Investor Market Analysis – 2026-05-02

Prime Property Funding Market Analysis for 2026-05-02. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – May 2026

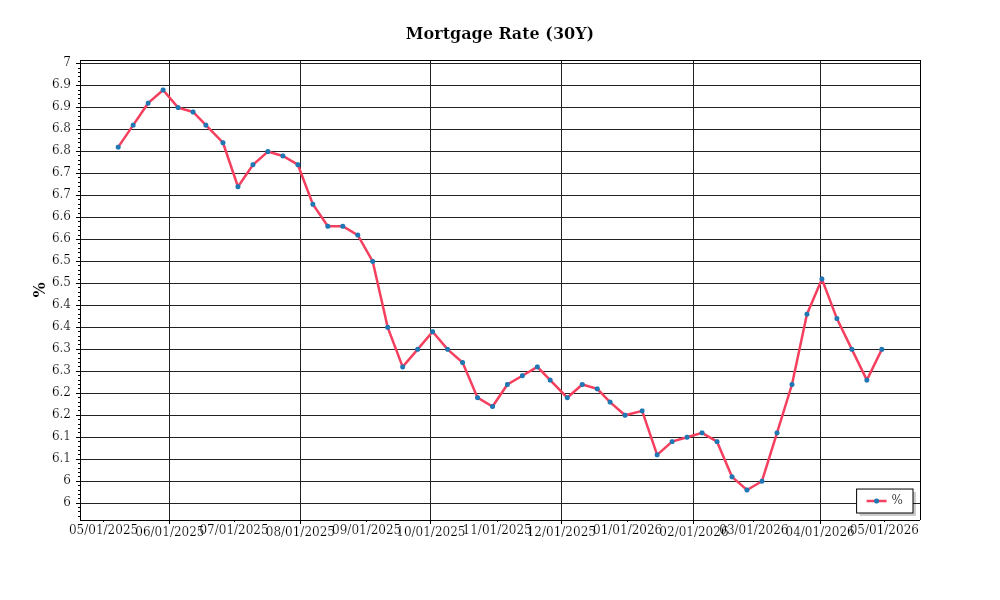

| 30-Year Mortgage Rate: | 6.30% |

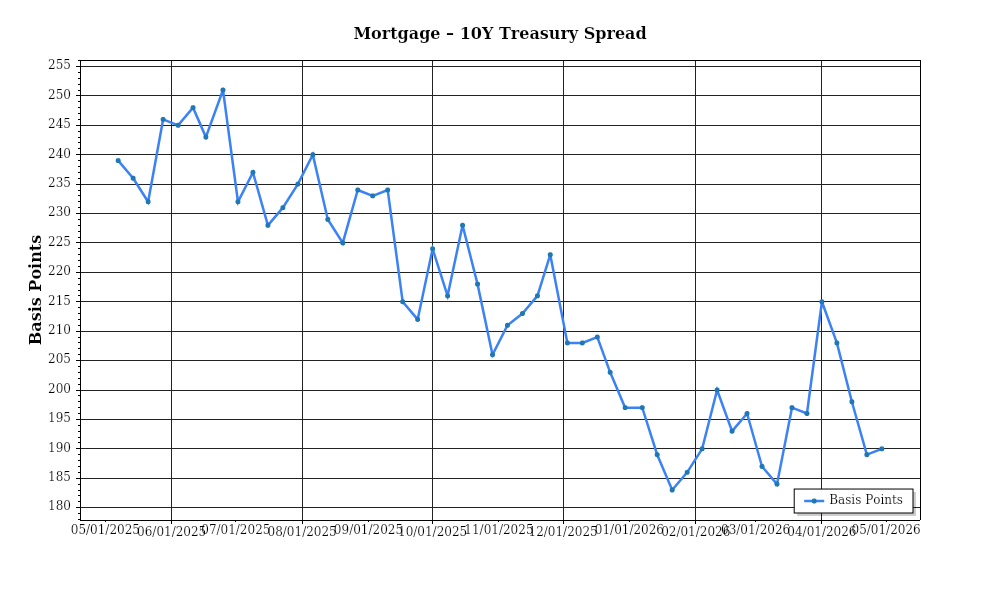

| Mortgage–Treasury Spread: | 190 bps |

Current Market Conditions

As of May 2026, the mortgage rate environment exhibits a complex landscape influenced by various macroeconomic factors. The average 30-year fixed mortgage rate currently stands at 6.3%, reflecting a slight decrease from the 6.5% recorded in April 2026. This marginal decline aligns with a recent dovish stance from the Federal Reserve, which has hinted at pausing its rate hikes due to cooling inflation pressures. However, the long-term trajectory of mortgage rates remains uncertain, with forecasts suggesting a potential range between 5.8% and 6.8% over the next 12 months, heavily contingent on inflationary trends and economic growth rates. In practical terms, this means that while current borrowers might experience slight relief in interest payments, prospective buyers should remain vigilant as rates could still fluctuate in response to broader economic conditions.

The mortgage-treasury spread, which serves as an indicator of lender risk perception, has widened slightly, standing at 2.5% in May 2026 compared to 2.3% in March 2026. This spread expansion suggests increased risk aversion among lenders, likely driven by concerns over geopolitical tensions and a moderate slowdown in economic growth. Typically, a wider spread indicates that lenders are demanding a higher risk premium for mortgage lending compared to safer government securities. For investors, this signals a more cautious lending environment where credit availability could tighten, affecting the ability of potential homebuyers to secure favorable mortgage terms. Moreover, this environment might encourage investors to scrutinize properties more closely for potential risk factors.

On the pricing front, the median home price in the United States has risen to $435,000 as of May 2026, marking a year-over-year increase of 6.8%. However, this national statistic belies significant regional variations. For instance, the Western U.S. continues to witness robust growth, with cities like San Francisco and Seattle seeing median price increases of 8% and 9.5%, respectively. In contrast, the Midwest experiences more modest growth, with median prices in cities like Cleveland and Detroit rising by 4% and 3.5%. These variations highlight the ongoing divergence in market dynamics across different regions, with coastal areas maintaining strong demand due to limited land availability and high-income demographics, while interior regions see slower appreciation due to more balanced supply-demand dynamics.

Inventory dynamics remain a pivotal factor in assessing market conditions. The national housing inventory level is approximately 2.5 months as of May 2026, indicating a seller’s market where supply is insufficient to meet current demand. This is a slight improvement over the 2.3 months recorded earlier this year, yet still far from the 6-month benchmark typically associated with a balanced market. The imbalance is exacerbated by prolonged construction timelines and regulatory bottlenecks. For investors, the low inventory levels signal continued competition for acquisitions, which could drive up prices and compress yields, especially in high-demand areas.

Cap rate trends provide further insight into the investment landscape. As of May 2026, the national average cap rate for multifamily properties is around 5.2%, reflecting a slight compression from 5.5% at the beginning of the year. This compression is indicative of increased investor demand for real estate assets, likely driven by their perceived stability in an otherwise volatile financial environment. However, the trend also suggests potential yield challenges, as lower cap rates mean that investors are willing to accept lower initial returns for anticipated capital appreciation. In practical terms, this underscores the necessity for investors to conduct meticulous due diligence to ensure that properties can generate sufficient income to meet return expectations despite ongoing cap rate compression.

Financing Environment & DSCR Analysis

The current financing environment in May 2026 is characterized by a moderate interest rate climate, with the Federal Reserve maintaining a steady approach to rate adjustments. Mortgage rates for commercial real estate hover around 5.5% to 6.0%, influencing **Debt Service Coverage Ratios (DSCR)** significantly. A higher interest rate environment directly affects the DSCR by increasing the cost of debt service, thereby reducing the coverage ratio if rental income does not proportionately increase. Investors and lenders are closely monitoring these ratios, as they are critical indicators of a property’s ability to cover its debt obligations. A tighter DSCR, say at a threshold of 1.35x, reflects a more conservative lending approach, requiring properties to generate $1.35 in income for every dollar of debt service, compared to a more lenient 1.25x threshold which allows for more aggressive financing structures.

In this market, most lenders demand a **DSCR of at least 1.30x**, balancing between risk and opportunity. This requirement acts as a safeguard, ensuring that properties generate sufficient net operating income (NOI) to cover debt obligations comfortably. For investors, meeting a 1.30x DSCR implies that for every $100,000 in annual debt service, the property must generate at least $130,000 in NOI. This threshold acts as a barrier for properties with lower cash flow margins, pushing investors to either negotiate better purchase prices or find ways to enhance property income, such as through value-add strategies or operational efficiencies.

For rental property owners, the current rate environment necessitates careful cash flow management. Consider a multifamily property with an annual rental income of $500,000 and operating expenses of $200,000, leaving an NOI of $300,000. With a DSCR requirement of 1.30x and a debt service obligation of $230,000, this property would just meet the requirement, with a DSCR of 1.30x. However, should interest rates nudge upward, increasing annual debt service to $240,000, the DSCR would drop to 1.25x, potentially disqualifying the property from refinancing under current lending standards. This scenario underscores the importance of stress-testing cash flows against potential rate hikes to maintain financing eligibility.

The market also sees a notable premium on **hard money and bridge loans**, with rates ranging between 8.0% and 10.0%. These short-term financing solutions offer flexibility for investors looking to reposition properties quickly but come at a higher cost. Such loans are particularly useful for properties that require significant rehabilitation or that are transitioning between tenants. The high cost of these loans necessitates a clear exit strategy, often involving refinancing to a lower-rate permanent loan once the property’s value and cash flow have been stabilized.

Refinancing strategies are becoming increasingly nuanced in this rate environment. Investors face the choice between locking in current rates to hedge against future increases or holding off in anticipation of potential rate drops. The decision heavily relies on the property’s current DSCR and projected cash flow stability. Properties with strong cash flows may opt to refinance now, securing predictable debt service costs, while those with tighter margins might delay refinancing, focusing on enhancing income streams to meet more stringent underwriting standards in the future.

Given these conditions, acquisition criteria are tightening. Investors must be diligent in their **underwriting standards**, ensuring that properties not only meet current DSCR requirements but also have the potential to withstand interest rate fluctuations. This often involves more conservative income projections, rigorous expense management, and a thorough analysis of market trends to ensure long-term viability. The current financing environment demands a strategic approach, balancing the immediate benefits of acquiring properties with the long-term implications of debt servicing under varying economic scenarios.

Investment Strategy & Risk Management

In the current real estate landscape of May 2026, savvy investors must employ strategic timing and acute market awareness to identify fruitful opportunities. Given the cyclical nature of real estate markets, timing the acquisition of properties during periods of lower competition can yield substantial benefits. Investors should prioritize markets with high demand and limited supply, as these conditions often yield higher appreciation potential. The spring buying season traditionally offers increased inventory, allowing for more negotiation leverage. Recognizing these patterns can help investors make informed decisions that capitalize on market fluctuations.

However, with opportunity comes risk, and the current environment presents several unique challenges. Rising interest rates are a critical factor, potentially affecting both acquisition costs and holding expenses. Investors should implement **interest rate hedging strategies** and lock in favorable terms where possible. Additionally, property value volatility requires robust contingency planning. Leveraging **stress testing** in underwriting can provide insights into potential downside scenarios, ensuring resilience against unexpected market shifts. Maintaining a diversified portfolio can also mitigate risk, spreading exposure across various asset classes and geographic locations to buffer against localized downturns.

Adjusting acquisition criteria in response to these conditions is crucial. Investors should adopt a more conservative approach, tightening underwriting standards to account for potential economic fluctuations. This includes reassessing **DSCR (Debt Service Coverage Ratio) thresholds** to ensure properties can withstand income variability. In the fix-and-flip sector, maintaining a keen focus on **spread risk**—the gap between purchase price, renovation costs, and expected sale price—is essential. Investors should also build in **contingency reserves** to accommodate unforeseen expenses, ensuring projects remain financially viable even if timelines extend or market conditions shift unexpectedly.

Ultimately, the key to thriving in today’s market is flexibility and preparedness. By incorporating comprehensive risk management strategies and maintaining a disciplined approach to acquisitions, investors can navigate the complexities of the current landscape with confidence. This proactive mindset not only safeguards investments but also positions investors to seize opportunities as they arise, driving sustained success in their real estate endeavors.

Key Considerations for Investors

- For fix-and-flip projects, maintain a **holding cost reserve** of at least 10% of total project costs to cover unexpected delays.

- Target a **minimum spread** of 20% between acquisition, renovation, and resale price to ensure profitability even in softening markets.

- Set cap rate targets for buy-and-hold properties at a minimum of **7%** to ensure competitive cash flow relative to market conditions.

- Assume a **3-5% annual rent growth** rate as a conservative estimate in underwriting, adjusting based on specific market dynamics.

- Maintain a **DSCR cushion** of 1.25x or higher to safeguard against potential declines in rental income.

- In the current rate environment, ensure bridge financing rates are fixed or capped to protect against rate hikes, with **contingency reserves** of 5-10% built into budgets.

- Prioritize acquisitions in markets demonstrating consistent **job growth** and population increases, focusing on cities with **3%+ annual employment growth**.

- Conduct rigorous **stress testing** of property values, assuming a 10% decline in worst-case scenarios to assess investment resilience.

- Diversify portfolios across at least **three geographic regions** to reduce exposure to localized economic disruptions.

- Implement robust **tenant screening** processes to enhance tenant quality, reducing potential income volatility and enhancing property stability.

By staying informed and adaptable, investors can not only weather current uncertainties but also emerge stronger, capitalizing on the myriad opportunities the real estate market continues to offer.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.