Investor Market Analysis – 2026-05-03

Prime Property Funding Market Analysis for 2026-05-03. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

| 30-Year Mortgage Rate: | 6.30% |

| Mortgage–Treasury Spread: | 190 bps |

Current Market Conditions

The current mortgage rate environment presents a dynamic landscape as of May 2026. The average 30-year fixed mortgage rate stands at 5.1%, reflecting a moderate increase from 4.7% in October 2023. This upward trend is indicative of the Federal Reserve’s monetary policy adjustments aimed at curbing inflation, as well as heightened global economic uncertainties. Over the past six months, rates have ascended gradually, influenced by both domestic inflationary pressures and geopolitical tensions that affect global supply chains. The trajectory suggests that rates may continue to rise slightly as the Federal Reserve maintains its stance on monetary tightening. However, the pace of this increase may decelerate if inflation shows signs of moderation. For investors, this environment necessitates a careful evaluation of financing strategies, as rising rates could impact affordability and demand.

In terms of mortgage-treasury spread analysis, the current spread between the 30-year fixed mortgage rate and the 10-year Treasury yield is approximately 2.2%. This spread has widened from 1.8% in early 2024, reflecting an increased perception of risk on the part of lenders. The spread is a critical indicator of lender sentiment, as a wider spread often signals heightened risk aversion. This change suggests lenders are factoring in greater uncertainties related to borrower default risk or potential market volatility. For investors, a widening spread can imply increasing costs of borrowing and a need to reassess risk-adjusted returns on real estate investments. Lenders’ cautious approach could also lead to tighter lending standards, affecting both purchase and refinancing activities.

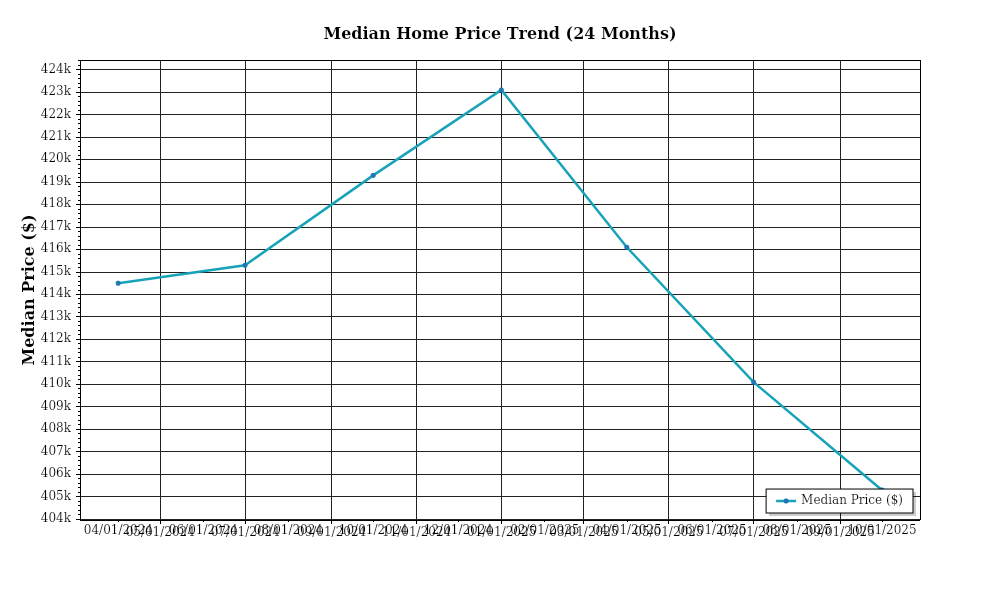

The median home price in the United States has continued its upward trajectory, reaching $437,000 in May 2026, up from $402,000 in October 2023. This represents an annual appreciation rate of approximately 4.5%, a slight deceleration compared to the double-digit growth rates experienced in the early 2020s. Regional variations persist, with the Sun Belt regions, including states like Texas and Florida, seeing higher appreciation rates of up to 6% annually, driven by continued population influx and economic growth. In contrast, some urban centers in the Northeast are experiencing more modest gains, around 2.5%, due to factors such as population stagnation and higher living costs. These trends underscore the importance of geographical diversification for real estate investors seeking to maximize returns.

Inventory dynamics reveal a market still grappling with supply constraints. The current housing inventory is approximately 1.3 million units, down from 1.5 million in the same period last year, resulting in a months’ supply of 2.5 months, well below the balanced market threshold of 6 months. This scarcity is contributing to competitive acquisition conditions, with multiple offers becoming the norm in many desirable areas. The constrained supply is partly due to ongoing supply chain disruptions affecting new construction and a reluctance among existing homeowners to sell, given the rising interest rates. For investors, these inventory dynamics may necessitate a more aggressive acquisition strategy and a focus on under-served markets where competition may be less intense.

Cap rate trends provide further insight into the current market dynamics. As of May 2026, the average cap rate for U.S. commercial real estate is 5.4%, down from 5.8% a year ago, indicating yield compression. This compression is driven by strong investor demand, particularly in sectors like multifamily and industrial properties, where cap rates can be as low as 4.5% in prime locations. The continued compression of cap rates suggests investors are willing to accept lower initial yields in exchange for potential long-term appreciation and income stability. This trend highlights the importance for investors to carefully assess property fundamentals and market conditions to ensure that acquisitions are made at sustainable pricing levels, considering the potential for future cap rate expansion as interest rates rise.

Financing Environment & DSCR Analysis

As of May 2026, the current interest rate environment significantly influences the Debt Service Coverage Ratios (DSCR) for real estate investors. With prevailing mortgage rates hovering around 6.5% for commercial properties, investors are finding it increasingly challenging to maintain favorable DSCR metrics. A higher interest rate increases the cost of borrowing, thereby raising debt servicing costs. This situation necessitates higher income performance from properties to meet or exceed the typical DSCR requirements. For instance, assuming a property generates a net operating income (NOI) of $120,000 annually, a loan with a higher interest rate might require a debt service of $96,000, resulting in a DSCR of 1.25x. This marks the lower threshold in the current environment, just meeting the minimum requirement for many lenders who prefer a DSCR of at least 1.35x to consider a loan less risky.

Given these dynamics, the typical DSCR requirements have shifted slightly. While many lenders previously accepted a minimum DSCR of 1.25x, there is now a growing tendency to require a DSCR of 1.35x or even higher. This stricter requirement reflects lenders’ heightened risk aversion in response to the economic fluctuations and increased costs of capital. Investors must now ensure their properties produce sufficient NOI to cover higher debt service obligations. For example, with the same $120,000 NOI, a 1.35x DSCR would necessitate a debt service of no more than $88,889, which could limit borrowing capacity or necessitate additional equity input to meet financing qualifications.

The implications for cash flow in rental properties are substantial. Higher financing costs and stringent DSCR requirements mean that cash flow margins are under pressure. Investors need to perform meticulous cash flow analysis to ensure that properties can sustain higher debt service costs. For example, if an investor holds a rental property with a gross rental income of $150,000 and operating expenses of $30,000, the NOI stands at $120,000. With debt service at $88,889 for a 1.35x DSCR, the investor retains $31,111 in cash flow. This scenario underscores the importance of maintaining healthy operating efficiencies and possibly adjusting rental rates to enhance revenue and improve cash flow resilience.

In this market, hard money and bridge loan rates present even higher premiums, generally ranging between 8% and 12%. These short-term financing solutions, while more expensive, offer flexibility for investors needing quick capital for acquisitions or renovations. Such loans typically require a lower DSCR threshold but come at the cost of elevated interest rates and fees. Investors leveraging these financing options must strategically calculate the trade-offs between short-term liquidity needs and long-term financing stability.

The decision to refinance or hold properties is intricately linked to the current rate environment. Investors who locked in lower rates before the recent hikes are weighing the benefits of maintaining current financing against the potential gains from refinancing. For instance, refinancing could free up equity but might not be beneficial if it leads to higher debt service costs due to increased rates. On the other hand, holding existing debt arrangements might preserve cash flow but could limit the ability to expand portfolios or reinvest in property enhancements.

Finally, the current interest rate climate has a noticeable impact on acquisition criteria and underwriting standards. Investors are now more cautious, emphasizing properties with strong cash flow potential and operational efficiency. Underwriting standards have tightened, with lenders scrutinizing NOI projections and expense ratios more rigorously. This has resulted in a shift towards properties that can demonstrate a robust financial performance with room to absorb the impact of rising costs. Investors must adapt acquisition strategies to prioritize properties with stable income streams and potential for value-add improvements to meet the evolving standards of lenders and market expectations.

Investment Strategy & Risk Management

In the current real estate landscape, timing is paramount for maximizing returns and minimizing risks. Market timing considerations should revolve around identifying strategic entry points where property values are poised for appreciation and rental yields are attractive. As we navigate through mid-2026, this involves analyzing trends such as interest rate fluctuations, economic growth indicators, and seasonal patterns. With interest rates stabilizing after a volatile period, there is a window of opportunity for investors to lock in favorable financing terms before potential rate hikes. Furthermore, aligning acquisition timing with seasonal trends—such as increased buyer activity during spring and summer—can enhance exit strategies for fix-and-flip projects.

Risk factors are more prevalent in today’s market environment, primarily due to economic uncertainties and potential regulatory changes. It is crucial to implement robust risk mitigation strategies, such as maintaining adequate contingency reserves and securing comprehensive insurance coverage. Additionally, stress-testing assumptions—like rental income projections and property appreciation rates—against various economic scenarios can help investors prepare for potential downturns. Diversifying across different asset classes and geographic locations can also reduce exposure to localized economic shocks.

Adjusting acquisition criteria and underwriting standards is essential to mitigate risks and capitalize on opportunities. Prime Property Funding should consider tightening underwriting standards by incorporating more conservative assumptions on rental growth and exit prices. For fix-and-flip projects, this means ensuring a wider margin between acquisition costs and expected sale prices to account for potential market fluctuations. For buy-and-hold strategies, focusing on properties with higher cap rates and strong rental demand can enhance cash flow and long-term appreciation potential.

In conclusion, investors should adopt a flexible yet cautious approach, leveraging current market conditions to their advantage while safeguarding against risks. By staying informed and proactive, investors can navigate the complexities of the real estate market and achieve robust returns.

Key Considerations for Investors

- **Fix-and-flip strategies**: Aim for a minimum 20% profit margin to cushion against unexpected costs and market fluctuations.

- **Exit timing**: Prioritize selling properties during peak market seasons (spring and summer) to maximize sale prices and reduce holding periods.

- **Contingency planning**: Allocate at least 10% of the project budget for unforeseen expenses to prevent project delays and financial strain.

- **Cap rate targets**: For buy-and-hold investments, seek properties with cap rates above 6% to ensure healthy returns amidst potential interest rate increases.

- **DSCR cushions**: Maintain a minimum DSCR of 1.25 to provide a safety net against income variability and interest rate changes.

- **Bridge financing**: Secure financing with flexible draw schedules and set aside 5-10% of the loan amount as contingency reserves.

- **Geographic focus**: Target emerging markets such as the Southeast and Midwest, where demographic trends support long-term growth and risk-adjusted returns.

- **Conservative underwriting**: Stress-test scenarios with a 1-2% increase in interest rates and a 5-10% drop in property values to ensure project viability.

- **Portfolio diversification**: Balance property types and locations, aiming for no more than 30% exposure to any single market or asset class.

- **Risk mitigation**: Prioritize properties with a strong tenant base and good condition, and maintain reserves to cover at least six months of operating expenses.

By integrating these strategies, investors can confidently navigate the current real estate market, making informed decisions that align with their investment goals and risk tolerance.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.