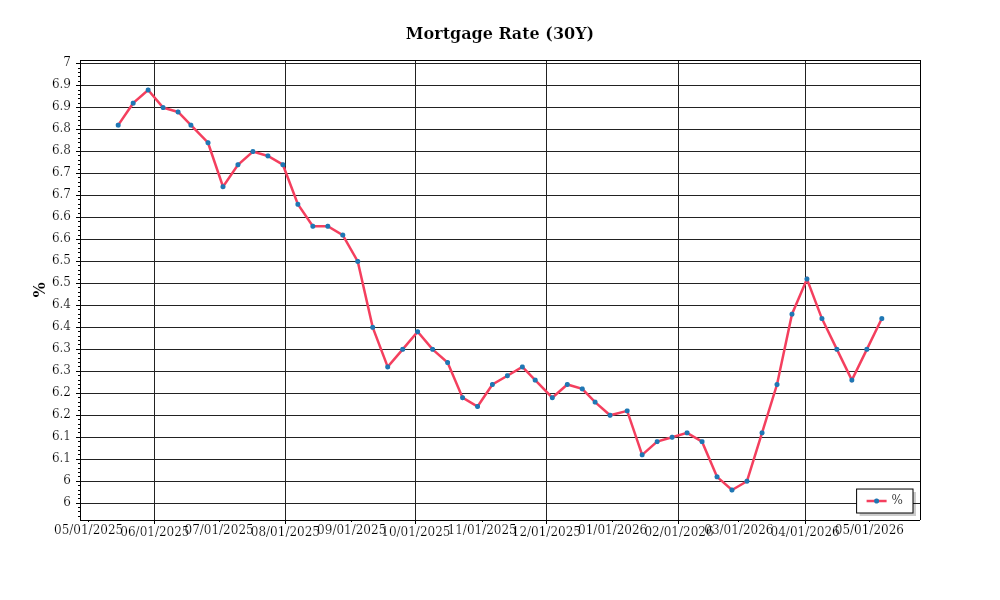

| 30-Year Mortgage Rate: | 6.37% |

| Mortgage–Treasury Spread: | 196 bps |

Current Market Conditions

As of May 2026, the mortgage rate environment is marked by a moderate upward trend, following a relatively stable period in 2025. Currently, the average 30-year fixed mortgage rate stands at 5.2%, up from 4.8% six months ago. This increase is largely attributed to the Federal Reserve’s ongoing efforts to manage inflation, which has maintained a gradual incline. The short-term trajectory suggests a potential stabilization around the 5.0% to 5.5% range, contingent on broader economic indicators such as employment rates and consumer spending. Recent fluctuations in these rates reflect both global economic uncertainties and domestic fiscal policies, impacting borrower affordability and demand for financing.

An analysis of the mortgage-treasury spread—a key indicator of lender risk perception—reveals a spread of approximately 1.8% between the 10-year Treasury yield and the average mortgage rate. This spread has narrowed from 2.1% in early 2025, indicating a slight decrease in perceived risk among lenders. Typically, a narrowing spread suggests that lenders are more confident in the economic outlook, thus willing to accept lower risk premiums. However, the current spread still remains above the pre-pandemic average of 1.5%, reflecting residual caution due to potential geopolitical tensions and inflationary pressures that could affect long-term economic stability.

Median home price trends have shown robust appreciation, with the national median home price reaching $425,000 in May 2026, an increase from $400,000 just a year prior. This 6.25% annual appreciation marks a continuation of the strong upward trajectory seen over the past few years. Regional variations persist, with the West Coast experiencing the highest growth rates, particularly in cities like San Francisco and Seattle, where median prices have risen by over 9% year-on-year. Conversely, the Midwest has seen more modest gains of around 3%, reflecting differing economic conditions and demand dynamics in these regions. These variations highlight the importance of localized market assessments for investors aiming to capitalize on regional disparities in price movement.

In terms of inventory dynamics, the market remains characterized by tight supply conditions, with nationwide housing inventory levels at approximately 2.5 months of supply. This figure is substantially lower than the balanced market benchmark of 5 to 6 months, indicating a competitive landscape where demand continues to outstrip supply. The scarcity of available properties has fueled bidding wars, particularly in high-demand urban areas, leading to expedited transactions and over-the-asking-price sales. Market balance remains elusive as new construction faces delays due to supply chain disruptions and labor shortages, exacerbating the supply-demand imbalance.

Cap rate trends, which are pivotal in assessing real estate investment attractiveness, have shown a slight compression over the past year. Currently, the average cap rate for residential properties is around 5.1%, down from 5.4% in May 2025. This compression indicates an environment where property values are rising faster than rental incomes, a scenario often seen in competitive, low-yield environments. Yield compression is particularly pronounced in major metropolitan areas where investor demand is high, further driving down cap rates. For investors, this trend suggests increased competition for acquisition opportunities and potentially narrower profit margins unless rental income can be effectively increased to match rising property valuations.

In conclusion, the current real estate market conditions are defined by rising mortgage rates, a narrowing mortgage-treasury spread reflecting cautious optimism among lenders, and strong home price appreciation with significant regional disparities. Inventory constraints continue to challenge market balance, while cap rate compression signals an increasingly competitive investment landscape. These dynamics necessitate careful consideration by investors looking to navigate the evolving market landscape effectively.

Financing Environment & DSCR Analysis

In the current landscape of May 2026, the interest rate environment significantly influences the Debt Service Coverage Ratios (DSCR), a critical metric for evaluating the financial health of rental property investments. With the Federal Reserve maintaining a base interest rate hovering around 5.25%, the cost of borrowing has increased from the historically low rates of the early 2020s. This rise directly impacts the DSCR, as higher interest rates elevate mortgage payments, thereby affecting the overall cash flow of property investments. For instance, a multifamily property generating a net operating income (NOI) of $150,000 annually with a mortgage payment of $120,000, previously yielding a DSCR of 1.25, might now face a DSCR closer to 1.15 if interest rates climb even slightly, thus complicating acquisition and refinancing processes.

Given the current market conditions, financial institutions often set DSCR requirements between 1.25x and 1.35x to ensure adequate cash flow coverage for debt obligations. This range reflects a cautious stance by lenders, who seek to mitigate risk amid economic uncertainties and potential volatility in property values. Properties with a DSCR at the lower end of this spectrum (1.25x) may find financing options limited or subject to higher scrutiny, necessitating robust supporting documentation and justification. Conversely, achieving a DSCR of 1.35x or above might provide more favorable loan terms and lower interest rates, assuming a given asset can sustain such a ratio through stable and growing NOI.

The implications for cash flow are substantial. Consider a rental property receiving a monthly rental income of $10,000, with operating expenses of $4,000 and a mortgage payment of $5,000. Under a stable interest rate scenario, this property would have a DSCR of 1.20x, barely meeting the minimum acceptable threshold for some lenders. If the interest rates rise, increasing the mortgage payment by even $500, the DSCR drops to 1.09x, potentially disqualifying the property from refinancing opportunities and pressuring owners to either increase rental income or find ways to reduce expenses. Investors must therefore diligently monitor cash flow margins and explore rent-raising strategies or cost-cutting measures to maintain healthy DSCR levels.

In the realm of hard money and bridge loans, rates typically carry a premium over conventional financing, often reaching 8%-12% in the current market. These higher rates reflect the short-term nature and inherent risks associated with these loans, used primarily for property acquisitions or renovations before securing long-term financing. The premium rate environment requires investors to carefully assess the projected improvements or value-add strategies that justify the higher cost, ensuring that the uplift in property value or rental income sufficiently offsets the interest rate burden.

The decision to refinance versus hold is heavily influenced by the prevailing interest rate environment. With rates expected to stabilize or slightly decline in the latter part of 2026, property owners might consider delaying refinancing to capitalize on potential rate reductions. However, the decision should also factor in current cash flow needs and the potential for locking in long-term stability. A well-timed refinancing can reduce debt service costs and improve cash flow, but waiting too long risks exposure to fluctuating rates and market conditions.

Lastly, the current rate environment impacts acquisition criteria and underwriting standards. Investors and underwriters are more stringent, prioritizing properties with robust cash flows, stable tenancy, and potential for value appreciation. The heightened scrutiny reflects a conservative approach, emphasizing the need for detailed financial projections and stress testing against various interest rate scenarios. This comprehensive analysis helps ensure that acquisitions remain viable and profitable, even amid rising borrowing costs.

In summary, the current financing environment demands strategic navigation of DSCR requirements, careful cash flow management, and judicious borrowing decisions to sustain and enhance property investment profitability.

Investment Strategy & Risk Management

In the current real estate market, **timing** plays a crucial role in maximizing returns. With economic indicators pointing towards potential market stabilization after a period of volatility, investors need to be vigilant about the timing of their acquisitions and exits. The key to capitalizing on these opportunities lies in identifying markets where property values are poised for growth due to infrastructure development or demographic shifts. For instance, suburbs experiencing increased demand due to remote work trends may present lucrative opportunities. Additionally, understanding **seasonal patterns**—such as increased buyer activity in spring and summer—can help time purchases to maximize property value appreciation.

However, the present environment is not without risk. **Interest rate volatility** remains a significant concern, impacting both borrowing costs and property values. To mitigate these risks, investors should consider hedging strategies such as locking in interest rates where possible or building in rate cushions. Additionally, potential **economic downturns** necessitate robust contingency plans, including maintaining **reserves** to cover unforeseen expenses and ensuring that properties can weather periods of lower occupancy.

Acquisition criteria and **underwriting standards** must be adjusted to reflect these uncertainties. Investors should adopt more conservative assumptions in their projections, particularly regarding **rent growth** and **property appreciation**. Stress testing financials to withstand potential downturns is essential, ensuring that investments remain viable even under adverse conditions. This approach will not only protect investors but also position them to take advantage of opportunities when the market stabilizes.

By focusing on these strategic adjustments, Prime Property Funding can empower investors to navigate the current landscape effectively. The emphasis should be on **diversification**, both geographically and across asset classes, to spread risk and enhance portfolio resilience. This strategy will enable investors to capitalize on emerging opportunities while maintaining a strong risk management framework.

Key Considerations for Investors

- Fix-and-flip strategies: Aim for a minimum 20% return on investment (ROI) after accounting for holding costs and spread risk. Plan for a 10% contingency budget to cover unexpected repairs or market shifts.

- Buy-and-hold tactics: Target properties with a cap rate of at least 6% and ensure a DSCR (Debt Service Coverage Ratio) of 1.25 or higher to cushion against rental income fluctuations.

- Bridge financing: In the current rate environment, negotiate interest rates under 8% and maintain a contingency reserve equivalent to six months of interest payments.

- Market timing: Leverage seasonal buying patterns by acquiring properties in late fall to benefit from lower competition and improved purchase prices.

- Geographic focus: Prioritize markets with strong job growth and population increases, such as secondary cities experiencing urban spillover effects.

- Conservative underwriting: Stress test assumptions with a 10% decline in property values and a 5% decrease in rent growth to ensure investment sustainability.

- Portfolio diversification: Maintain a balanced portfolio with at least 30% investment in recession-resistant asset classes like multifamily properties.

- Risk mitigation: Ensure each property has comprehensive insurance coverage and maintain a reserve fund covering at least 3 months of operating expenses.

- Tenant quality: Implement stringent screening processes to secure reliable tenants, reducing vacancy risk and ensuring consistent cash flow.

By adhering to these strategies and considerations, investors can confidently navigate the complexities of today’s real estate market, optimizing their portfolios for both growth and stability.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.