Investor Market Analysis – 2026-04-17

Prime Property Funding Market Analysis for 2026-04-17. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

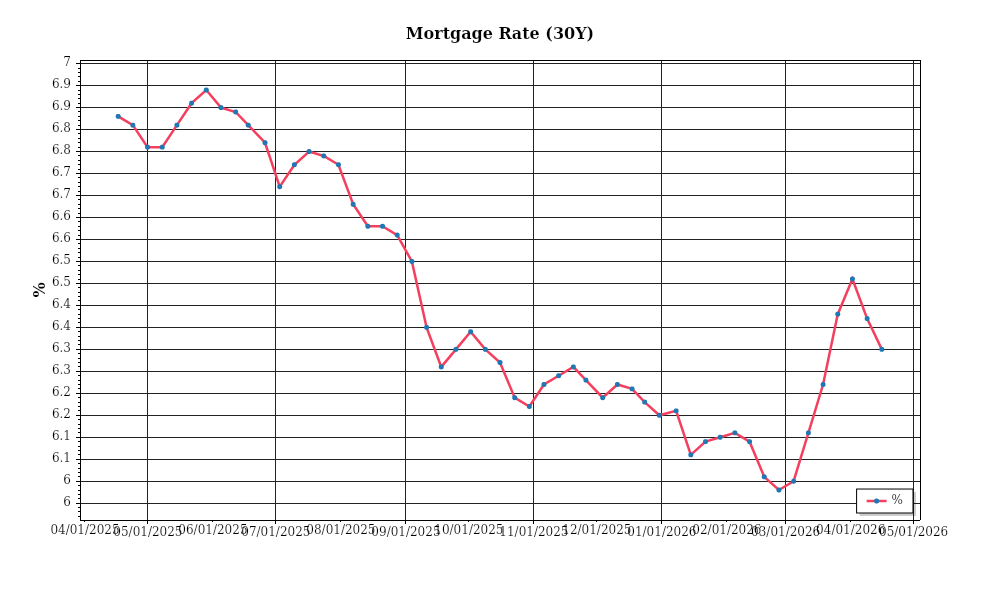

| 30-Year Mortgage Rate: | 6.30% |

| Mortgage–Treasury Spread: | 201 bps |

Current Market Conditions

As of April 2026, the mortgage rate environment is experiencing a significant shift reflective of broader economic conditions. The average 30-year fixed mortgage rate currently stands at 5.85%, which represents a 45 basis point increase from January of this year. This upward trend in mortgage rates can be attributed to the Federal Reserve’s ongoing efforts to manage inflation, which has been persistently above its target. Over the past 12 months, mortgage rates have increased by approximately 1.25 percentage points, indicating a tightening monetary policy stance. The trajectory suggests a continued rise, although at a potentially moderated pace if inflation shows signs of stabilization. For investors, this environment necessitates a focus on financing strategies that mitigate the impact of rising borrowing costs on investment returns.

The mortgage-treasury spread, a key indicator of lender risk perception, has also widened recently. Currently, the spread between the 30-year fixed mortgage rate and the 10-year Treasury yield is approximately 210 basis points, up from an average of 180 basis points seen in the previous year. This widening spread suggests increased risk aversion among lenders, likely due to a combination of economic uncertainty and potential credit quality concerns. A higher spread typically signals that lenders are demanding higher compensation for risk, which can lead to tighter credit conditions. For real estate investors, this implies a need for enhanced due diligence and perhaps a shift towards higher-credit-quality investments to navigate this environment effectively.

Median home price trends continue to exhibit growth, albeit at a slowing pace compared to the frenetic increases seen in the post-pandemic period. As of the latest data, the national median home price is approximately $406,000, reflecting a year-over-year appreciation rate of 3.7%. This is a deceleration from the double-digit appreciation rates observed in 2022 and 2023. Regionally, disparities remain significant; for instance, the South and Midwest are experiencing relatively robust appreciation rates of 4.5% and 4.2% respectively, driven by sustained in-migration and economic growth. Conversely, the West has seen a more modest increase of 2.1%, as affordability concerns and higher mortgage rates weigh more heavily. Such regional variations underscore the importance of localized market analysis for investors seeking to capitalize on areas with strong demand fundamentals.

Inventory dynamics remain a critical factor shaping the current real estate landscape. Nationally, housing supply has improved slightly, with the total inventory of unsold homes at 3.2 months of supply, up from 2.8 months a year ago. This increment signals a gradual easing of the severe supply constraints experienced in recent years but still falls short of a balanced market, typically defined by a 6-month supply. The competitive environment remains fierce, particularly in urban centers and high-demand suburban areas, where multiple-offer scenarios are still commonplace. For investors, this competition necessitates a strategic approach to acquisitions, with an emphasis on speed and decisiveness in deal-making to secure desirable properties.

Cap rate trends are also noteworthy, as they reflect broader shifts in investor sentiment and market conditions. Nationally, cap rates have expanded slightly, with the average cap rate for multifamily properties now standing at 5.1%, up from 4.8% a year earlier. This upward movement suggests a modest yield expansion, primarily driven by rising interest rates and increased financing costs. However, in markets where rental demand remains robust, such as the Southeast, cap rates have remained relatively compressed, indicating strong investor confidence in future income growth. For investors, this nuanced landscape emphasizes the need to balance yield expectations with market-specific risk assessments, particularly in an environment where financial conditions are tightening.

Financing Environment & DSCR Analysis

As of April 2026, the current interest rate environment is exerting significant pressure on the Debt Service Coverage Ratios (DSCR) for real estate investments. With average interest rates on commercial real estate loans hovering around 6.5%, up from the sub-4% levels seen a few years ago, borrowers are facing increased debt service costs. This rise in interest rates directly impacts the DSCR, which is a critical metric that lenders use to assess a borrower’s ability to service debt. A higher interest rate increases the monthly debt service obligation, thereby reducing the DSCR unless rental income can be increased to compensate for the higher costs. For example, on a $1 million loan amortized over 25 years, a rate increase from 4% to 6.5% raises the monthly payment from approximately $5,278 to $6,752, requiring an additional $1,474 per month in income to maintain the same DSCR.

In the current environment, lenders typically demand a DSCR of at least 1.25x to 1.35x, with more conservative lenders leaning towards the higher end of this spectrum to buffer against potential income shortfalls. A DSCR of 1.25x means that the property’s net operating income (NOI) must be at least 25% greater than its debt obligations. In practical terms, if a property has monthly debt payments of $10,000, it would need to generate at least $12,500 in NOI to meet a 1.25x threshold. With rising interest rates, the challenge for property owners is to ensure that rental income or other revenue streams are robust enough to meet these more stringent requirements. This often necessitates either increased rental rates or additional revenue-generating strategies, which can be challenging in competitive or over-saturated markets.

The increased cost of borrowing has significant cash flow implications for rental properties. For instance, consider a rental property generating $15,000 in monthly NOI. With a loan requiring $10,000 in monthly payments at a DSCR of 1.25x, the property would have $5,000 in monthly cash flow. However, if the interest rate increases the monthly payment to $12,000, the cash flow drops to $3,000, potentially compromising the investment’s viability if additional expenses or vacancies occur. This scenario highlights the importance for investors to carefully assess their property’s ability to sustain higher debt service costs and to explore opportunities for rental increases or expense reductions to shore up cash flow.

In this climate, hard money and bridge loan rate premiums have also widened, reflecting increased risk and liquidity constraints. These loans, typically used for short-term financing needs or to bridge the gap between acquisition and permanent financing, now command rates in the range of 9% to 12%. The higher rates reflect lenders’ increased risk aversion and the cost of capital, making them more expensive options for investors looking to acquire or reposition properties quickly. Consequently, investors must carefully weigh the cost of these loans against potential returns, ensuring that projected cash flows can support the higher debt service.

Given the elevated rates, investors face strategic decisions regarding refinance timing versus hold strategies. The decision to refinance an existing loan depends on the potential to secure a more favorable rate or term, which could be challenging in the current rate environment. Conversely, holding strategies may involve maintaining existing financing arrangements until rates stabilize or decrease. This necessitates a thorough analysis of existing loan terms, prepayment penalties, and market conditions to determine the optimal course of action.

Finally, the current rate environment is shaping acquisition criteria and underwriting standards. Investors and lenders alike are placing greater emphasis on property fundamentals, such as location, tenant credit quality, and lease terms, to mitigate risk. Underwriting is becoming increasingly stringent, with thorough due diligence and stress testing of cash flows against potential rate hikes and economic downturns. Investors must adapt by seeking properties with strong NOI potential and ensuring that acquisition prices reflect the increased cost of capital, thereby safeguarding profitability in a challenging financial landscape.

Investment Strategy & Risk Management

In the current real estate climate, characterized by fluctuating interest rates and evolving market dynamics, strategic timing and opportunity identification are crucial. Investors should be vigilant about market cycles, recognizing that while certain markets present lucrative opportunities, the timing of entry and exit is paramount. As demand for housing continues to shift, especially in areas undergoing demographic and economic changes, investors should seek to capitalize on undervalued properties or emerging neighborhoods. This requires a keen understanding of local market trends, permitting faster decision-making in rapidly changing conditions.

The current environment presents several risk factors, notably the potential for interest rate hikes and the ongoing volatility in both residential and commercial sectors. Mitigation strategies should prioritize flexible financing options and thorough due diligence processes. Investors should consider locking in rates where feasible and maintaining liquidity to navigate unforeseen market shifts. Diversification across asset classes, geographic regions, and investment strategies can further cushion against localized downturns. Additionally, maintaining a robust contingency fund is critical to cover unexpected costs and changes in market conditions.

To align acquisition criteria with current market realities, investors must adjust their underwriting standards. This includes revisiting cap rate targets and stress testing assumptions against various economic scenarios. Conservative assumptions about rent growth and occupancy rates should be employed to ensure that investments remain viable under less favorable conditions. For fix-and-flip projects, careful planning around holding costs and potential delays is essential. Investors should also consider more conservative loan-to-value ratios to mitigate leverage risks.

In conclusion, the key to navigating the current real estate market lies in a balanced approach that combines strategic market entry, disciplined risk management, and flexible investment criteria. By staying informed and agile, investors can identify and seize opportunities while safeguarding their portfolios against potential downturns. Confidence in well-researched strategies and a readiness to adapt will empower investors to thrive even amid uncertainty.

Key Considerations for Investors

- Fix-and-flip strategies: Ensure holding costs do not exceed 10% of the total project budget. Plan for a minimum 20% profit margin to account for market volatility.

- Exit timing: Target a sales window within 6 months post-renovation to minimize exposure to market changes.

- Contingency planning: Allocate at least 15% of project costs to a contingency reserve to address unexpected expenses.

- Buy-and-hold tactics: Aim for a cap rate of no less than 5.5% to ensure sufficient returns in a rising interest rate environment.

- DSCR cushions: Maintain a Debt Service Coverage Ratio of at least 1.25 to ensure robust cash flow.

- Bridge financing: Opt for short-term loans with flexible draw schedules and set aside 5% of the loan amount for contingency reserves.

- Market timing: Consider acquisition opportunities in the fall when competition is typically lower, balancing this against potential increased holding costs.

- Geographic focus: Investigate secondary markets such as Nashville or Raleigh for better risk-adjusted returns.

- Conservative underwriting: Stress test investment assumptions with scenarios anticipating a 2% increase in interest rates and a 10% drop in property values.

- Portfolio diversification: Ensure a mix of at least 3 asset classes and spread investments across 5 different geographic markets to mitigate risks.

- Risk mitigation: Establish reserves totaling at least 6 months of operating expenses and ensure properties are comprehensively insured against natural disasters and market fluctuations.

By adhering to these strategies and considerations, investors can navigate the complexities of the current market with confidence and foresight, positioning themselves for sustainable success.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.