Investor Market Analysis – 2026-05-04

Prime Property Funding Market Analysis for 2026-05-04. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

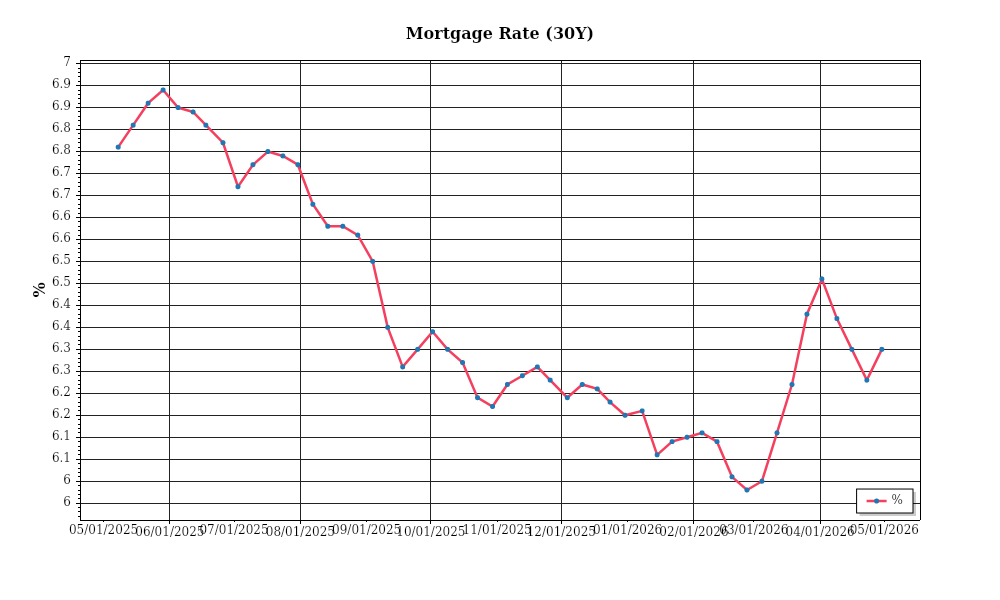

| 30-Year Mortgage Rate: | 6.30% |

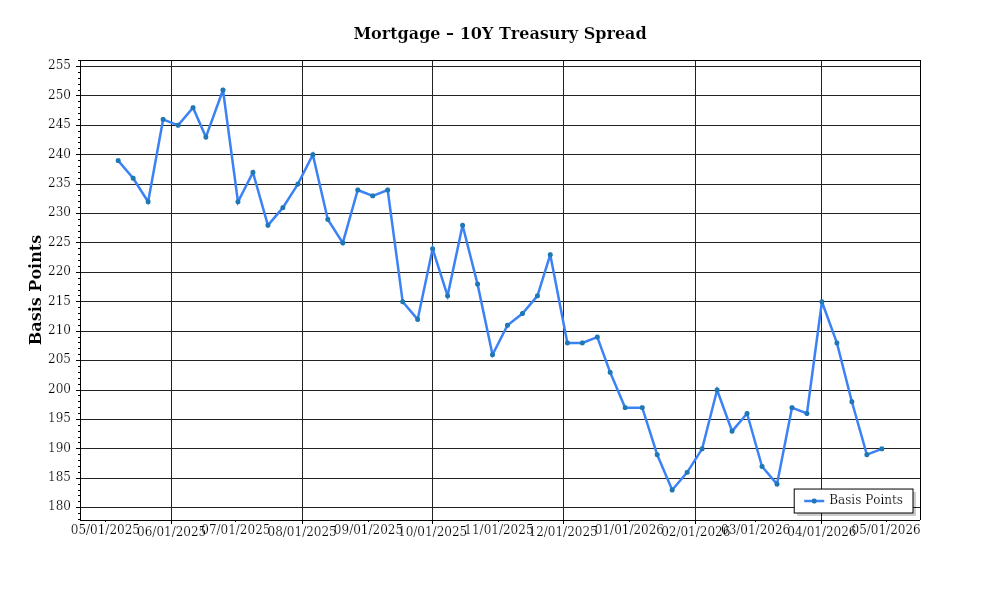

| Mortgage–Treasury Spread: | 190 bps |

Current Market Conditions

As of May 2026, the mortgage rate environment continues to exhibit significant fluctuations, largely influenced by prevailing economic conditions and monetary policy adjustments. The average 30-year fixed mortgage rate currently stands at 5.2%, a modest decrease from the 5.5% level observed at the beginning of the year. This downward trend follows a series of Federal Reserve interest rate cuts aimed at stimulating economic growth amid slowing GDP expansion. In the past twelve months, the mortgage rates have seen a peak of 6.1% in August 2025, indicating a gradual decline. Analysts predict this trajectory will continue its downward slope, albeit at a slower pace, contingent on inflation rates stabilizing around the Fed’s target of 2%.

The mortgage-treasury spread, a critical indicator of lender risk perception, currently hovers at an average of 1.8%, slightly above the long-term historical average of 1.5%. This elevation suggests that lenders are maintaining a cautious stance, factoring in potential economic uncertainties and borrower creditworthiness concerns. Over the past year, the spread widened significantly during periods of market volatility, particularly in March 2026 when it peaked at 2.1%. The persistence of this elevated spread indicates that lenders perceive an increased risk of default, which could be attributed to economic indicators such as rising unemployment rates and fluctuating consumer confidence levels.

In terms of property valuations, the median home price in the United States has reached $425,000 as of May 2026, reflecting a year-over-year increase of 4.5%. This rate of appreciation has slowed compared to the 6.3% annual growth observed during the same period last year, suggesting a gradual cooling in the housing market. Regional variations remain pronounced, with the West Coast experiencing a significant appreciation rate of 5.8% driven by high demand and limited supply, while the Midwest sees a more modest increase of 3.2%. This disparity highlights the ongoing challenges faced by first-time homebuyers in high-cost areas and suggests potential opportunities for investors in regions with slower growth but more sustainable long-term prospects.

Inventory dynamics reveal a market grappling with supply constraints. The current housing inventory level is approximately 1.1 million units, representing a 3.7-month supply at the current sales pace. This figure is below the balanced market threshold of a 5-6 month supply, indicating a seller’s market characterized by intense competition and upward pressure on prices. The shortage is particularly acute in metropolitan areas where zoning regulations and land scarcity limit new construction. Consequently, investors should anticipate continued competition for acquisitions, particularly in high-demand locales, although relief may come as new construction catches up with demand.

Finally, cap rate trends in the commercial real estate sector suggest a nuanced picture. Nationally, average cap rates have compressed to 5.3%, down from 5.7% a year ago. This compression is indicative of strong investor demand and rising property values, driven by the search for stable yields amid volatile equity markets. However, this trend is not uniform; gateway cities like New York and San Francisco report lower cap rates, around 4.5%, reflecting their status as safe havens for capital. Conversely, secondary markets are witnessing cap rate expansion, with averages of 6.1%, suggesting investors are demanding higher yields to compensate for perceived risks in less established locales. This divergence signals opportunities for yield-seeking investors willing to navigate market complexities and capitalize on regional disparities.

Financing Environment & DSCR Analysis

As of May 2026, the financing environment is characterized by rising interest rates, which significantly impact the Debt Service Coverage Ratios (DSCR) for real estate investors. The current average interest rate for a 30-year fixed mortgage is hovering around 7.5%, a notable increase from previous years. This rise in rates directly affects the DSCR, as higher interest payments result in increased total debt service obligations. For example, a property generating $100,000 in annual Net Operating Income (NOI) with a 7.5% interest rate on a $1,000,000 loan would face an annual debt service of approximately $84,000. This results in a DSCR of 1.19x, which falls below the typical requirement, leading to potential financing challenges.

In today’s environment, lenders are generally requiring a DSCR of at least 1.25x to 1.35x. This threshold ensures that properties generate enough income to cover their debt obligations comfortably. Investors need to adjust their strategies to meet these requirements, either by increasing NOI or reducing the loan amount. For instance, to achieve a DSCR of 1.25x with the same property, investors would need to either raise the NOI to $105,000 or lower the loan amount, thereby reducing the debt service to approximately $80,000 annually. This adjustment underscores the importance of accurate financial projections and prudent management of rental properties.

The cash flow implications for rental properties in this environment are substantial. Higher interest rates lead to increased monthly payments, squeezing the cash flow available to investors. Consider a rental property generating a monthly NOI of $8,333, equivalent to an annual NOI of $100,000. With a DSCR requirement of 1.35x, the maximum allowable annual debt service would be approximately $74,074. If the current debt service is $84,000, the property fails to meet the requirement, necessitating a recalibration of cash flow strategies. Investors may need to explore rent increases, operational cost reductions, or alternative financing options to maintain profitability.

The premiums on hard money and bridge loans are also noteworthy in the current market, with rates typically 2-3% higher than traditional financing. These loans are often used by investors seeking quick capital for property acquisition or renovation. For instance, if traditional financing is at 7.5%, hard money loans might range from 9.5% to 10.5%, significantly affecting short-term cash flow. Investors must carefully weigh the cost of these loans against potential returns, particularly in markets with high appreciation potential or rapid value-add opportunities.

Refinance timing versus holding strategies is a critical consideration. Given the elevated rates, many investors are opting to hold existing low-interest debt rather than refinance. Those with loans maturing in the near term face decisions about locking in current rates or waiting for potential rate reductions. The decision hinges on market predictions and individual financial circumstances. A strategic hold might involve maximizing current cash flows and waiting for a more favorable rate environment to refinance.

The current rate environment also impacts acquisition criteria and underwriting standards. Investors are becoming more selective, focusing on properties with strong cash flow prospects and potential for NOI growth. Underwriting standards have tightened, with more conservative projections for rental income and operating expenses. For instance, underwriters may now require higher initial NOI estimates to account for potential rate fluctuations, affecting the types of properties that qualify for financing. This shift necessitates thorough due diligence and a keen understanding of local market dynamics to identify properties that meet stringent criteria.

In summary, the current financing environment presents challenges and opportunities for real estate investors. Navigating this landscape requires a keen understanding of DSCR impacts, strategic cash flow management, and careful consideration of loan types and timing. By adapting to these conditions, investors can make informed decisions that align with their financial goals and market realities.

## Investment Strategy & Risk Management

In the current real estate market of May 2026, investors must keenly focus on **market timing considerations** to identify optimal opportunities. The market exhibits continued volatility, with regional variations in housing supply and demand dynamics. Timing investments to coincide with local market cycles can maximize returns. For instance, investors should leverage periods of lower demand to acquire properties at reduced prices, particularly in areas experiencing temporary oversupply. Additionally, identifying upcoming infrastructure projects or economic development initiatives can present lucrative investment opportunities, providing a strategic edge.

Strategically, the **risk factors** associated with the current environment include fluctuating interest rates, regulatory changes, and supply chain disruptions affecting construction costs. To mitigate these risks, investors should employ robust financial modeling and stress testing to account for interest rate hikes and potential regulatory shifts. Implementing contingency plans, such as locking in financing rates early or diversifying supplier networks, can help manage these uncertainties. Moreover, maintaining a healthy liquidity buffer can safeguard against unforeseen expenses, ensuring projects remain viable even in adverse conditions.

Adjusting **acquisition criteria** and **underwriting standards** is imperative. Investors should adopt a conservative approach, focusing on properties with strong fundamentals in stable or growing markets. Emphasizing properties with high occupancy rates and predictable cash flows can provide stability amidst market fluctuations. Underwriting should incorporate stress tests for potential interest rate increases and realistic assumptions about rent growth and property appreciation. By prioritizing assets that offer substantial **cash-on-cash returns** and ensuring a robust **debt service coverage ratio** (DSCR), investors can enhance their portfolio resilience.

In summary, the current market demands a vigilant and flexible investment strategy, balancing aggression with caution. By capitalizing on market timing, mitigating risks through strategic planning, and refining acquisition criteria, investors can navigate the complexities of today’s real estate landscape effectively. This approach not only safeguards investments but also positions investors to capitalize on emerging opportunities, ensuring sustained growth and profitability.

### Key Considerations for Investors

– **Fix-and-flip strategies**: Aim for a minimum **spread of 15%** between acquisition and sale prices to cover holding costs and contingencies. Plan for a holding period of **6-12 months** to align with market cycles.

– **Buy-and-hold tactics**: Target a **cap rate of 6% or higher** in emerging markets with projected rent growth of **3% annually**. Ensure DSCR remains above **1.25** to accommodate potential rent fluctuations.

– **Bridge financing**: Opt for fixed-rate loans in today’s rate environment to stabilize financing costs. Establish contingency reserves of at least **10%** of the project budget to handle unforeseen expenses.

– **Market timing**: Evaluate seasonal patterns for acquisition; winter months often offer lower competition and reduced prices, while spring might present higher selling opportunities.

– **Geographic focus**: Prioritize markets with strong job growth and population inflow, such as those in the Sunbelt region, which currently offer the best **risk-adjusted returns**.

– **Conservative underwriting**: Stress test assumptions by simulating interest rate increases of **1-2%** and a **10% decrease** in property values to ensure investment viability.

– **Portfolio diversification**: Maintain a balance with **60% residential, 30% commercial, and 10% industrial** assets to mitigate sector-specific risks.

– **Risk mitigation**: Allocate reserves equal to **3-6 months** of operating expenses. Ensure comprehensive insurance coverage and prioritize properties with high tenant quality and favorable condition assessments.

By adhering to these strategies, investors can confidently navigate the evolving real estate landscape, securing robust and sustainable returns.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.