Investor Market Analysis – 2026-04-16

Prime Property Funding Market Analysis for 2026-04-16. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

| 30-Year Mortgage Rate: | 6.37% |

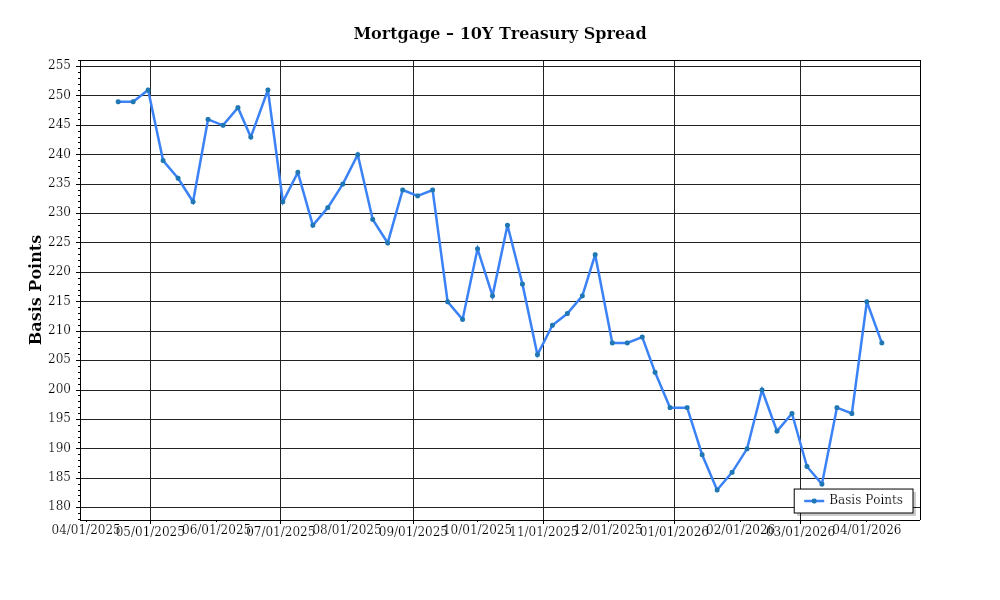

| Mortgage–Treasury Spread: | 211 bps |

Current Market Conditions

As of April 2026, the mortgage rate environment is experiencing notable shifts. The average 30-year fixed mortgage rate stands at 5.8%, a slight increase from 5.6% in March 2026. This uptick follows a year-long trend of moderated increases, reflecting the Federal Reserve’s cautious approach to interest rate hikes amidst inflationary pressures. Over the past twelve months, mortgage rates have ranged from 5.1% to 6.0%, indicating a relatively stable yet slightly upward trajectory. This environment suggests a gradual normalization post-pandemic, with moderate rate increases expected throughout the year. Analyzing this trend, investors should anticipate upward pressure on monthly mortgage payments, potentially dampening demand slightly as affordability constraints tighten.

In examining the mortgage-treasury spread, which currently sits at 1.75%, we can infer lender risk perceptions. This spread has narrowed from 2.0% at the same time last year, signaling a decrease in perceived lending risk. Typically, a narrowing spread indicates that lenders are more confident about borrower reliability and the broader economic outlook. The current spread, however, remains slightly above the pre-pandemic average of 1.5%, suggesting lingering caution. This cautious optimism is underpinned by economic stabilization and improved employment rates, yet tempered by potential geopolitical tensions and fluctuating global markets. Investors should interpret this as a signal that while the lending environment is becoming less risky, it has not fully returned to pre-pandemic norms.

The median home price across the United States has continued its upward trajectory, with current levels at $420,000, reflecting a 6.5% year-over-year increase. However, this national figure masks significant regional variations. For instance, the West Coast, particularly in tech-driven markets like San Francisco, has seen a more modest appreciation rate of 3.2%, bringing the median price to $890,000. In contrast, the Southeast, including cities like Charlotte and Atlanta, has experienced robust growth with appreciation rates exceeding 8%, driven by migration trends and relative affordability. These disparities highlight the importance of regional analysis for investors, as areas with higher growth rates may offer better short-term returns, albeit with increased competition and potential for market saturation.

Inventory dynamics reveal a market that is still grappling with imbalances. Nationally, the housing supply remains constrained, with an average inventory level of 2.4 months, well below the healthy market benchmark of 4 to 6 months. This scarcity is exacerbated by construction slowdowns due to supply chain disruptions and labor shortages. As a result, properties are experiencing rapid turnover, with average days on market decreasing to 21 days, compared to 34 days a year ago. Such tight conditions fuel competitive buyer environments, often resulting in bidding wars. This environment presents opportunities for sellers but poses challenges for buyers and investors seeking acquisitions at reasonable prices.

Cap rate trends offer a glimpse into the commercial real estate sector’s yield dynamics. Currently, cap rates average at 5.3%, showing a slight compression from 5.5% last year. This compression is indicative of increased investor demand for real estate assets, driven by their relative stability and income generation potential amidst volatile equity markets. However, the compression also signals potential yield risks, as investors may be accepting lower returns in anticipation of continued appreciation and rental growth. In practical terms, this suggests that while investment opportunities remain attractive, particularly in high-demand sectors like multifamily and industrial, investors should remain vigilant of overvaluation and ensure that acquisitions align with long-term strategic objectives.

Financing Environment & DSCR Analysis

In April 2026, the financing environment is characterized by a relatively high interest rate climate, which significantly impacts the Debt Service Coverage Ratio (DSCR) for real estate investors. With mortgage rates hovering around 6.5% for standard 30-year fixed loans, investors face increased debt servicing costs. This directly affects the DSCR, a critical metric used by lenders to assess the risk of a real estate investment. A higher interest rate naturally inflates the monthly debt obligations, thereby reducing the DSCR. For example, if an investor secures a property generating $10,000 in monthly rental income, and the debt service totals $7,500 monthly, the DSCR would be 1.33x. However, under current rates, the debt service might increase to $8,000, reducing the DSCR to 1.25x, which may fall below the preferred threshold for many lenders.

In today’s market, DSCR requirements are adjusting to accommodate the evolving financial landscape. Lenders typically enforce a minimum DSCR of 1.25x; however, given the current economic uncertainties and rate fluctuations, a more conservative 1.35x is becoming increasingly common. This shift implies that borrowers need to demonstrate stronger cash flow resilience to qualify for traditional financing. For instance, if a property previously qualified with a DSCR of 1.25x, generating $120,000 annually against $96,000 in debt service, the new requirement would necessitate an increase in net operating income or a reduction in debt service to meet the 1.35x threshold. This requirement compels investors to either enhance operational efficiencies or consider properties with inherently stronger revenue streams.

The implications for cash flow in rental properties are profound. Consider a property with an annual rental income of $200,000 and operating expenses totaling $60,000. The net operating income (NOI) would be $140,000. With current financing at 6.5%, annual debt service might rise to $112,000, resulting in a DSCR of approximately 1.25x. This tight margin leaves little room for unforeseen expenses, reducing the attractiveness of such investments under current conditions. Investors are thus more cautious, potentially seeking properties in markets with higher rental yields or those with the potential for operational improvements to bolster cash flow.

In the current financing landscape, hard money and bridge loans are seeing rate premiums reflecting risk and liquidity concerns. Rates for these short-term financing solutions range between 8% and 12%, substantially higher than traditional loans. These premiums reflect lenders’ risk aversion and the short-term nature of such loans. While they provide crucial flexibility for quick acquisitions or renovations, the cost implications are significant. For a $1 million property acquisition, a 10% interest rate would incur annual interest payments of $100,000, substantially impacting cash flow and necessitating a rapid refinancing strategy once stabilized.

The decision to refinance or hold properties is particularly strategic in this environment. With anticipations of potential rate stabilization or decline in the near term, many investors are adopting a ‘wait-and-see’ approach to refinancing. Holding onto current financing terms, despite higher rates, could be advantageous if future conditions allow for refinancing at more favorable rates. Conversely, properties with imminently expiring loans face pressure to refinance, even at current rates, to avoid punitive default scenarios.

The impact on acquisition criteria and underwriting standards is equally significant. Investors are more discerning, prioritizing properties with robust cash flow potential and manageable debt levels. Underwriting processes are stricter, with increased emphasis on stress-testing cash flows against potential interest rate hikes. As a result, properties with below-market rents or those requiring significant capital expenditure face higher scrutiny. This environment necessitates a meticulous approach to both property selection and financial structuring to ensure resilience against the prevailing high-interest landscape.

Investment Strategy & Risk Management

As the real estate market in April 2026 continues to evolve, strategic investment involves meticulous market timing, recognizing opportunities, and robust risk management. The current environment, characterized by fluctuating interest rates and varied regional performance, demands a nuanced approach. For Prime Property Funding, which specializes in hard money loans, fix-and-flip financing, and DSCR loans, identifying opportunities hinges on data-driven analysis and agile decision-making.

**Market Timing Considerations and Opportunity Identification:** In the prevailing market, timing is crucial. Investors must be vigilant about macroeconomic indicators that suggest optimal entry and exit points. The recent stabilization in interest rates provides a window for acquisition, particularly in high-demand urban areas where inventory remains constrained. Identifying properties with value-add potential in these markets can yield significant returns, especially when coupled with strategic improvements. The key is to monitor not only economic signals but also local market trends, such as employment growth and infrastructure development, which can influence property values.

**Risk Factors in Current Environment and Mitigation Strategies:** The primary risk in today’s market is the uncertainty surrounding economic conditions, including potential interest rate hikes. This volatility necessitates a comprehensive risk mitigation strategy. Investors should hedge against interest rate fluctuations by securing fixed-rate financing where possible and maintaining liquidity to manage unexpected expenses. Additionally, diversifying across geographic locations and asset classes can reduce exposure to localized downturns. Incorporating robust due diligence processes, including stress testing cash flows against worst-case scenarios, is essential for safeguarding investments.

**Adjusting Acquisition Criteria and Underwriting Standards:** In light of these risks, adjusting acquisition criteria is imperative. Prioritizing properties with strong cash flow potential and high occupancy rates is essential. Underwriting standards should be tightened, with a focus on conservative revenue projections and higher DSCR thresholds to cushion against potential income disruptions. For fix-and-flip projects, ensuring a substantial spread between acquisition costs and potential sales prices is critical to absorb holding costs and market fluctuations. With buy-and-hold strategies, aiming for properties with cap rates exceeding 6% can provide a buffer against unforeseen market changes.

Key Considerations for Investors

- **Fix-and-flip strategies:** Target a spread of at least 20% between purchase and potential sale price to cover holding costs and unforeseen expenses.

- **Buy-and-hold tactics:** Aim for a **cap rate** of at least 6% and factor a rent growth assumption of 3% annually to ensure robust cash flow.

- **Bridge financing:** Secure financing with a **fixed rate** to mitigate interest rate risk and establish a draw schedule that aligns with project milestones.

- **Market timing:** Consider **seasonal trends**, with spring acquisitions potentially offering better pricing due to increased inventory.

- **Geographic focus:** Prioritize markets with strong job growth and population influx, such as Austin, TX, and Raleigh, NC, for **risk-adjusted returns**.

- **Conservative underwriting:** Implement stress tests assuming a 10% reduction in rental income to ensure sustainability.

- **Portfolio diversification:** Balance investments across **asset classes** such as residential, commercial, and industrial properties to mitigate sector-specific risks.

- **Risk mitigation:** Maintain at least 6 months of **reserves** for operating expenses and debt service to weather economic downturns.

- **Tenant quality:** Implement rigorous screening to ensure high-quality tenants, reducing the risk of default and vacancies.

- **Property condition:** Prioritize properties with minimal deferred maintenance to reduce upfront capital expenditure and unforeseen costs.

In conclusion, by strategically timing market entry, meticulously managing risks, and adjusting acquisition criteria, investors can capitalize on current opportunities while safeguarding their portfolios. With these strategies, Prime Property Funding can confidently navigate the real estate landscape, maximizing returns and minimizing risks.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.