Investor Market Analysis – 2026-03-27

Prime Property Funding Market Analysis for 2026-03-27. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

| 30-Year Mortgage Rate: | 6.38% |

| Mortgage–Treasury Spread: | 205 bps |

Current Market Conditions

As of March 2026, the mortgage rate environment remains a critical factor influencing real estate investment decisions. The current average mortgage rate for a 30-year fixed loan is hovering around 6.25%, a significant increase from 4.75% reported in March 2025. This upward trend has been persistent over the past year, largely due to the Federal Reserve’s tightening monetary policy in response to inflationary pressures. The trajectory suggests further rate hikes, with market forecasts indicating potential stabilization only if inflation metrics show substantial improvement. This environment increases borrowing costs for buyers, potentially dampening demand and impacting home sales volume.

An analysis of the mortgage-treasury spread provides insights into lender risk perception. The spread between the 30-year mortgage rate and the 10-year Treasury yield currently stands at 2.15%, slightly above the historical average of 1.75%. This widened spread signals that lenders perceive a higher risk in the mortgage market, possibly due to economic uncertainty and expectations of continued volatility in interest rates. Such a spread suggests that lenders are building in additional risk premiums to safeguard against potential defaults, which could further tighten credit conditions and constrain borrower access to financing.

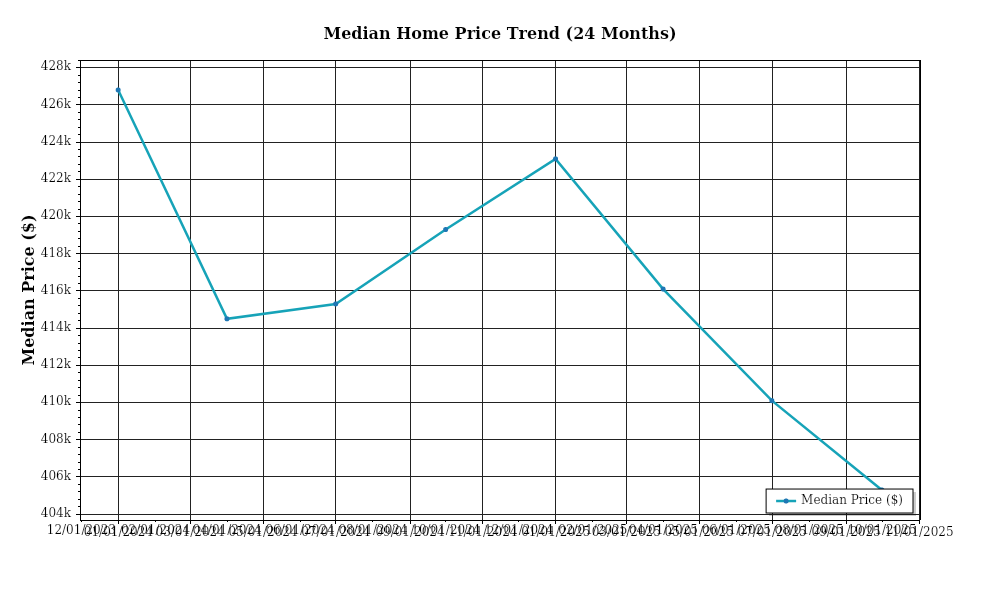

Turning to home price trends, the national median home price now stands at approximately $425,000, reflecting a year-over-year appreciation rate of 5.1%. While this indicates continued growth, the rate of appreciation has decelerated compared to the previous year’s 8.7%, pointing to a cooling market. Regionally, the West Coast, particularly cities like San Francisco and Los Angeles, has experienced modest appreciation rates of 2.5% due to affordability constraints, whereas Southeastern markets such as Atlanta and Charlotte have seen robust growth of 7.8% amid strong demand and lower baseline prices. This regional variation highlights shifting dynamics as affordability and migration patterns reshape local markets.

Inventory dynamics also play a pivotal role in current market conditions. The months of supply metric, which measures how long the current inventory would last at the current sales pace, is currently at 3.2 months, indicating a relatively balanced market, though slightly leaning towards a seller’s market. This is an increase from 2.6 months in March 2025, suggesting a gradual easing of the severe inventory constraints seen in prior years. However, competition for acquisitions remains intense, particularly in suburban areas where demand has surged due to hybrid work arrangements becoming more permanent. An increase in new construction starts, up by 7.4% year-over-year, could further alleviate supply pressures if sustained.

Cap rate trends provide a lens into the commercial real estate sector’s performance. Currently, average cap rates across major property types stand at 5.3%, up from 4.9% a year ago, indicating a mild expansion. This trend of yield expansion can be attributed to rising interest rates and investors demanding higher returns to offset increased financing costs. However, sectors such as industrial and multi-family have shown resilience with cap rates remaining relatively flat, at 4.7% and 4.5% respectively, driven by strong underlying demand fundamentals. On the other hand, retail and office properties have experienced more pronounced yield expansion, reflecting investor caution amid shifting consumer behaviors and remote work trends.

Overall, the current market conditions reflect a complex interplay of rising mortgage rates, lender risk perceptions, varied home price appreciation, evolving inventory levels, and nuanced cap rate movements. These factors collectively shape the landscape for real estate investments, requiring astute analysis and strategic foresight from investors navigating these dynamic times.

Financing Environment & DSCR Analysis

As of March 2026, the financing environment presents a dynamic landscape for real estate investors, particularly concerning interest rates and their effects on the Debt Service Coverage Ratios (DSCR). The current interest rates, influenced by the Federal Reserve’s monetary policy aimed at moderating inflationary pressures, hover around 5.5% for conventional loans. This environment poses challenges for investors to maintain favorable DSCRs, as higher rates increase monthly debt obligations, thus affecting the affordability and attractiveness of potential investments. A higher interest rate directly translates into elevated monthly debt service payments, thereby requiring properties to generate increased net operating income (NOI) to meet lender requirements.

In this rate environment, lenders typically set DSCR requirements between 1.25x to 1.35x. A DSCR of 1.25x signifies that the property generates 25% more income than is required to cover the debt service, while a 1.35x DSCR indicates a 35% surplus. Given the elevated interest rate, achieving these thresholds becomes more challenging, necessitating either increased rental income or reduced debt levels. The choice of DSCR threshold critically impacts the underwriting process; a higher DSCR requirement often necessitates more conservative income assumptions and stricter underwriting standards, potentially limiting the pool of viable properties that meet these criteria.

For rental property investors, the implications of current DSCR requirements are significant. Consider a multi-family property with an annual debt service of $120,000. To satisfy a DSCR of 1.25x, the property must generate an NOI of at least $150,000. If the required DSCR is 1.35x, the NOI must increase to $162,000. This raises the bar for property performance and necessitates a deeper focus on operational efficiencies and rental rate adjustments to ensure compliance with lender expectations. Investors face pressure to optimize property management and tenant retention strategies to maintain or boost NOI, which is crucial for both existing portfolios and prospective acquisitions.

In the current market, hard money and bridge loan rate premiums reflect the increased risk and cost of capital. Such loans typically carry interest rates 2-4 percentage points above conventional financing, often ranging from 7.5% to 9.5%. These loans, while more expensive, provide flexibility for acquisitions requiring rapid closing or properties needing significant rehabilitation. However, the premium necessitates careful consideration of exit strategies to ensure profitability. Investors employing these financing options must diligently plan for refinancing or sale to mitigate the cost impact of these higher rates.

The decision to refinance or hold properties is influenced by the prevailing rate environment. With interest rates projected to stabilize or potentially decrease as inflationary pressures ease, investors must weigh the benefits of locking in current rates against the possibility of more favorable terms in the future. A refinance strategy might be advantageous if it leads to improved cash flow through reduced payments, even at the expense of extending loan maturity. Conversely, a hold strategy could be prudent if current rates are deemed unsustainable and likely to decline, preserving equity and avoiding prepayment penalties.

Ultimately, the current financing environment necessitates a recalibration of acquisition criteria and underwriting standards. Investors must adjust their investment models to account for higher debt costs and stricter DSCR requirements, focusing on properties with robust income potential and value-add opportunities. Enhanced due diligence processes, including stress testing for interest rate variability and market downturns, become essential. This conservative approach ensures that acquisitions remain viable and profitable amidst evolving economic conditions, safeguarding investor equity and returns.

Investment Strategy & Risk Management

In the current real estate environment, market timing is paramount for maximizing returns, especially for investors dealing with hard money loans, fix-and-flip projects, and DSCR loans. As of March 2026, the market exhibits signs of stabilization following a period of volatility. This presents a prime opportunity for investors to capitalize on value acquisitions. Identifying properties in transitional neighborhoods where appreciation potential is high can yield substantial returns. The key is to remain vigilant about local market trends and to leverage data analytics to pinpoint the optimal entry and exit points.

Risk factors in the current environment include fluctuating interest rates, potential economic slowdowns, and supply chain disruptions impacting renovation schedules and costs. To mitigate these risks, investors should adopt a multi-faceted approach. This includes locking in interest rates where possible to avoid unexpected hikes, diversifying portfolios across different asset classes and geographic locations, and maintaining adequate liquidity reserves for unforeseen expenses. For fix-and-flip ventures, having a comprehensive contingency plan for holding costs and exit strategies is essential to adapt to market shifts.

Adjusting acquisition criteria and underwriting standards is critical to navigating the present market landscape. Investors should refine their criteria to focus on properties with strong cash flow potential and favorable cap rates. Underwriting standards must be stringent, incorporating stress tests that account for potential downturns in rent growth or property values. It’s vital to ensure that DSCR loans are structured with ample cushions to withstand minor revenue fluctuations without default risk.

For Prime Property Funding, the current climate necessitates a strategic pivot towards conservative yet opportunistic investment strategies. By prioritizing high-quality assets with low leverage and focusing on markets with robust economic fundamentals, investors can enhance their risk-adjusted returns. The focus should be on diligent due diligence, comprehensive market analysis, and flexible exit strategies to maximize profitability.

Key Considerations for Investors

- Fix-and-flip strategies: Ensure holding costs do not exceed 10% of the projected after-repair value (ARV) and maintain a spread risk analysis to evaluate potential profit margins.

- Exit timing: Plan for a sale timeline of 6-9 months to account for potential market shifts and ensure liquidity.

- Buy-and-hold tactics: Target a minimum cap rate of 6% in growth markets to ensure viable long-term returns, and set rent growth assumptions at a conservative 2-3% annually.

- DSCR cushions: Maintain a DSCR of at least 1.25 to provide a buffer against income variability and ensure loan servicing capacity.

- Bridge financing: Monitor the rate environment closely and negotiate flexible draw schedules to manage cash flow during the renovation phase.

- Contingency reserves: Keep contingency reserves at 10-15% of project costs to cover unexpected expenses.

- Market timing: Prioritize acquisitions in Q2 and Q3 when market activity and property values typically peak.

- Geographic focus: Focus on secondary markets such as Austin, Nashville, and Raleigh, which offer higher risk-adjusted returns due to robust economic growth.

- Conservative underwriting: Conduct stress testing on cash flow projections with a 5-10% variance to account for market fluctuations.

- Portfolio diversification: Balance the portfolio with a mix of residential, commercial, and mixed-use properties across at least three different states to mitigate localized risks.

By implementing these strategies and staying informed about market conditions, investors can confidently navigate the real estate landscape and achieve superior returns. With foresight and adaptability, opportunities abound even in uncertain times.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.