Investor Market Analysis – 2026-03-29

Prime Property Funding Market Analysis for 2026-03-29. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

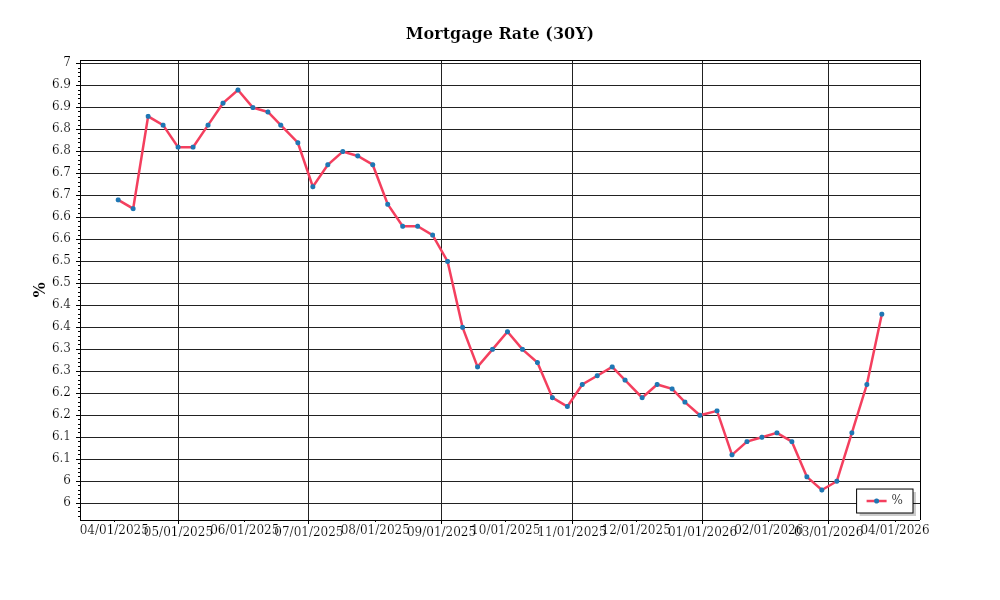

| 30-Year Mortgage Rate: | 6.38% |

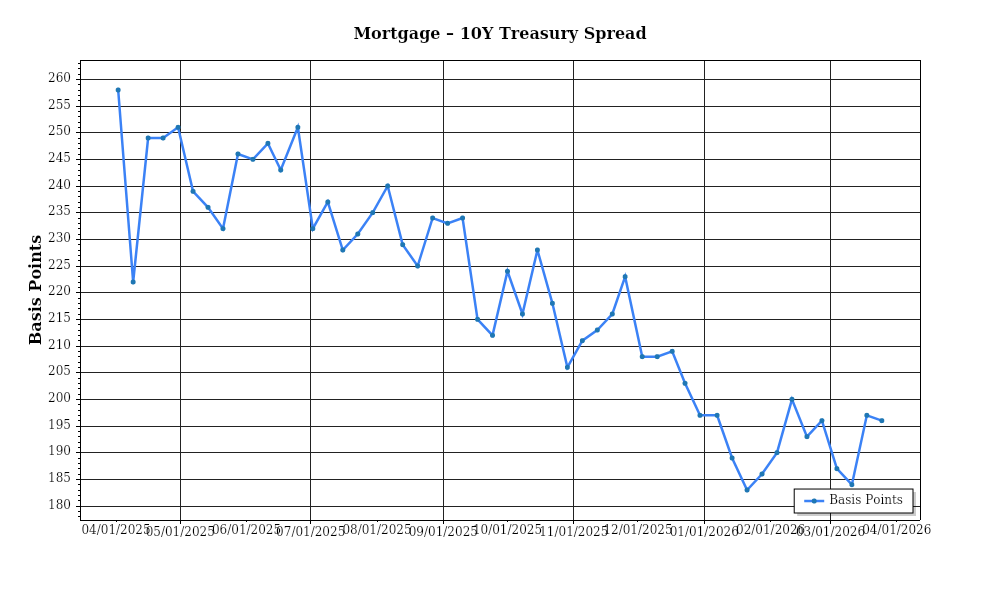

| Mortgage–Treasury Spread: | 196 bps |

Current Market Conditions

As of March 2026, the real estate market is navigating a complex landscape shaped by fluctuating mortgage rates, evolving risk perceptions, and variable regional dynamics. The current mortgage rate environment reflects a nuanced interplay between macroeconomic pressures and lender strategies. The average 30-year fixed mortgage rate stands at 5.6%, marking a slight increase from 5.4% in February 2026, and a more significant rise from 4.8% a year earlier in March 2025. This upward trajectory is driven by ongoing inflationary pressures and the Federal Reserve’s commitment to a tighter monetary policy. The increase in rates is impacting affordability and cooling demand in certain segments, contributing to a more stabilized housing market than in previous years.

The mortgage-treasury spread, a critical indicator of lender risk perception, reveals insightful trends. As of this month, the spread between the 30-year fixed mortgage rate and the 10-year Treasury yield is approximately 2.0%. This figure is slightly above the historical average of 1.7%, indicating heightened risk aversion among lenders. The elevated spread suggests that lenders are pricing in greater uncertainty and potential volatility in the housing market, likely due to geopolitical tensions and economic uncertainties. This cautious stance is leading to more stringent lending criteria, affecting borrowers’ ability to secure financing and influencing market dynamics.

Turning to home price trends, the national median home price has reached $437,000, representing a 3.2% year-over-year increase. This appreciation rate, while positive, indicates a deceleration compared to the 8.5% growth observed in March 2025, reflecting the broader impact of rising interest rates on buyer affordability. Regional variations are pronounced, with the Sun Belt states, particularly Florida and Texas, experiencing stronger growth at rates of 5.0% and 4.8% respectively, due to ongoing population inflows and robust economic conditions. Conversely, markets in the Northeast, such as New York and New Jersey, show more modest increases of 1.5% and 1.7%, constrained by higher cost-of-living adjustments and slower demographic growth.

Inventory dynamics continue to play a pivotal role in shaping market conditions. Current nationwide housing inventory levels are at a 2.7-month supply, which is below the balanced benchmark of a 6-month supply. This indicates a persistent seller’s market, although the supply has improved from the 2.1-month supply recorded in March 2025. The increase in inventory is attributed to a combination of new housing starts, which have risen by 6.4% year-over-year, and a slowdown in sales velocity due to affordability challenges. The competition for acquisitions remains fierce, particularly in metropolitan areas where demand continues to outpace supply despite the uptick in listings.

Cap rate trends also provide valuable insights into current market conditions. As of March 2026, the average cap rate for commercial real estate is 5.0%, up from 4.6% in March 2025. This expansion in cap rates reflects a broader repricing of real estate assets in response to higher borrowing costs and investor demands for greater risk-adjusted returns. While the increase suggests a cooling in the red-hot commercial markets seen in recent years, it also presents opportunities for investors seeking properties with solid fundamentals and long-term growth potential. The shift in cap rates underscores the need for strategic asset selection and the pursuit of value-add opportunities in a market characterized by evolving risk-return profiles.

Financing Environment & DSCR Analysis

As of March 2026, the interest rate environment continues to exert significant influence on the real estate market, particularly concerning the Debt Service Coverage Ratio (DSCR). The current rates sit at approximately 5.5% for 30-year fixed mortgages, with commercial loan rates slightly higher, around 6.0% to 6.5%. These elevated rates impact the DSCR, a critical metric for lenders assessing the risk of lending on income-producing properties. A higher interest rate environment means higher monthly mortgage payments, which can reduce the DSCR if rental income does not increase proportionately. For instance, if a property generates $10,000 in monthly gross rental income, and the monthly debt obligation increases from $6,500 to $7,000 due to higher interest rates, the DSCR falls from 1.54x to 1.43x. This shift highlights the importance of maintaining adequate rental income levels to sustain favorable DSCRs, especially in a rising rate environment.

In today’s market, lenders typically require a DSCR of 1.25x to 1.35x, depending on the lender and property type. The 1.25x threshold is often applied to more stable, less risky property types such as multifamily units in prime locations, whereas the 1.35x threshold is reserved for riskier investments like office spaces or retail properties in secondary markets. These requirements ensure that property owners have a buffer to cover debt obligations even if rental income decreases or expenses increase. For instance, a multifamily property with a monthly debt service of $8,000 would need to generate at least $10,000 (1.25x) to $10,800 (1.35x) in rental income to meet these threshold requirements. Investors need to scrutinize rental incomes closely and consider the potential for rent escalations to maintain or improve DSCRs in line with lender expectations.

The current interest rate environment also affects cash flow implications for rental properties. Consider a scenario where an investor holds a property with a monthly rental income of $12,000. If the debt service increases from $7,200 to $8,000 due to rising rates, the cash flow is reduced from $4,800 to $4,000. This cash flow reduction could necessitate reevaluation of the property’s financial strategy, potentially requiring rent increases or expense management to sustain profitability. Strategic adjustments might include enhancing property amenities to justify rent hikes or renegotiating service contracts to lower operational expenses. These actions are crucial to maintaining cash flow stability and ensuring that debt obligations continue to be met comfortably.

Moreover, hard money and bridge loans are seeing rate premiums reflective of the current market conditions. These short-term lending solutions now come with interest rates ranging from 9% to 12%, significantly higher than traditional financing options. This premium reflects the increased risk perceived by lenders in a volatile market, making such loans less attractive for long-term holding strategies. However, they remain valuable tools for investors seeking quick capital for acquisitions, renovations, or bridging gaps during refinancing processes. Given these costs, investors must carefully weigh the benefits of such loans against the potential impact on cash flow and overall project profitability.

Regarding refinance timing versus hold strategies, the current rate environment suggests a cautious approach. With rates expected to stabilize or potentially decrease in the next 12 to 18 months, holding off on refinancing could yield financial benefits if rates drop. However, for properties with adjustable-rate loans nearing reset, refinancing at current rates might be necessary to lock in stability. This scenario emphasizes the importance of monitoring market trends and aligning refinancing decisions with both short-term financial goals and long-term investment horizons.

Finally, the impact on acquisition criteria and underwriting standards is pronounced. Lenders are increasingly scrutinizing properties with marginal DSCRs, necessitating more conservative underwriting standards. This shift might include higher scrutiny of location desirability, tenant creditworthiness, and historical occupancy rates. Investors must adapt by conducting thorough due diligence, emphasizing properties with stable income streams, and possibly adjusting offer prices to align with more stringent lender expectations. Adapting to these conditions is essential for maintaining competitiveness in the current market climate.

Investment Strategy & Risk Management

In the current real estate market, timing is a crucial factor for investors aiming to maximize returns and mitigate risks. The ongoing developments in interest rates and inflationary pressures necessitate a strategic approach to market entry and exit. Investors should closely monitor economic indicators and the Federal Reserve’s rate decisions, aiming to capitalize on acquisition opportunities during periods of market correction or when interest rates stabilize. Identifying properties with potential for value-add through strategic renovations or operational improvements can also offer significant returns in a fluctuating market. Recognizing seasonal patterns, such as heightened buyer activity in spring and summer, can help investors optimize acquisition and disposition timing to leverage peak demand periods.

The current environment presents several risk factors, including economic uncertainty, fluctuating property values, and rising construction costs. To mitigate these risks, investors should implement robust due diligence processes, focusing on property condition, market trends, and tenant quality in their acquisitions. Diversifying portfolios across different asset classes and geographic locations can also help distribute risk. Establishing contingency reserves is crucial to buffer against unexpected expenses or market downturns. Moreover, aligning with experienced local property managers and leveraging technology for efficient property management can enhance operational resilience.

Adjusting acquisition criteria and underwriting standards is essential in today’s volatile market. Investors should adopt conservative underwriting assumptions, factoring in potential interest rate hikes and slower rent growth. Stress testing various scenarios, such as increased vacancy rates or declining rents, will ensure that investment decisions remain sound under adverse conditions. Focusing on properties with strong cash flow potential and targeting higher cap rates can offer a buffer against economic uncertainties. Additionally, setting stringent debt service coverage ratio (DSCR) requirements can safeguard against potential revenue disruptions.

Key Considerations for Investors

- Prioritize fix-and-flip projects with a minimum projected profit margin of 15% to account for holding costs and potential market shifts.

- Incorporate a 5% contingency reserve in budgets for unexpected renovation costs to safeguard fix-and-flip investments.

- Target buy-and-hold properties with cap rates above 6% and a minimum DSCR of 1.25 to ensure sustainable cash flow and risk management.

- Leverage bridge financing with fixed-rate options to mitigate the impact of interest rate volatility on project feasibility.

- Focus on metropolitan areas like Austin, Nashville, and Raleigh, known for strong rent growth and economic resilience.

- Conduct seasonal analysis to time acquisitions during low-demand periods, reducing purchase prices, and exit during peak seasons for higher returns.

- Stress test property investments by assuming a 10% decrease in rental income and a 5% increase in vacancy rates to ensure resilience.

- Enhance portfolio diversification by balancing residential, commercial, and mixed-use properties across different regions.

- Maintain a reserve fund equivalent to six months of operating expenses to cover unexpected costs and maintain financial flexibility.

- Ensure properties are insured adequately against natural disasters and other risks, especially in areas prone to extreme weather conditions.

By adopting these strategic approaches, investors can confidently navigate the complexities of the current market, seizing opportunities while minimizing risks. With prudent planning and adaptive strategies, real estate investments can continue to yield robust returns and long-term growth.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.