Investor Market Analysis – 2026-04-13

Prime Property Funding Market Analysis for 2026-04-13. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

| 30-Year Mortgage Rate: | 6.37% |

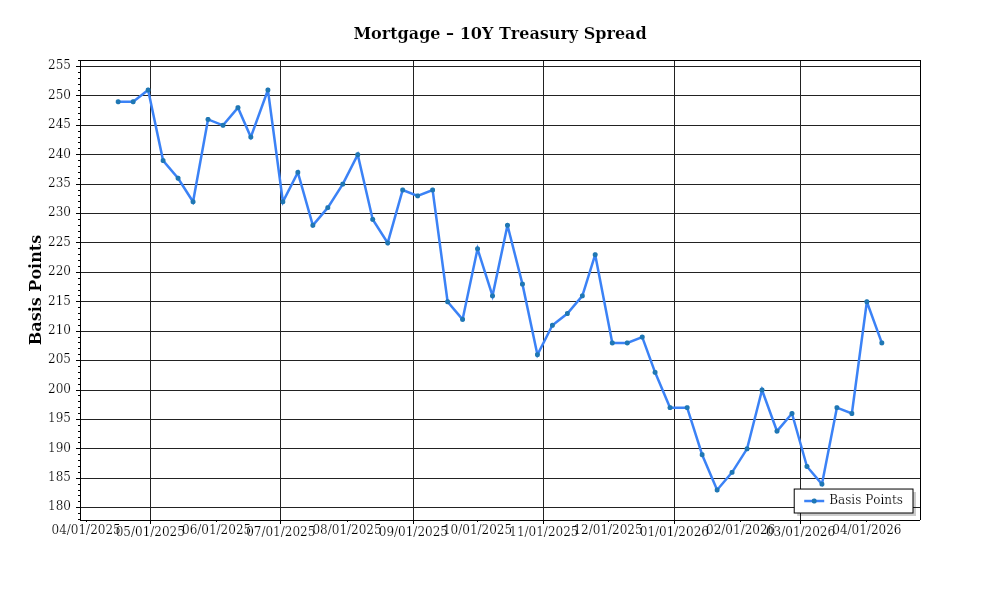

| Mortgage–Treasury Spread: | 208 bps |

Current Market Conditions

As of April 2026, the real estate market is navigating a complex landscape characterized by varied influences on mortgage rates, home prices, and inventory levels. The current mortgage rate environment is a key factor shaping the market, with the average 30-year fixed mortgage rate now standing at 5.2%. This represents a 0.3 percentage point increase from the same period last year. This uptick is primarily driven by the Federal Reserve’s ongoing monetary tightening policies intended to curb inflation, which have led to a more cautious lending environment. Additionally, the trajectory suggests a gradual but steady increase in rates as economic indicators point towards sustained inflationary pressures. This rise in mortgage rates is expected to impact affordability, particularly for first-time homebuyers, potentially cooling down the robust demand seen in recent years.

The mortgage-treasury spread, a critical indicator of lender risk perception, currently averages 1.9%. This is slightly above the historical norm of 1.5%, indicating heightened risk aversion among lenders. The spread has widened over the past six months, reflecting uncertainties in the broader economic outlook and concerns over borrower creditworthiness. A persistently high spread suggests that lenders are pricing in greater risks, possibly due to anticipated economic slowdowns or the potential for increased default rates. For investors, this could signal tighter credit conditions and an increased need for due diligence when assessing potential acquisitions.

Median home prices continue to show significant variation across different regions. Nationally, the median home price has risen to $410,000, marking a year-over-year appreciation rate of 6.5%. This growth, while robust, is a deceleration from the double-digit gains observed in previous years. Regionally, markets such as the Midwest and Southeast are experiencing higher than average appreciation rates of 8.2% and 7.5% respectively, driven by population influxes and relatively affordable housing stock. Conversely, the West Coast and Northeast regions are seeing slower growth rates of 4.3% and 3.8%, due in part to higher baseline prices and more stringent regulatory environments. These disparities highlight the importance of regional analysis in investment decisions, as market dynamics can vary significantly.

Inventory levels remain a critical factor in the market’s balance, with current housing inventory at approximately 3.4 months of supply. This figure indicates a slight increase from previous quarters but still falls below the 5-6 month range typically associated with a balanced market. The undersupply is exacerbated by ongoing supply chain disruptions and labor shortages affecting new construction, coupled with many homeowners opting to stay put due to favorable existing mortgage rates. The competitive landscape for acquisitions remains fierce, particularly in high-demand regions, where bidding wars are not uncommon. This scarcity of inventory continues to support price appreciation, albeit at a moderated pace compared to the pandemic-driven surge.

Cap rate trends are also evolving, with current average cap rates at 5.1%, reflecting a slight compression from last year’s 5.3%. This trend indicates that investors are willing to accept lower initial yields, likely due to expectations of continued property value appreciation and rental income growth. The compression is more pronounced in urban centers and high-growth suburbs, where demand for residential and mixed-use properties remains strong. However, in less dynamic markets, cap rates have remained stable or even expanded slightly, as investors require higher yields to offset perceived risks. Understanding these shifts is crucial for investors seeking to balance yield expectations with risk management in their portfolios.

Together, these factors paint a picture of a market in transition, influenced by external economic forces and internal supply-demand dynamics. Investors must navigate these conditions with a keen eye on regional variations, risk assessments, and evolving economic indicators to make informed decisions.

Financing Environment & DSCR Analysis

The financing environment in April 2026 presents a complex landscape for real estate investors, particularly regarding the impact of current interest rates on Debt Service Coverage Ratios (DSCR). With the Federal Reserve’s recent adjustments maintaining a cautious yet firm stance on rates, the benchmark interest rates are presently around 5.25%. This environment leads to elevated borrowing costs, which directly influence DSCRs—a critical metric for lenders assessing the risk involved in providing loans for rental properties. A higher interest rate increases the monthly debt service, which can compress the DSCR if rental incomes do not rise correspondingly. For instance, a typical investment property with an annual net operating income (NOI) of $120,000 and annual debt service of $90,000 would have a DSCR of 1.33x. However, with increasing interest rates causing the debt service to rise to $100,000, the DSCR would shrink to 1.20x, potentially falling below lender requirements.

In the current market, typical DSCR requirements have adjusted slightly. More conservative lenders may now demand a minimum DSCR of 1.35x, compared to previous thresholds as low as 1.25x. This shift reflects the increased risk aversion due to interest rate volatility and economic uncertainty. Lenders are looking to ensure that properties can cover debt obligations comfortably despite potential fluctuations in the rental market or unforeseen operating expenses. For investors, meeting these heightened requirements means either increasing rental incomes or reducing loan amounts, possibly requiring a larger equity stake. For example, to achieve a 1.35x DSCR with a $100,000 debt service, an NOI of $135,000 would be necessary, prompting investors to enhance property management efficiency or consider value-add strategies that boost income.

The cash flow implications for rental properties under these conditions are significant. Higher debt obligations mean cash flow margins can tighten, impacting the investor’s ability to reinvest in property improvements or distribute returns to stakeholders. Consider a scenario where a property generates a monthly NOI of $10,000, and the debt service increases from $7,500 to $8,333 due to rising rates. The monthly net cash flow reduces from $2,500 to $1,667, a 33% decrease. Such a reduction necessitates a reevaluation of operational budgets and might push investors towards markets with higher rent growth potential or properties with untapped income opportunities.

In this climate, hard money and bridge loan rate premiums have also seen an uptick. These short-term, high-interest loans provide flexibility but come with costs that can be prohibitive in a high-rate environment. Currently, hard money loans might command interest rates in the range of 9% to 12%, while bridge loans could be slightly lower but still above conventional mortgage rates. These premiums reflect the risk lenders associate with short-term, speculative investments and necessitate careful consideration by investors, particularly regarding exit strategies and refinancing possibilities.

The decision between refinance timing and hold strategies is crucial given the current rate environment. Investors holding properties with lower-rate loans secured in previous years face the dilemma of refinancing to access equity or holding to maintain favorable terms. If refinancing leads to a higher interest rate, the associated costs might offset benefits unless the equity is deployed into significantly higher-return projects. Conversely, holding might limit capital availability but preserves cash flow stability. Each strategy’s viability depends on market forecasts and individual investment goals, emphasizing the importance of tailored financial analysis.

Finally, the impact on acquisition criteria and underwriting standards is pronounced. Investors must exercise greater diligence, ensuring properties meet stricter financial metrics and exhibit resilience against economic fluctuations. Underwriting is increasingly incorporating stress testing for interest rate hikes and potential dips in rental income, necessitating robust property performance histories and market analysis. The current environment demands a strategic approach, balancing risk with opportunity, and aligning acquisition decisions with long-term financial objectives.

Investment Strategy & Risk Management

In the current real estate market, timing is everything for maximizing returns, especially given the cyclical nature of real estate and the broader economic environment as of April 2026. With interest rates stabilizing after recent fluctuations and inflation pressures easing, investors have a window of opportunity to capitalize on acquisitions before anticipated rate hikes potentially re-emerge in the latter half of the decade. Identifying markets with strong demographic growth and economic resilience can provide a strategic edge. Investors should focus on areas with robust employment growth and diversified economic bases, which are likely to outperform in both rental and resale markets.

Risk management has become increasingly crucial in this environment. Market volatility, potential regulatory changes, and fluctuating material costs pose significant challenges. To mitigate these risks, investors need to incorporate flexible strategies such as dynamic pricing models and contingency planning. For example, incorporating a 10-15% contingency in renovation budgets can safeguard against unexpected expenses, ensuring projects remain viable even if costs escalate. Additionally, maintaining liquidity reserves equivalent to 6-12 months of operating expenses can provide a buffer against unforeseen downturns or rental vacancies.

Adjusting acquisition criteria and underwriting standards is essential for navigating the current landscape. Focus should be on conservative assumptions, particularly regarding rent growth and exit cap rates. Investors are advised to target properties with cap rates at least 1% above the current market average to account for potential economic shifts. Furthermore, maintaining a debt service coverage ratio (DSCR) of 1.25 or higher can help ensure properties remain cash flow positive, even in less favorable market conditions. Rigorous stress testing of financial models against various scenarios can highlight vulnerabilities and inform more resilient investment strategies.

Prime Property Funding clients can excel by adopting a diversified approach, balancing fix-and-flip projects with buy-and-hold investments and strategic bridge financing. This mixed strategy allows investors to capture quick returns through flipping while building long-term wealth through rental income. By focusing on high-demand areas and maintaining a disciplined approach to underwriting, investors can position themselves to thrive in both stable and turbulent markets.

Key Considerations for Investors

- For fix-and-flip strategies, aim for a minimum gross profit margin of 25% to account for holding costs and potential market fluctuations.

- Implement contingency plans that allocate at least 10% of the renovation budget for unexpected expenses.

- Set cap rate targets for buy-and-hold properties at 6% or higher to ensure competitive cash flow margins.

- Incorporate a DSCR cushion of 1.25 to 1.5 to ensure sustainability during periods of lower rental income.

- Utilize bridge financing with flexible draw schedules to adapt to project timelines and market conditions.

- Prioritize markets with a rent growth projection of 3% annually, ensuring sustainability in income growth.

- Focus investments in geographic areas with a diverse economic base, such as tech hubs or regions with robust healthcare sectors.

- Conduct stress tests on underwriting assumptions, simulating scenarios with cap rate increases of up to 2% and rent decreases of 5%.

- Maintain a diversified portfolio across asset classes and geographies to optimize risk-adjusted returns.

- Ensure properties have adequate insurance coverage and maintain reserves for capital improvements and tenant turnover.

By utilizing these strategies and maintaining a proactive approach, Prime Property Funding clients can confidently navigate the current landscape, leveraging both short-term gains and long-term wealth-building opportunities.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.