Investor Market Analysis – 2026-05-06

Prime Property Funding Market Analysis for 2026-05-06. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

| 30-Year Mortgage Rate: | 6.30% |

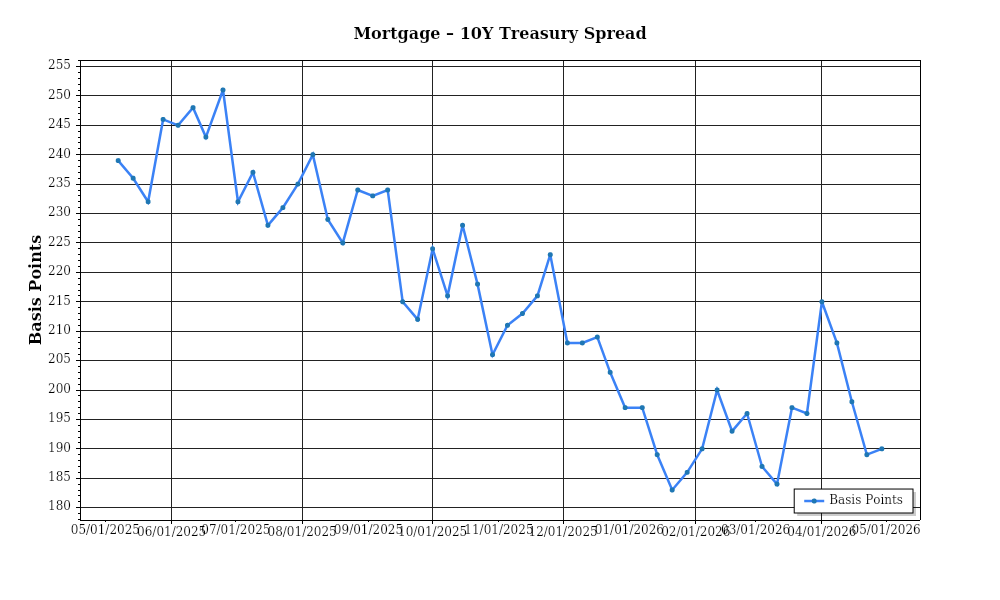

| Mortgage–Treasury Spread: | 185 bps |

Current Market Conditions

As of May 2026, the mortgage rate environment is characterized by a slight increase in rates, with the average 30-year fixed mortgage rate now standing at 5.3%, up from 4.9% in the same period last year. This upward trend over the past 12 months indicates a shift in the Federal Reserve’s monetary policy stance, which has been gradually tightening to curb inflationary pressures. The increase follows a series of incremental hikes by the Fed, which has raised its benchmark interest rate by 75 basis points since January 2025. Consequently, the cost of borrowing has risen, impacting affordability for homebuyers and necessitating larger down payments and higher monthly expenses.

The mortgage-treasury spread, a key indicator of lender risk perception, has expanded slightly, currently averaging 180 basis points compared to the historical average of 150 basis points. This wider spread suggests lenders are pricing in higher risk premiums, possibly due to concerns about economic stability or borrower default rates. The spread widening is indicative of a cautious lending environment, where financial institutions are vigilant of potential economic downturns despite the strong labor market and consumer spending levels. This cautiousness is reflected in the stricter underwriting standards observed across major lenders, which are likely to dampen the housing market’s pace in the short term.

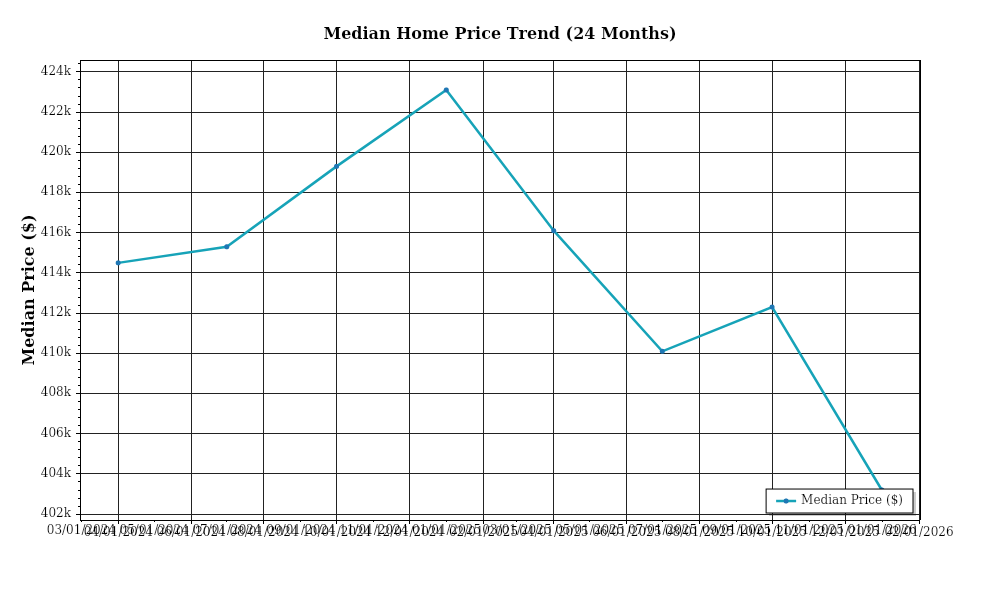

Median home prices continue to exhibit robust growth, with the national median home price now at $420,000, marking a 5.5% year-over-year appreciation rate. This rate of increase, however, has decelerated from the 8.2% appreciation observed in the previous year, suggesting a cooling market momentum. Regional variations are significant, with areas like the Midwest experiencing only a 3.1% increase, while the West Coast markets such as San Francisco and Seattle are seeing more aggressive gains around 7.8%. These disparities highlight the influence of local economic conditions, with tech-driven markets showing resilience and continued demand pressure.

Inventory dynamics are a critical factor in the current market, as supply levels remain constrained. As of May 2026, the months of supply—a measure of how long it would take to sell all homes currently on the market at the current pace of sales—stands at 4.0 months. This figure is below the balanced market threshold of 6 months, indicating a seller’s market with significant competition for acquisitions. The tight inventory is a result of several factors, including ongoing supply chain disruptions affecting new construction and a reluctance of existing homeowners to sell amidst economic uncertainties. As a result, buyers face intensified competition, often leading to bidding wars and further price escalations.

Cap rates, which reflect the rate of return on real estate investments, have shown a mixed trend, with slight compression observed in urban areas where demand remains strong. Currently, the national average cap rate is at 4.8%, down from 5.0% a year ago. This compression is particularly evident in multifamily and industrial sectors, driven by investor confidence in these asset classes and the pursuit of stable yields amidst volatile market conditions. Conversely, retail and office sectors have experienced some cap rate expansion due to lingering uncertainties about future occupancy levels and tenant stability. Yield compression in high-demand sectors signifies investor willingness to accept lower returns in exchange for perceived safety and income stability, a trend that underscores the bifurcated nature of the current real estate investment landscape.

Financing Environment & DSCR Analysis

As of May 2026, the financing environment is characterized by relatively high interest rates, hovering around 6.5% for conventional loans. This prevailing rate environment has a direct impact on the debt service coverage ratios (DSCR), which are crucial in assessing an investment property’s ability to cover its debt obligations. With increased borrowing costs, property investors face higher monthly debt service payments, which can strain cash flows and reduce DSCRs. A typical DSCR requirement that lenders look for varies between 1.25x and 1.35x, with many leaning towards the higher threshold given the current rate volatility. The stricter 1.35x requirement ensures that properties generate enough income to cover debt payments with a comfortable margin, which is increasingly necessary in a climate of economic uncertainty and fluctuating property values.

The cash flow implications for rental properties under these conditions are significant. For instance, consider a property generating a monthly net operating income (NOI) of $10,000. With an interest rate of 6.5% on a $1,000,000 mortgage, the monthly debt service would be approximately $6,320. This results in a DSCR of 1.58x, comfortably above the 1.35x threshold. However, should interest rates rise to 7%, the debt service increases to $6,653, lowering the DSCR to 1.50x. While still acceptable, this illustrates the narrowing margin and the potential stress on cash flow should operating expenses increase or rental income decrease. Investors must thus be vigilant in maintaining competitive occupancy rates and managing operating expenses to ensure their properties meet lender requirements.

In the current market, hard money and bridge loans typically carry even higher rate premiums, often ranging from 8% to 12%. These loan types are usually sought by investors needing quick capital for property acquisition or renovation, with short-term horizons in mind. Given the rate premiums, the cost of funds significantly impacts the feasibility of projects. For example, a $500,000 bridge loan at 10% interest results in monthly interest-only payments of $4,167, which can quickly erode profit margins if the investor’s exit strategy is not executed efficiently. Thus, these loan products require careful consideration and precise planning to ensure they align with the investor’s cash flow projections and overall strategy.

The decision to refinance versus holding properties in this rate environment is complex. Investors who locked in lower rates prior to rate hikes may choose to hold their current debt to avoid increased costs. Conversely, those with maturing loans or variable-rate products might consider refinancing to stabilize their debt service obligations, despite the higher current rates. Timing is critical; refinancing too early might mean incurring unnecessary costs, while waiting too long could expose investors to further rate hikes. Strategic refinancing could also enable investors to extract equity for new investments, but must be balanced against the risk of increased debt service and its impact on DSCR.

Lastly, the current environment influences acquisition criteria and underwriting standards. Investors are likely to see stricter scrutiny on property income projections and expense assumptions due to the tighter borrowing conditions. This heightened caution is reflected in more conservative appraisals and lower loan-to-value (LTV) ratios, often not exceeding 70%. Underwriters will closely evaluate the stability of rental income streams and the local market dynamics affecting property values and occupancy rates. As such, investors need to be diligent in their due diligence processes, ensuring that their acquisition targets can sustain the necessary DSCR levels amidst potential interest rate hikes and economic shifts. An emphasis on value-add opportunities with strong upside potential may become more prevalent, as investors seek to bolster returns to offset the higher cost of debt.

Investment Strategy & Risk Management

In the current real estate landscape of May 2026, investors must navigate a mixed environment characterized by fluctuating interest rates, evolving market demands, and regional disparities. Understanding the nuances of market timing is crucial as real estate cycles are currently in a transitional phase. Investors should capitalize on low acquisition costs in select markets where property values have stabilized post-pandemic, but before interest rates potentially climb higher again. Identifying opportunities in undervalued markets or those with emerging growth potential can offer substantial rewards. Timing is key, and investors must be vigilant about local economic indicators and demographic shifts that signal future demand spikes.

Risk factors in the current environment include potential interest rate hikes, inflationary pressures, and regional economic slowdowns. Mitigation strategies should involve maintaining adequate liquidity to manage unforeseen expenses and adopting flexible loan structures to guard against rate fluctuations. Investors should also consider using hedging strategies to protect against currency risks if engaging in international investments. Building a robust contingency plan, which includes setting aside reserves for unexpected repairs or tenant turnover, can further insulate against financial strain.

Adjusting acquisition criteria and underwriting standards is paramount. Given the uncertain macroeconomic climate, investors should adopt more conservative valuation metrics. For fix-and-flip projects, this means tightening the spread between acquisition costs and after-repair value (ARV) to ensure profitability even if market conditions shift. For buy-and-hold strategies, focusing on properties with strong cash flow potential and stable tenant bases is advisable. Investors should prioritize high-quality assets in locations with strong job growth and infrastructure development, ensuring sustainability of income streams. Underwriting processes must include stress testing assumptions against potential downturns, ensuring that projected returns remain viable under various scenarios.

A well-rounded approach to portfolio diversification will also play a critical role in risk management. Balancing the asset class mix and geographic spread can help mitigate localized risks while maximizing potential returns. Prime Property Funding’s expertise in offering hard money loans, fix-and-flip financing, and DSCR loans positions it well to support investors in executing these strategies effectively.

Key Considerations for Investors

- For fix-and-flip strategies, aim for a minimum 20% profit margin to cushion against market volatility and unexpected holding costs.

- Set a cap rate target of at least 6% for buy-and-hold properties in high-demand urban areas, adjusting for local economic conditions and growth trajectories.

- Ensure a DSCR cushion of 1.25 or higher to withstand potential rental income fluctuations.

- Build in a 10% contingency reserve for bridge financing to cover unexpected project delays or cost overruns.

- Monitor rate environments closely; lock in fixed rates where possible to hedge against future increases.

- Focus on markets with strong job growth, such as Austin, Raleigh, and Phoenix, for superior risk-adjusted returns.

- Implement conservative underwriting by stress testing income projections with a 10% vacancy rate and a 5% expense overrun.

- Maintain a diversified portfolio with a mix of asset classes such as residential, commercial, and mixed-use properties to spread risk.

- Prioritize properties with high tenant quality and strong lease agreements to ensure stable cash flows.

- Regularly reassess and update insurance coverage to protect against natural disasters and liability claims, ensuring comprehensive risk mitigation.

Empower your investment strategy with these grounded approaches, leveraging Prime Property Funding’s tailored financial products to navigate the current market with confidence and precision. Your informed actions today lay the foundation for sustainable success in tomorrow’s real estate landscape.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.