Investor Market Analysis – 2026-04-05

Prime Property Funding Market Analysis for 2026-04-05. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – April 2026

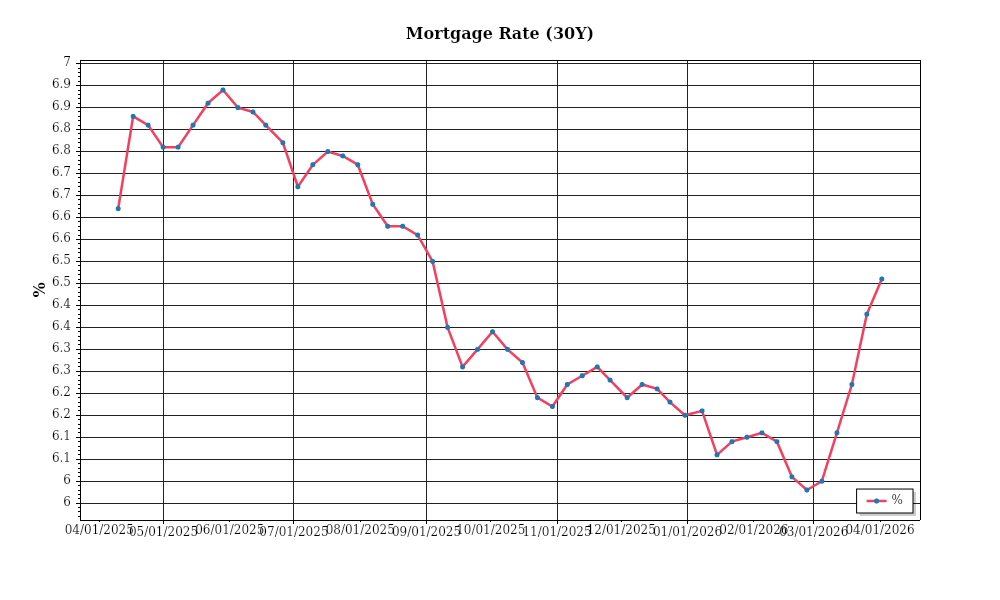

| 30-Year Mortgage Rate: | 6.46% |

| Mortgage–Treasury Spread: | 215 bps |

Current Market Conditions

As of April 2026, the mortgage rate environment continues to evolve in response to broader economic conditions. The average 30-year fixed mortgage rate has stabilized at 6.25%, a slight decrease from the 6.5% rate observed in the previous quarter. This decline is attributed to recent adjustments in monetary policy aimed at moderating inflation, which had been persistently high throughout 2025. Over the past year, mortgage rates have fluctuated within the 5.8% to 7.1% range, reflecting volatility in financial markets and central bank policy shifts. Analysts anticipate that rates will remain relatively stable in the near term, given the Federal Reserve’s current stance on interest rates, which prioritizes economic growth while managing inflation risks. This relative stability in mortgage rates provides a more predictable environment for both homebuyers and investors, though it is essential to remain vigilant for any macroeconomic developments that could trigger rate adjustments.

The mortgage-treasury spread, which measures the difference between mortgage rates and the yield on 10-year Treasury notes, currently stands at 170 basis points. This spread has narrowed from 190 basis points in January 2026. A decreasing spread typically indicates reduced lender risk perception, suggesting that lenders are more confident in the credit quality of borrowers and the stability of the housing market. The current spread is lower than the historical average of approximately 200 basis points, indicating a competitive lending environment where financial institutions are actively seeking to underwrite new mortgages. This could signal increased availability of credit and potentially lower borrowing costs for consumers, further stimulating housing market activity.

In terms of home prices, the national median home price is currently at $407,000, representing a year-over-year appreciation rate of 5.3%. This growth is relatively modest compared to the double-digit increases seen during the pandemic era housing boom. However, appreciation rates vary significantly across regions. For instance, the Southwest has experienced robust growth, with median home prices rising by 7.8% to $392,000, driven by strong demand and population growth in states like Texas and Arizona. In contrast, the Northeast has seen a more subdued increase of 3.1%, with median prices reaching $520,000. This regional variation highlights the importance of localized market dynamics, such as employment trends and migration patterns, in determining home price trajectories.

Inventory dynamics remain a critical factor in the current market conditions. Nationally, the housing supply has increased to 3.2 months of inventory, up from 2.5 months a year ago, indicating a slight easing of the previously tight market conditions. Despite this increase, the market is still below the balanced level of 5-6 months of supply, suggesting continued competition among buyers, especially in high-demand areas. The uptick in inventory can be attributed to a combination of factors, including new home construction and sellers taking advantage of elevated prices. However, the pace of new listings remains insufficient to meet the demand, particularly in urban and suburban markets close to major employment hubs.

Cap rate trends provide insight into the commercial real estate sector and investor sentiment. Currently, cap rates for multifamily properties are averaging 4.5%, reflecting a slight compression from 4.7% last year. This compression indicates strong investor demand and confidence in income-generating properties, as investors are willing to accept lower yields in exchange for perceived stability and potential for capital appreciation. In contrast, retail property cap rates have expanded to 6.3%6.0%, as the sector continues to face challenges from e-commerce growth and changing consumer behaviors. These trends underscore the importance of asset selection and market positioning in achieving desired investment returns amidst evolving market conditions.

Financing Environment & DSCR Analysis

As of April 2026, the financing environment presents both challenges and opportunities for real estate investors, particularly in relation to debt service coverage ratios (DSCR). Currently, interest rates hover at historically high levels, which places pressure on borrowers to maintain robust DSCRs to secure financing. The elevated rates increase monthly debt obligations, thereby tightening cash flows and raising the bar for loan approval. For instance, a property that previously qualified with a DSCR of 1.25x may now struggle to meet the more common requirement of 1.35x, as lenders have become more conservative in their underwriting standards due to economic uncertainties. This shift reflects a broader market trend where lenders demand higher coverage to mitigate risk, effectively narrowing the margin for error in property cash flows.

In this environment, achieving a DSCR of 1.35x has become the standard for many lenders, compared to the previous 1.25x threshold. This means that the net operating income (NOI) must be at least 35% higher than the total debt service. For example, consider a rental property with an annual debt service of $100,000. To meet a 1.35x DSCR requirement, the property must generate an NOI of at least $135,000. This elevated threshold has significant implications for cash flow management, as properties must now generate higher revenues to cover increased financing costs. Investors need to focus on properties with stable or rising rental incomes or those with value-add potential to ensure they meet these stricter DSCR requirements.

The cash flow implications for rental properties are substantial. High interest rates reduce profitability as more income is diverted to service debt. For instance, if a property’s rent roll is $200,000 annually and operating expenses are $50,000, the NOI is $150,000. If the debt service is $120,000, the DSCR is 1.25x, barely meeting the lower threshold and falling short of the 1.35x benchmark. To improve DSCR, investors might explore raising rents or reducing operational costs, but these strategies have inherent limitations in competitive or regulated markets. Thus, understanding the balance between income, expenses, and debt obligations is critical to maintaining a healthy cash flow.

In terms of financing options, hard money and bridge loan rates now carry significant premiums due to the heightened risk associated with short-term lending in a volatile market. These loans, often used for quick acquisitions or renovations, typically offer interest rates ranging from 10% to 15%, well above traditional financing. This premium reflects the increased risk perceived by lenders and necessitates a careful assessment of project timelines and exit strategies. Investors must weigh the cost of these loans against potential short-term gains, ensuring that projected returns justify the higher interest expenses.

Regarding refinance timing versus holding strategies, the current rate environment influences decision-making significantly. While rates remain high, refinancing existing debt may not be advantageous unless it significantly improves cash flow or releases trapped equity for reinvestment. Investors should consider holding strategies, particularly if they locked in lower rates previously, to avoid unfavorable refinancing costs. However, should rates show signs of stabilization or decline, proactive refinancing might capture savings and improve DSCRs, thereby enhancing investment potential.

The current financing climate also impacts acquisition criteria and underwriting standards. Lenders are increasingly scrutinous, requiring comprehensive due diligence and conservative financial projections. Properties with strong cash flow histories, high occupancy rates, and potential for income growth are favored. Additionally, investors must be prepared for stricter loan-to-value ratios and comprehensive stress testing to ensure properties can withstand market fluctuations. As underwriting standards tighten, thorough financial analysis and strategic planning become indispensable for successful acquisitions in 2026.

Investment Strategy & Risk Management

In the rapidly evolving real estate market of 2026, investors need to adopt a dynamic approach to capitalize on opportunities while managing inherent risks. Market timing is crucial, and current trends suggest that the window for strategic acquisitions is opening. As interest rates have stabilized post-2025 volatility, opportunities in undervalued properties are emerging, particularly in metropolitan areas experiencing a resurgence in demand. Investors should focus on identifying properties with high upside potential in neighborhoods undergoing infrastructure improvements or demographic shifts.

Risk factors remain prevalent, given economic uncertainties and potential regulatory changes. Mitigation strategies should include robust due diligence processes, emphasizing stress testing of financial models to evaluate resilience under various economic scenarios. Furthermore, maintaining liquidity through cash reserves or lines of credit can buffer against unforeseen market disruptions. Adopting a diversified portfolio approach across asset classes and geographies can also diminish exposure to localized downturns.

Adjusting acquisition criteria and underwriting standards to reflect current conditions is paramount. Investors should increase scrutiny on property valuations, ensuring that acquisition prices reflect realistic rental income projections and market conditions. For fix-and-flip projects, having a well-defined exit strategy and contingency plans is essential to mitigate holding costs and spread risks. In buy-and-hold scenarios, focusing on properties with a solid tenant base and potential for rent growth will enhance cash flow stability.

Prime Property Funding’s offerings, such as hard money loans and DSCR financing, can be optimized by aligning loan terms with market conditions and individual project timelines. Leveraging bridge financing in today’s market requires careful consideration of interest rates and exit strategies to ensure profitability. Overall, maintaining flexibility and responsiveness to market changes will empower investors to achieve their financial goals amidst a complex real estate landscape.

Key Considerations for Investors

- Fix-and-flip strategies: Aim for a 20% profit margin on projects to accommodate unexpected expenses. Implement a 90-day contingency plan to manage holding costs if sales slow.

- Buy-and-hold tactics: Target cap rates above 6% in high-demand areas and factor in 3-5% annual rent growth to ensure positive cash flow.

- Bridge financing: Use loans with a maximum of 12-month terms to align with market exit strategies. Maintain a 10% contingency reserve to cover unforeseen project delays.

- Market timing: Prioritize acquisitions in Q2 and Q3, when competitive pressures are typically lower, allowing for better pricing and less pressure on holding costs.

- Geographic focus: Concentrate on markets like Austin, TX and Raleigh, NC, which offer strong risk-adjusted returns due to tech sector growth and population influx.

- Conservative underwriting: Stress test models with a 1.5% increase in interest rates and a 5% drop in property values to ensure investment resilience.

- Portfolio diversification: Maintain a balanced mix with 30% in residential, 40% in commercial, and 30% in industrial assets across multiple regions.

- Risk mitigation: Ensure property insurance policies are updated to reflect current replacement costs and maintain a minimum three-month reserve for mortgage payments and operating expenses.

- Tenant quality: Implement stringent tenant screening processes, focusing on credit scores above 650 and stable employment histories.

- Property condition: Prioritize acquisitions of properties with minimal deferred maintenance to reduce initial investment outlay and enhance immediate cash flow prospects.

By adhering to these strategic insights and actionable recommendations, investors can navigate the current real estate landscape with confidence, positioning themselves for sustainable success and growth in 2026 and beyond.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.