Investor Market Analysis – 2026-05-05

Prime Property Funding Market Analysis for 2026-05-05. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

| 30-Year Mortgage Rate: | 6.30% |

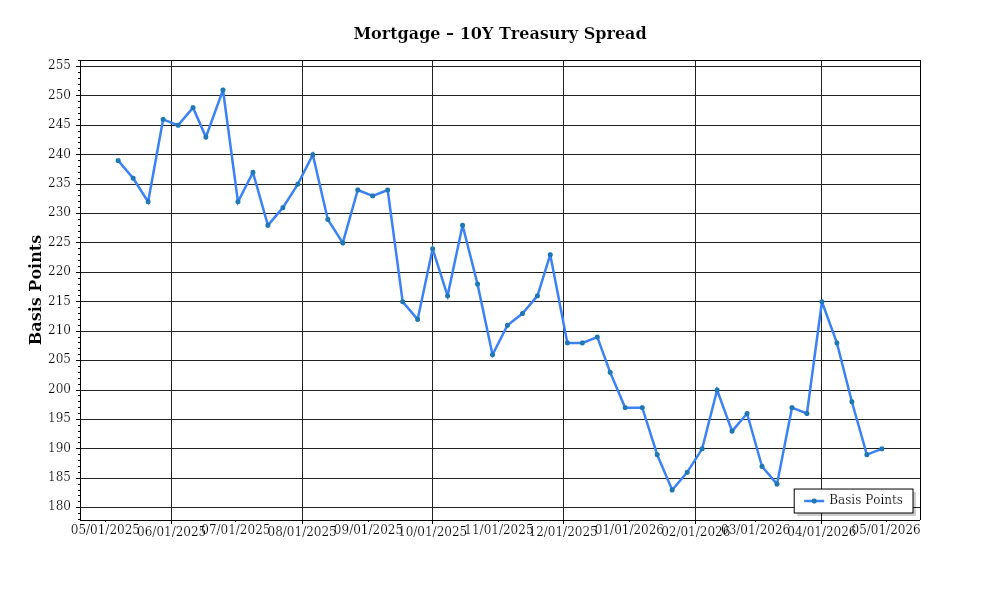

| Mortgage–Treasury Spread: | 191 bps |

Current Market Conditions

As of May 2026, the mortgage rate environment is characterized by a modest yet steady increase in rates. Currently, the average 30-year fixed mortgage rate stands at 6.2%, up from 5.7% in October 2023. This uptick reflects a gradual tightening by the Federal Reserve, aimed at curbing inflationary pressures while maintaining economic stability. The Federal Reserve’s consistent policy adjustments over the past 30 months have been mirrored in the mortgage rates, with a notable impact on home affordability and buyer sentiment. Recent trends indicate that while the pace of rate increases has slowed, the trajectory remains upward, suggesting that potential homebuyers and investors may face higher financing costs in the near term. This environment poses significant implications for market dynamics, particularly affecting first-time buyers and those leveraging variable rate mortgages.

The mortgage-treasury spread, which is the difference between mortgage rates and the yield on 10-year Treasury bonds, currently stands at 1.8%. This spread, slightly above the historical average of roughly 1.5%, signals heightened lender risk perception. Typically, a wider spread suggests that lenders are factoring in greater uncertainty or risk, potentially due to economic volatility or concerns about borrower defaults. The current spread reflects a cautious outlook by lenders amidst economic adjustments and geopolitical uncertainties influencing global markets. This elevated spread, combined with the rising mortgage rates, indicates that lenders are maintaining stringent credit standards, which could moderate buyer activity and influence housing demand.

In terms of home prices, the median home price as of May 2026 is approximately $429,000, marking a 5.2% increase year-over-year. This appreciation rate, although robust, is a deceleration from the double-digit growth observed in the immediate aftermath of the pandemic-induced housing boom. Regional variations are notable, with the Southeast and Southwest regions experiencing higher than average appreciation rates of 6.8% and 7.1%, respectively, driven by strong demographic shifts and economic growth. In contrast, the Midwest and Northeast have seen more modest increases of 3.4% and 4.0%, reflecting slower economic recovery and demographic stability. These trends highlight a continued demand-supply imbalance, particularly in high-growth areas, underscoring the importance of regional analysis for investment strategies.

Inventory dynamics also play a crucial role in shaping current market conditions. As of May 2026, the housing inventory remains tight, with a supply level of approximately 2.9 months, well below the balanced market benchmark of 6 months. This low inventory level indicates intense competition for available homes, exacerbated by supply chain disruptions and labor shortages that have hampered new construction. The scarcity of housing options, especially in urban and rapidly growing suburban areas, has contributed to sustained upward pressure on prices and has intensified competition among buyers. This environment presents challenges for homebuyers but also suggests potential opportunities for investors in new construction and renovation projects.

Cap rate trends in the real estate market are also crucial indicators of current conditions. Nationally, the average cap rate has compressed slightly to 5.5%, down from 5.8% a year ago. This compression reflects strong demand for real estate assets, particularly in sectors like multifamily and industrial properties, which continue to attract significant investment capital. Yield compression is indicative of investor confidence in long-term real estate fundamentals and the pursuit of stable income-generating assets amidst volatile financial markets. However, this trend also suggests that investors may face challenges in achieving desired returns, necessitating careful analysis and strategic asset selection. As cap rates continue to compress, investors may need to adjust their expectations and explore value-added opportunities to enhance yields.

Financing Environment & DSCR Analysis

As of May 2026, the financing environment is characterized by relatively high interest rates, which are exerting significant pressure on the Debt Service Coverage Ratios (DSCR) across the real estate market. With the Federal Reserve maintaining a cautious stance and keeping rates elevated to control inflation, borrowing costs for real estate investors have increased substantially. The current average interest rate for commercial real estate loans hovers around 7%, a marked rise from the sub-5% rates seen in the early 2020s. This elevation in rates directly impacts DSCR, a critical metric used by lenders to assess the feasibility of loan repayments relative to the property’s income. Higher interest expenses reduce net operating income (NOI) available for debt service, thereby lowering the DSCR.

In this environment, lenders have adjusted their DSCR requirements to mitigate risk. Typically, a DSCR of 1.25x has been the industry standard; however, with the increased risk of economic fluctuations, many lenders are now demanding a threshold of 1.35x or higher. This shift is particularly impactful for investors, as it requires either a reduction in loan amounts or an increase in property income to meet these heightened criteria. For instance, if a property generates an NOI of $100,000, under a 1.25x DSCR requirement, the maximum allowable annual debt service would be $80,000. With a 1.35x requirement, this drops to approximately $74,074, necessitating either higher down payments or improved operational efficiencies to secure financing.

The implications of these requirements are far-reaching for cash flow of rental properties. Higher DSCR thresholds mean that property owners need to optimize rental income or reduce operating costs to maintain profitability. Consider a rental property with a gross rental income of $150,000 and operating expenses of $50,000, resulting in an NOI of $100,000. With a loan of $900,000 at a 7% interest rate, annual debt payments amount to approximately $75,720, presenting a DSCR of 1.32x—just below the new 1.35x benchmark. This scenario necessitates either renegotiation of rents or cost-cutting measures to align with lender expectations.

In the current market, hard money and bridge loans have emerged as viable, albeit costly, alternatives for investors unable to meet traditional DSCR requirements. These loans typically carry interest rate premiums of 2-4% above conventional mortgage rates, reflecting their short-term nature and higher risk profile. For instance, a bridge loan might come with an interest rate of 9-11%, significantly impacting the cost of capital and necessitating careful consideration of exit strategies to ensure profitability upon stabilization or sale of the asset.

Decisions regarding refinance timing versus hold strategies are pivotal in this rate environment. Investors must weigh the benefits of refinancing at potentially higher rates against the possibility of future rate reductions, which could enhance future cash flows. A strategic hold might be advisable if a property is nearing lease renewals or rental escalations, which could improve DSCR naturally. Conversely, properties with predictable cash flows and low risk of vacancy might benefit from locking in current rates to hedge against further increases.

Finally, the impact of the current rate environment on acquisition criteria and underwriting standards cannot be overstated. Investors are now required to adopt more conservative assumptions in their financial models, often incorporating higher vacancy rates and slower rent growth projections. Underwriting standards have tightened, with increased scrutiny on location quality, tenant creditworthiness, and property condition to mitigate the risk of underperformance. In summary, the prevailing financial conditions necessitate a more rigorous approach to investment analysis, with a significant focus on maintaining robust cash flow to meet the heightened DSCR thresholds and ensure long-term asset stability.

## Investment Strategy & Risk Management

In the current real estate climate, timing is crucial for maximizing returns as the market undergoes shifts influenced by interest rate changes and evolving consumer preferences. Investors should keep a close eye on **interest rate movements** and economic indicators such as employment rates and inflation, which directly impact consumer buying power and borrowing costs. Identifying opportunities in this environment involves looking for distressed properties or areas with recent infrastructure developments, as these can offer undervalued acquisitions. The current market conditions favor those who can act quickly and decisively, leveraging **short-term financing options** to capitalize on price corrections and emerging trends.

Risk factors in this environment include potential changes in interest rates, which could affect both **financing costs** and **property values**. Investors need to adopt robust **risk mitigation strategies**, such as securing rate locks for financing and maintaining liquidity to navigate sudden market shifts. Diversifying geographic focus and asset classes can also help minimize exposure to localized downturns and sector-specific risks. It’s imperative to conduct thorough due diligence and stress-test investment assumptions against adverse scenarios, such as slower-than-expected rent growth or increased vacancy rates.

Adjusting acquisition criteria and underwriting standards is essential to align with the current market dynamics. Investors should prioritize properties with **strong cash flow potential** and conservative leverage ratios. Underwriting standards must incorporate **higher contingency reserves** to account for unexpected increases in holding costs or renovation expenses. Additionally, focusing on properties with **value-add opportunities** can enhance returns even in a flat market by improving asset performance through strategic upgrades and management enhancements.

In conclusion, the key to navigating the current real estate market lies in a balanced approach that embraces strategic flexibility and rigorous risk management. By staying informed and adaptable, investors can seize opportunities and safeguard their portfolios against volatility. Prime Property Funding clients should leverage our expertise in hard money loans, fix-and-flip financing, and DSCR loans to optimize their investment strategies and achieve resilient, sustainable growth.

### Key Considerations for Investors

– **Fix-and-flip strategies:** Aim for a **minimum spread of 20%** between purchase and resale prices to buffer against unexpected costs. Incorporate a **10% contingency** in renovation budgets to account for unforeseen expenses.

– **Buy-and-hold tactics:** Target a **cap rate of at least 6%** to ensure adequate returns in a rising rate environment. Maintain a **DSCR cushion of 1.25x** to withstand rent fluctuations and unexpected vacancies.

– **Bridge financing:** Secure **rate locks** to mitigate the impact of potential interest rate hikes. Design draw schedules that align closely with project milestones to optimize cash flow management.

– **Market timing:** Evaluate **seasonal trends** to identify optimal entry points, focusing on historically slower months for acquisition to reduce competition and holding costs.

– **Geographic focus:** Prioritize markets with **projected job growth over 3%** annually and increasing population trends for better risk-adjusted returns.

– **Conservative underwriting:** Stress test **cash flow assumptions** with a **10% increase in vacancy rates** and **5% increase in operating expenses** to ensure resilience.

– **Portfolio diversification:** Balance asset classes to achieve a mix of **60% residential and 40% commercial** properties, and spread investments across at least **three different geographic regions**.

– **Risk mitigation:** Keep **liquid reserves covering six months** of operating expenses and debt service to manage unexpected downturns. Ensure comprehensive insurance coverage and prioritize properties with **minimal deferred maintenance**.

– **Exit strategies:** Develop multiple exit plans, such as refinancing or transitioning from fix-and-flip to rental, to adapt to changing market conditions and ensure flexibility.

By adhering to these strategies and recommendations, investors can confidently navigate the dynamic real estate landscape, mitigate risks, and capitalize on emerging opportunities.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.