Investor Market Analysis – 2026-03-30

Prime Property Funding Market Analysis for 2026-03-30. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

| 30-Year Mortgage Rate: | 6.38% |

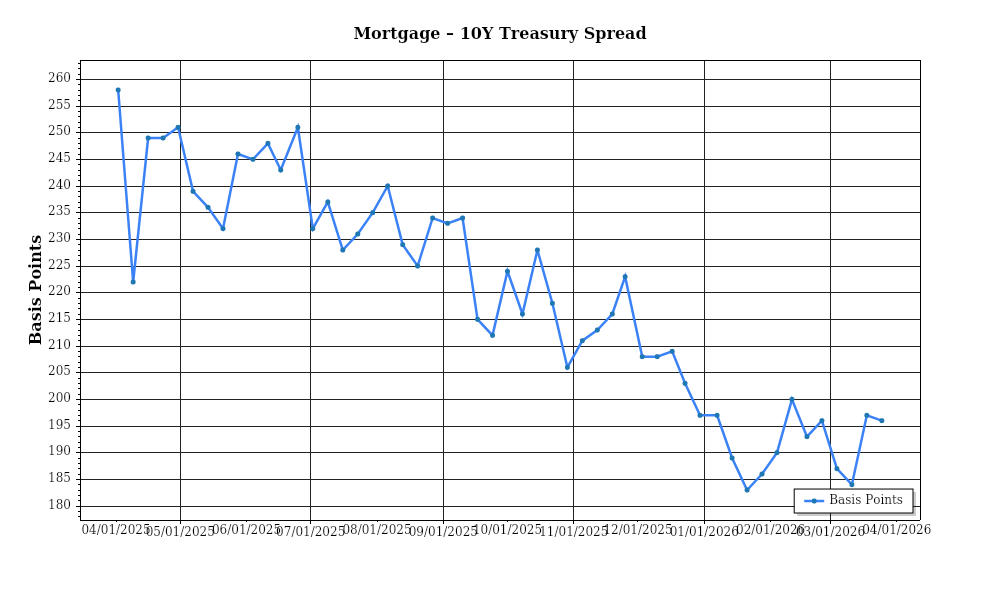

| Mortgage–Treasury Spread: | 196 bps |

Current Market Conditions

The current mortgage rate environment in March 2026 reveals a landscape characterized by both historical highs and recent stabilizations. The average 30-year fixed mortgage rate stands at 7.1%, showing a slight decrease from its peak of 7.5% in late 2025. Over the past year, the Federal Reserve’s monetary policies have exerted upward pressure on borrowing costs, largely in response to inflationary concerns. However, recent data suggest a plateauing trend, attributed to the Fed’s cautious approach in further rate hikes amid slowing economic growth. The average 15-year fixed mortgage rate is slightly lower at 6.5%, providing some relief for refinancing homeowners. This stabilization in mortgage rates could signal a potential shift towards more favorable borrowing conditions, albeit still high compared to pre-pandemic levels, when rates hovered around 3-4%.

Examining the mortgage-treasury spread, we observe critical insights into lender risk perceptions. As of March 2026, the spread between the 30-year mortgage rates and the 10-year treasury yield is approximately 2.2%. This spread is notably wider than the historical average of around 1.7%, indicating heightened risk aversion among lenders. This increased spread suggests that lenders are pricing in potential economic uncertainties and the risk of borrower defaults. It reflects a cautious lending environment, where financial institutions are wary of macroeconomic volatility and are adjusting their risk premiums accordingly. The wider spread also poses a challenge to affordability, as it contributes to keeping mortgage rates elevated, thereby affecting homebuyer purchasing power.

Turning to median home price trends, the national median home price is approximately $420,000, reflecting a year-over-year appreciation rate of 3.8%. This rate of appreciation marks a deceleration from the double-digit growth rates observed in 2022-2024, signaling a cooling housing market. Regional variations are pronounced; for instance, the West Coast, particularly cities like San Francisco and Seattle, sees a modest appreciation of 2.5%, while the Southeast, especially in metros like Atlanta and Raleigh, experiences a stronger growth rate of 5.2%. Such disparities highlight the uneven pace of housing demand and affordability across the country, influenced by local economic conditions and migration patterns.

Inventory dynamics continue to shape the market balance. The current housing inventory stands at approximately 3.1 months’ supply, indicating a slight increase from last year’s 2.8 months. This increase suggests a gradual shift towards a more balanced market, although it still falls short of the 5-6 months’ supply that typically characterizes an equilibrium between buyers and sellers. The increased inventory is partly due to rising mortgage rates, which have tempered buyer enthusiasm and extended time on market. However, competition remains fierce, particularly in suburban areas, where demand for larger homes and outdoor space persists. This ongoing competition underscores the need for strategic acquisition approaches for investors seeking entry into these markets.

Cap rate trends provide further insights into the real estate investment landscape. As of March 2026, the national average cap rate is 5.6%, representing a slight expansion from 5.3% in early 2025. This expansion indicates a subtle shift in investor sentiment, as rising interest rates and economic uncertainties prompt a reevaluation of asset yields. Despite this slight increase, cap rates remain compressed compared to historical norms, underscoring the sustained investor interest in real estate as a hedge against inflation and a source of stable returns. Yield compression in high-demand urban centers contrasts with modest expansions in secondary and tertiary markets, where investors seek higher returns to offset elevated risk profiles. This nuanced cap rate environment requires astute investment strategies to capitalize on emerging opportunities while managing potential downsides.

Financing Environment & DSCR Analysis

In March 2026, the financing environment is characterized by relatively high interest rates compared to recent years, directly impacting the Debt Service Coverage Ratios (DSCR) for real estate investors. As interest rates have risen, the cost of borrowing has increased significantly, affecting the ability to meet DSCR requirements. With average commercial mortgage rates now hovering around 6.5% to 7%, investors find themselves under pressure to maintain a DSCR of at least 1.25x to 1.35x, which are the typical thresholds required by lenders in this market. Higher interest rates increase monthly debt service obligations, challenging property owners to generate sufficient rental income to cover these costs, thereby squeezing DSCRs downward.

In this environment, lenders are adhering to stricter DSCR requirements, often demanding a minimum of 1.35x, especially for properties in less stable markets or those with higher perceived risk. This requirement ensures that properties can reliably cover their debt obligations with a comfortable margin. For example, a property generating $10,000 in monthly net operating income (NOI) would need to keep its monthly debt service below approximately $7,407 to meet a 1.35x DSCR. Conversely, a 1.25x DSCR would allow for a slightly higher maximum monthly debt service of $8,000. Properties not meeting these thresholds may face challenges in securing traditional financing, pushing investors to explore alternative funding options like hard money or bridge loans.

The current market dynamics have significant implications for cash flow from rental properties. For instance, consider a multifamily property with a mortgage rate of 6.5% and a loan amount of $1 million. If the annual debt service totals $76,000, the property must generate at least $95,000 in NOI to meet a 1.25x DSCR. With rising costs and potentially stagnant rent growth in some areas, maintaining or improving NOI to meet these thresholds can be difficult, leading to tighter cash flow margins. Investors and property managers must focus on operational efficiency and strategic rent increases where feasible to sustain or improve cash flows.

Moreover, the premiums associated with hard money and bridge loans have widened due to the current rate environment. Rates for these short-term financing solutions typically range from 8% to 12%, reflecting the higher risk and flexibility they offer. These loans become attractive options for investors needing to quickly close deals or reposition properties, though the higher interest burdens necessitate a clear exit strategy. Understanding the cost implications and structuring investments with a timeline for refinancing into lower-cost, long-term debt is crucial in utilizing these loans effectively.

Given the current interest rate environment, investors face strategic decisions regarding refinance timing versus hold strategies. With the expectation of potential future rate stabilization, some investors may opt to hold existing financing, especially if locked in at lower rates from previous years. Conversely, properties with impending loan maturities or those acquired at higher rates might consider refinancing to mitigate interest rate risks. The decision hinges on market forecasts, property performance, and the investor’s financial strategy.

These financing conditions inevitably impact acquisition criteria and underwriting standards. Investors are increasingly cautious, focusing on properties with strong cash flow histories and robust market fundamentals. Underwriting standards have tightened, with more rigorous stress-testing of income streams and careful consideration of vacancy rates and expense growth. Ultimately, the financing environment of March 2026 demands thorough due diligence and strategic financial planning to ensure investment viability and resilience.

## Investment Strategy & Risk Management

In the current market landscape of March 2026, investors must navigate a complex interplay of factors to optimize their real estate investment strategies. With interest rates stabilizing after a period of volatility, there is a distinct window of opportunity for acquisitions, particularly in under-valued or emerging markets. The key to successful market timing lies in identifying opportunities where property values have yet to fully rebound from previous downturns. Investors should focus on areas with strong economic fundamentals and demographic trends indicating growth potential. This approach allows for capitalizing on appreciation as markets normalize.

However, the current environment is not without its risks. The potential for economic fluctuations, changes in interest rates, and evolving market dynamics necessitate a proactive risk management framework. Investors should prepare for these uncertainties by diversifying their portfolios across asset classes and geographies. Incorporating stress testing into underwriting processes ensures that assumptions remain robust under various scenarios. Additionally, maintaining a flexible capital reserve can cushion against unforeseen expenses or market shifts, preserving liquidity and operational capability.

Adjusting acquisition criteria and underwriting standards is critical in this climate. Given the heightened importance of cash flow stability, investors should prioritize properties offering strong cap rates and positive cash-on-cash returns. This focus on income-producing assets minimizes exposure to market volatility. Furthermore, refining underwriting standards to include more conservative assumptions on rent growth and occupancy rates can provide a margin of safety. Ensuring that Debt Service Coverage Ratios (DSCR) exceed minimum thresholds is essential for sustaining financial health in a fluctuating market environment.

Ultimately, the strategic focus for investors should be on leveraging market insights to optimize property acquisition and management. By adopting a disciplined approach to market timing, risk mitigation, and underwriting adjustments, investors can enhance their portfolios’ resilience and profitability.

### Key Considerations for Investors

- Fix-and-Flip Strategies: Limit holding costs to a maximum of 3% of the property’s ARV (After Repair Value) to reduce financial strain during renovation periods.

- Spread Risk: Target properties with a minimum spread of 20% between purchase and projected sale price to buffer against market swings.

- Exit Timing: Plan for multiple exit strategies, including rental conversion, to mitigate selling risks if the market softens.

- Buy-and-Hold Tactics: Aim for cap rates above 6% to ensure competitive cash flow in a stable market.

- Rent Growth Assumptions: Use conservative estimates of 2-3% annual rent growth when forecasting long-term cash flows.

- Bridge Financing: Secure flexible draw schedules to align with project milestones, minimizing interest accrual.

- Contingency Reserves: Maintain reserves covering at least 6 months of operating expenses to safeguard against unforeseen disruptions.

- Geographic Focus: Prioritize markets in the Southeast and Midwest for optimal risk-adjusted returns, given their economic stability and growth potential.

- Conservative Underwriting: Stress test scenarios with a 10% drop in rental income and a 1% increase in vacancy rates to ensure investment durability.

- Portfolio Diversification: Balance asset class mix with no more than 30% concentration in any single asset type to mitigate sector-specific risks.

By focusing on these strategic areas, investors can confidently navigate the real estate market, leveraging opportunities while effectively managing associated risks.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.