Investor Market Analysis – 2026-03-21

Prime Property Funding Market Analysis for 2026-03-21. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

| 30-Year Mortgage Rate: | 6.22% |

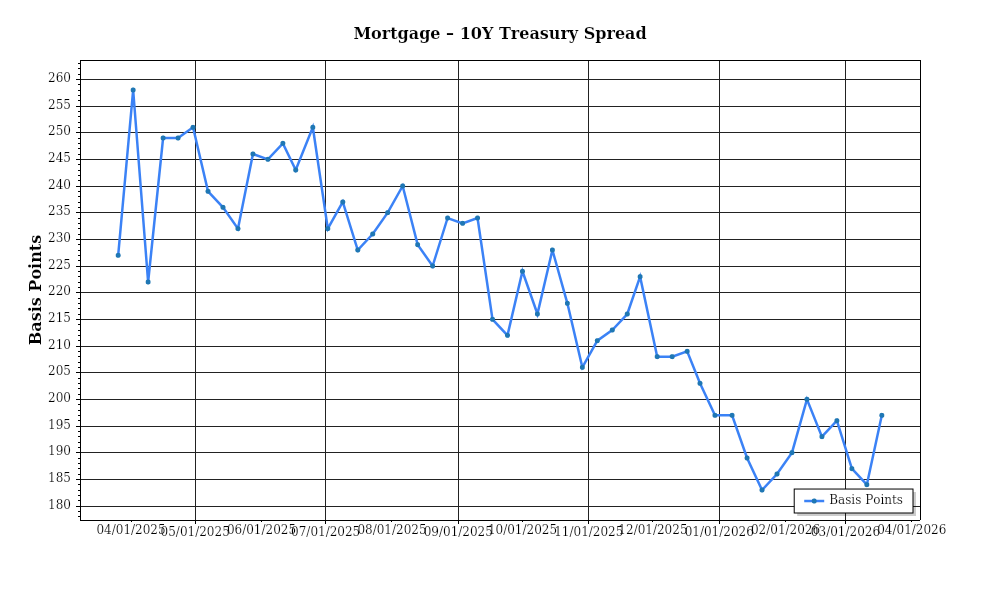

| Mortgage–Treasury Spread: | 197 bps |

Current Market Conditions

As of March 2026, the real estate market is navigating a complex landscape shaped by a combination of macroeconomic factors, regional disparities, and shifting buyer dynamics. A critical component influencing the market is the mortgage rate environment. Currently, the average 30-year fixed mortgage rate stands at 5.35%, which marks a slight increase from 4.85% in March 2025. This uptick reflects a broader trend observed over the past 18 months, where rates have gradually climbed from historic lows observed during the pandemic years. The Federal Reserve’s recent decisions to maintain a cautious yet steady approach to interest rate hikes have contributed to this trajectory, with the central bank’s benchmark rate now at 2.50%. These rising mortgage rates are exerting upward pressure on monthly payments, potentially dampening buyer enthusiasm, especially among first-time homebuyers.

The mortgage-treasury spread, a key indicator of lender risk perception, currently averages around 1.75%. This figure represents the difference between the average mortgage interest rate and the yield on 10-year U.S. Treasury bonds, which presently stands at 3.60%. A rising spread, as observed over the past several months, typically signals increased risk aversion among lenders, often due to economic uncertainties or anticipated market volatility. The current spread is higher than the long-term average of approximately 1.50%, suggesting that lenders are factoring in heightened risks, possibly due to geopolitical tensions, economic slowdown concerns, or expectations of future rate volatility. This risk sensitivity can lead to tighter lending standards, impacting borrowers’ ability to secure financing.

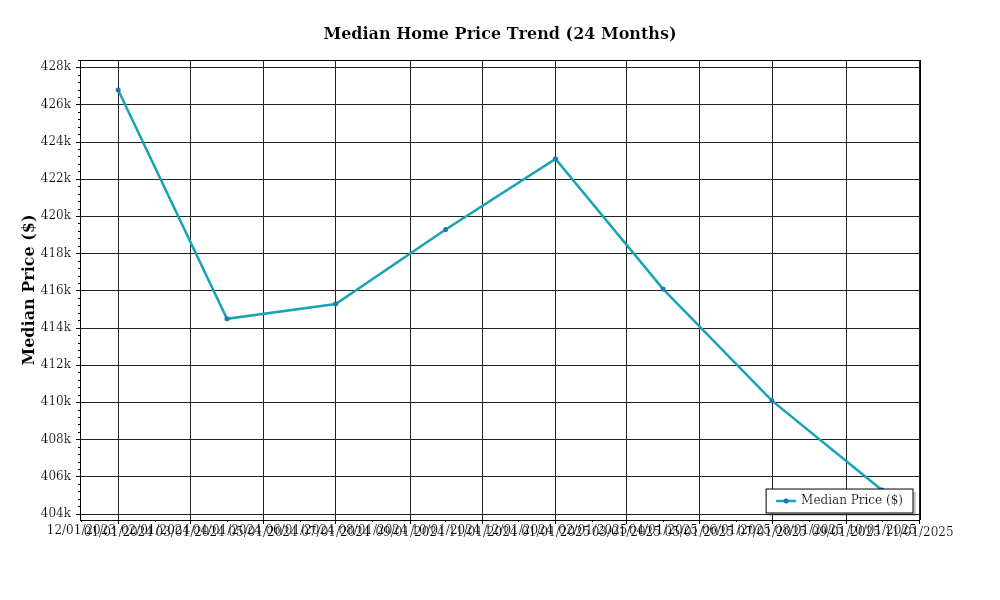

Median home prices continue to show robust growth, albeit with notable regional variations. Nationally, the median home price has reached $412,000, reflecting an annualized appreciation rate of 7.2%, down from the double-digit growth rates seen during the pandemic-fueled market frenzy. Regions like the Southeast and Mountain West are experiencing higher appreciation rates, with cities such as Austin and Nashville recording increases of 9.5% and 8.3%, respectively. Conversely, the Northeast, with a more mature market and higher baseline prices, shows slower growth, with cities like Boston seeing a modest 4.1% increase. These regional disparities highlight the influence of local economic conditions, population movements, and supply constraints on home prices.

Inventory dynamics remain a critical factor in understanding the current market balance. Nationally, the housing supply is estimated at 2.3 months, indicating a seller’s market, as a balanced market typically requires a supply of around 6 months. This limited inventory is driving competition among buyers, with multiple-offer scenarios still prevalent in desirable markets. However, new listings have shown a slight uptick, rising by 5% year-over-year, suggesting that some homeowners are capitalizing on high prices. This modest increase in supply is insufficient to fully alleviate competitive pressures, but it may contribute to a gradual stabilization of the market.

Finally, cap rate trends reveal insights into investment property yields and market sentiment. Currently, the average cap rate for multifamily properties stands at 4.7%, reflecting a slight compression from 5.1% a year ago. This compression indicates strong investor demand and expectations of continued rental income growth, despite rising financing costs. However, in the office and retail sectors, cap rates are experiencing slight expansion, with current averages at 6.2% and 6.8% respectively, up from the previous year’s 5.9% and 6.5%. This divergence is due to ongoing challenges in these sectors, such as remote work trends impacting office space demand and e-commerce growth affecting retail. Yield compression in multifamily and selective expansion in office and retail suggest a nuanced investor outlook, prioritizing sectors perceived as resilient or poised for recovery.

Financing Environment & DSCR Analysis

The current interest rate environment as of March 2026 presents unique challenges and opportunities for real estate investors, particularly in relation to Debt Service Coverage Ratios (DSCR). With average interest rates on conventional loans hovering around 6.5%, there is significant pressure on DSCR calculations, which can directly impact an investor’s ability to secure financing. A higher interest rate environment generally means higher monthly debt obligations, thereby reducing the DSCR. For example, consider a property generating a monthly net operating income (NOI) of $10,000. At the current interest rate, the monthly debt payment might be approximately $8,000, resulting in a DSCR of 1.25x. This figure is at the lower end of acceptable thresholds, making it crucial for investors to either increase NOI or seek properties with more favorable financing terms to maintain financial viability.

In this market, typical DSCR requirements are becoming more stringent. While a DSCR of 1.25x was once a standard benchmark, lenders are increasingly shifting towards a 1.35x threshold to mitigate risk. This adjustment means that properties must now produce $1.35 in NOI for every $1 in debt service. This shift is particularly impactful for properties with thinner margins or those in markets with slower rent growth. Investors must conduct thorough financial due diligence to ensure their properties can meet these elevated requirements, potentially necessitating higher down payments or seeking properties with lower acquisition costs to improve their financing prospects.

The implications of these DSCR requirements are significant for cash flow and rental properties. For instance, if an investor purchases a property for $1 million with a $750,000 loan at a 6.5% interest rate, the monthly debt service is approximately $4,740. To achieve a DSCR of 1.35x, the property must generate at least $6,399 in monthly NOI. This requirement could mean increasing rents or reducing operational expenses to ensure compliance. For properties that fall below this threshold, investors might face challenges in securing favorable terms or refinancing options, impacting overall profitability and investment strategy.

In the current market, hard money and bridge loan rates carry significant premiums, often ranging from 8% to 12%, reflecting the increased risk lenders perceive in the current economic climate. These loans, while offering quicker access to capital, require careful consideration due to their higher costs. They are typically used for short-term financing solutions, such as property flips or renovations, and necessitate a clear exit strategy to avoid eroding potential profits. Investors must weigh the benefits of rapid capital deployment against the high-interest costs and assess whether the potential returns justify the financial outlay.

The decision between refinance timing versus hold strategies is particularly nuanced in this rate environment. While refinancing could lock in lower rates when market conditions improve, the current rates suggest a more cautious approach. Holding onto existing financing with lower rates from previous years might be more advantageous until interest rates stabilize or decrease. This strategy requires investors to remain vigilant in monitoring market trends and be prepared to act swiftly when conditions become favorable. The potential for rate cuts in the near future could make refinancing a more attractive option, but timing is critical to maximize benefits.

Finally, these financial conditions necessitate a reevaluation of acquisition criteria and underwriting standards. Lenders are increasingly conservative, emphasizing strong cash flow, low vacancy rates, and stable tenant profiles. Underwriting processes are more rigorous, with a greater focus on stress testing financial scenarios to ensure properties can withstand economic fluctuations. Investors must adapt by prioritizing properties with strong fundamentals and resilient market characteristics, ensuring that their portfolios remain robust despite the challenging financing environment.

Investment Strategy & Risk Management

In the current real estate climate, characterized by fluctuating interest rates and evolving market conditions, **market timing** is crucial for maximizing returns. Investors should be vigilant in identifying opportunities where property values are temporarily depressed due to macroeconomic factors, such as regional economic slowdowns or increased interest rates. The window for potential acquisitions may be brief as market corrections can occur swiftly. Therefore, maintaining readiness to move quickly on acquisitions that meet investment criteria is key. Additionally, seasonal patterns, such as a dip in activity during colder months, can present buying opportunities at favorable prices.

In this environment, **risk factors** such as interest rate volatility, inflation pressures, and potential economic downturns necessitate robust risk management strategies. Effective **mitigation strategies** include maintaining a conservative debt profile, ensuring properties are adequately insured, and having contingency plans for cost overruns or extended holding periods. Stress testing financial models against various economic scenarios can also help investors prepare for unforeseen shifts. Additionally, diversifying property portfolios across asset classes and geographic regions can help spread risk and smooth returns.

Adjusting **acquisition criteria and underwriting standards** is imperative in uncertain times. Investors should prioritize properties that offer strong cash flow potential and higher **cap rates** to buffer against economic fluctuations. Enhanced due diligence, including thorough market analysis and tenant quality assessments, is essential to uncover hidden risks. Underwriting standards should be stringent, incorporating higher **DSCR (Debt Service Coverage Ratio) cushions** and conservative rent growth assumptions to ensure resilience against market shocks.

Key Considerations for Investors

- Fix-and-flip strategies: Prioritize properties with at least a 20% anticipated profit margin to account for potential holding cost overruns and market fluctuations.

- Implement strict exit timing strategies to minimize market exposure, targeting renovations that can be completed within six months to limit holding costs.

- Set cap rate targets for buy-and-hold investments at a minimum of 6% to ensure adequate returns in a rising interest rate environment.

- Underwrite with conservative annual rent growth assumptions of 2-3% to buffer against economic unpredictability.

- Ensure bridge financing options offer flexible draw schedules and maintain contingency reserves of at least 10% of project costs.

- Monitor the rate environment closely and structure financing with fixed rates where possible to mitigate interest rate risk.

- Consider **geographic focus** on markets with strong employment growth and demographic trends, such as the Southeast and Southwest, which offer better risk-adjusted returns.

- Incorporate stress testing in underwriting to assess property performance under adverse economic conditions.

- Balance portfolios with a mix of asset classes, targeting a blend of residential and commercial properties to diversify income streams.

- Mitigate risks with adequate reserves, insurance coverage, and by maintaining high tenant quality and ensuring properties are in excellent condition to minimize vacancy and repair costs.

By adopting these strategic adjustments and maintaining a disciplined approach, investors can navigate the complexities of the current market with greater confidence and resilience. The key is to remain adaptable, vigilant, and proactive in managing both opportunities and risks.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.