Investor Market Analysis – 2026-03-20

Prime Property Funding Market Analysis for 2026-03-20. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

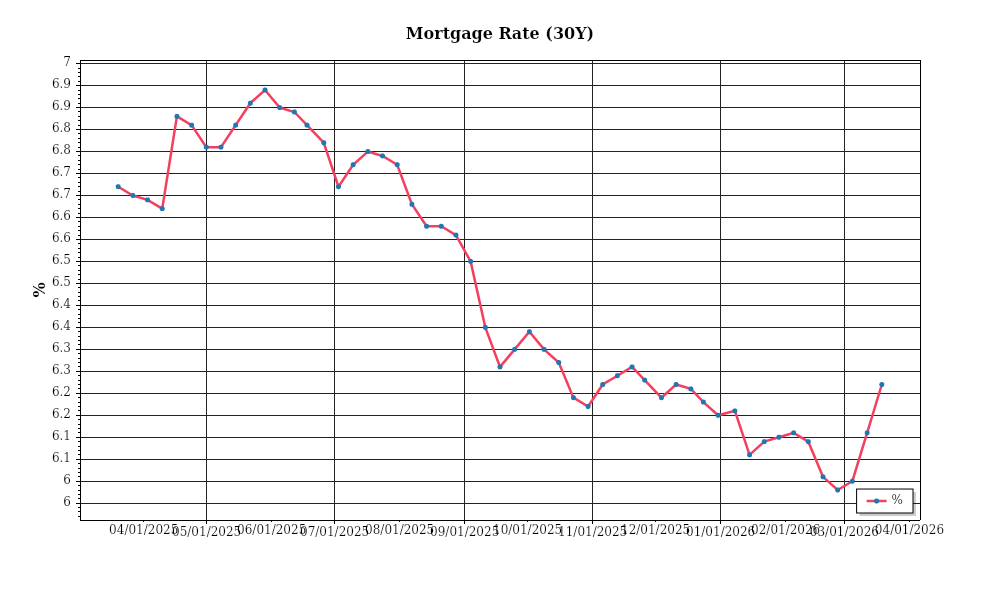

| 30-Year Mortgage Rate: | 6.22% |

| Mortgage–Treasury Spread: | 196 bps |

Current Market Conditions

As of March 2026, the mortgage rate environment remains a pivotal factor influencing the real estate market. The average 30-year fixed mortgage rate currently stands at 5.75%, reflecting a notable increase from 4.5% a year ago. This uptick aligns with the Federal Reserve’s tightening monetary policy, which has seen the federal funds rate rise in response to persistent inflationary pressures. Over the past six months, rates have stabilized somewhat, hovering between 5.5% and 6%. The trajectory indicates a cautious balancing act by the Fed, aiming to control inflation without stalling economic growth. For investors, this means a tighter borrowing landscape, potentially cooling demand in the housing sector.

The mortgage-treasury spread offers additional insights into lender risk perceptions. Currently, the spread between 30-year mortgage rates and the 10-year treasury yield is approximately 180 basis points, a slight increase from the historical average of 150 basis points. This wider spread suggests that lenders are pricing in greater risk, likely due to economic uncertainty and potential borrower defaults. The elevated spread signals caution, as lenders anticipate potential volatility in the housing market. For investors, this heightened risk perception could influence financing costs and overall returns.

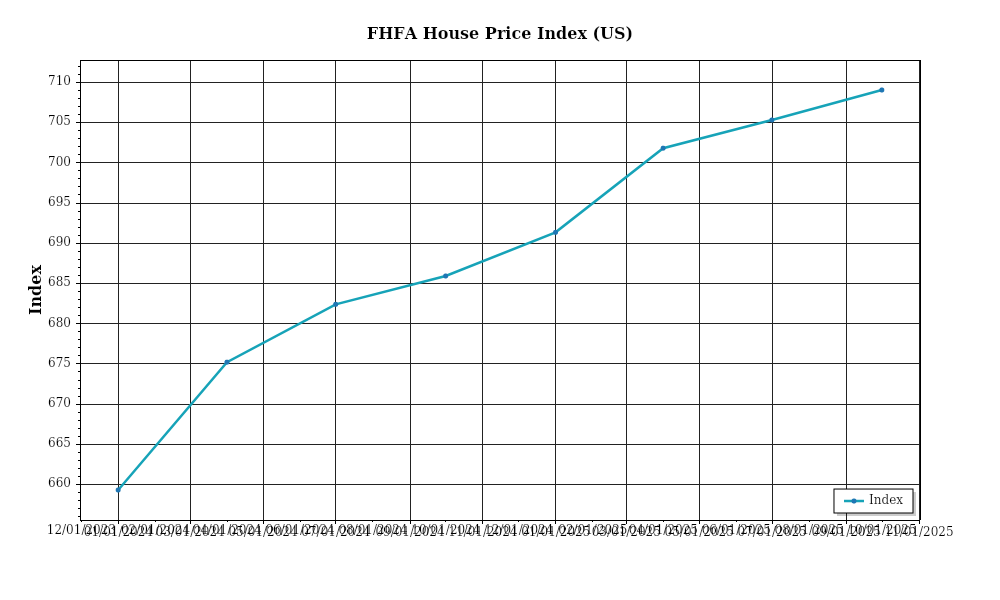

Turning to median home price trends, there’s been a modest appreciation over the past year. The national median home price reached $425,000 in March 2026, up from $410,000 in March 2025, marking a 3.66% year-over-year increase. This rate of appreciation represents a deceleration from the 6.5% increase observed in the preceding year. Regionally, the Southern United States continues to exhibit robust growth, with median prices in markets like Austin and Nashville climbing by 5% and 6%, respectively. Conversely, traditionally high-cost markets like San Francisco and New York have seen more muted growth, with price increases of 1.5% and 2%, reflecting affordability constraints and a shift in buyer preferences towards more affordable locales.

Inventory dynamics remain a critical component of the current market conditions. National inventory levels are slightly improved, with a 2.8-month supply as of March 2026, up from 2.5 months a year earlier. Despite this incremental increase, the market remains undersupplied relative to the balanced market threshold of 5-6 months of inventory. Competition for acquisitions remains fierce, particularly in desirable suburban and exurban areas where supply constraints are most pronounced. This limited inventory continues to support price stability but contributes to extended bidding wars and rapid transactions, posing challenges for new entrants and smaller investors.

Lastly, cap rate trends are offering mixed signals in the current environment. Average cap rates in the commercial real estate sector have compressed to 5.2%, down from 5.5% a year ago. This compression reflects sustained investor interest despite rising borrowing costs, driven by the search for yield in a low-interest-rate environment. However, the potential for cap rate expansion looms should interest rates continue to rise, which would increase financing costs and potentially depress property values. In practical terms, investors need to carefully assess the balance between acquisition costs and anticipated returns, particularly in markets where cap rate compression is most pronounced.

Overall, the current market conditions present a complex landscape for investors, characterized by rising interest rates, cautious lender sentiment, moderate home price appreciation, constrained inventory, and nuanced cap rate dynamics. Understanding these factors is essential for navigating the evolving real estate investment terrain.

Financing Environment & DSCR Analysis

As of March 2026, the financing landscape presents both opportunities and challenges for real estate investors, particularly in terms of managing debt service coverage ratios (DSCR). **Interest rates** remain a crucial factor influencing DSCR calculations. Currently, the average interest rate for commercial real estate loans hovers around 6.5%. This rate impacts the DSCR directly, as higher interest rates increase monthly debt obligations, thereby lowering the DSCR unless rental income rises proportionately. For instance, a property generating $100,000 in annual net operating income (NOI) with an annual debt service of $80,000 yields a DSCR of 1.25x. If interest rates rise, pushing debt service to $85,000, the DSCR drops to 1.18x, potentially below the acceptable threshold for many lenders.

In today’s environment, lenders typically require DSCRs between **1.25x and 1.35x**, with 1.25x being the minimum threshold for standard loan products and 1.35x often needed for less stable properties or those in secondary markets. This requirement reflects the increased risk lenders perceive in the current economic climate, with inflationary pressures and potential market volatility. The difference in these thresholds can significantly affect an investor’s financing options and property selection. Properties with higher DSCRs are more attractive to lenders, allowing for more favorable loan terms and potentially larger loan amounts. Conversely, properties on the lower end of the DSCR spectrum may face stricter underwriting criteria or higher interest rates.

The cash flow implications for rental properties in this environment are substantial. For example, consider a multifamily property with an NOI of $200,000 and a loan requiring a DSCR of 1.35x. The required annual debt service would be approximately $148,148. In a scenario where rental incomes decline or expenses increase, maintaining this DSCR becomes challenging without adjusting rents or improving operational efficiencies. Investors must be vigilant in managing expenses and exploring revenue-enhancing strategies to preserve cash flow and meet DSCR requirements. Failure to maintain adequate DSCR can lead to refinancing challenges or even loan default, particularly if property values decline or market conditions deteriorate.

In the current market, **hard money and bridge loans** carry significant rate premiums, often ranging from 9% to 12%, reflecting the higher risk associated with these short-term financing solutions. These loans are typically used for properties undergoing repositioning or in transitional phases. Given these higher rates, investors need to carefully consider the cost-benefit ratio of using such financing, as the cost of capital can quickly erode profit margins. However, for projects with high upside potential or those requiring fast execution, these loans provide necessary flexibility.

Given this rate environment, investors face strategic decisions regarding **refinance timing versus hold strategies**. With interest rates forecasted to remain stable or rise slightly, refinancing existing debt at current rates could lock in costs before any further increases. However, holding existing low-rate loans until market conditions improve might be advantageous if refinancing terms are unfavorable. Investors should conduct a detailed analysis of projected cash flows, potential interest rate movements, and property-specific factors to determine the optimal strategy.

Finally, the current financing environment impacts **acquisition criteria and underwriting standards**. With tighter DSCR requirements and higher interest rates, investors need to adjust their acquisition criteria to focus on properties with robust cash flows and potential for rent growth. This may involve prioritizing properties in high-demand markets or those with value-add opportunities that can enhance income streams. Underwriting standards have become more stringent, with lenders scrutinizing income stability, tenant mix, and market conditions more closely. Investors must be prepared with comprehensive financial analyses and thorough market studies to support their acquisition proposals and secure favorable financing terms.

Investment Strategy & Risk Management

In the evolving real estate landscape of 2026, identifying and capitalizing on market timing opportunities is crucial for maximizing returns. The current environment, characterized by moderate economic growth and fluctuating interest rates, necessitates a keen understanding of timing entry and exit points. For fix-and-flip investors, the strategy should center on swift execution to minimize holding costs and optimize profit margins. This involves leveraging predictive analytics to identify neighborhoods with rising property values and leveraging short-term market dips to acquire undervalued assets. Meanwhile, buy-and-hold investors should focus on markets with consistent rent growth and strong employment fundamentals to ensure steady income streams and potential appreciation.

Navigating risk factors in the current market requires a proactive approach. Interest rate volatility poses a significant challenge, especially for those relying on bridge financing or adjustable-rate loans. To mitigate this, investors should consider locking in fixed-rate loans where possible and maintaining liquidity reserves to cushion against unexpected rate hikes. Additionally, understanding local market dynamics, such as regulations and tax policy changes, can help investors anticipate and manage potential pitfalls. Diversifying geographically and across asset classes can further insulate portfolios from localized economic downturns.

Adjusting acquisition criteria and underwriting standards is paramount in today’s market. Investors should incorporate more conservative assumptions, such as lower rent growth projections and higher vacancy rates, to stress-test potential acquisitions. For hard money and DSCR financing, stricter underwriting standards with increased DSCR cushions can safeguard against income disruptions. It is also advisable to enhance contingency planning by setting aside additional reserves for unanticipated expenses and capital improvements, ensuring long-term asset stability.

In conclusion, while the real estate market presents challenges, it also offers significant opportunities for strategic investors. By refining acquisition strategies, enhancing risk management protocols, and adapting to economic shifts, investors can achieve robust returns. Prime Property Funding stands ready to support investors with tailored financing solutions that align with these strategic imperatives.

Key Considerations for Investors

- Fix-and-flip strategies: Aim for a minimum 25% gross profit margin to account for holding costs and unforeseen expenses. Execute projects within a 90-day turnover period to reduce spread risk.

- Buy-and-hold tactics: Target properties with a cap rate of at least 6% in markets with projected rent growth of 3-5% to ensure a positive cash flow and robust cash-on-cash returns.

- Bridge financing: Opt for structures with capped rates and clear draw schedules to manage cash flow effectively. Maintain a contingency reserve equivalent to 5% of the project’s total cost.

- Market timing: Prioritize acquisitions in late winter and early spring to leverage lower holding costs and benefit from seasonal demand upticks.

- Geographic focus: Focus on secondary markets with emerging job sectors, such as Austin and Raleigh, which offer best risk-adjusted returns.

- Conservative underwriting: Implement stress tests by increasing assumed interest rates by 2% and reducing expected rent growth by 1-2% to evaluate deal resilience.

- Portfolio diversification: Balance portfolios with a 50/50 mix of residential and commercial properties spread across at least three distinct geographic regions.

- Risk mitigation: Maintain liquidity reserves covering at least 6 months of operating expenses and prioritize properties with strong tenant quality and solid structural condition.

- Insurance: Ensure comprehensive coverage, including flood and earthquake insurance where applicable, to protect against natural disasters.

- Tenant quality: Implement rigorous screening processes, requiring a minimum credit score of 650 and verified income that is at least 3 times the monthly rent.

With these strategies, investors can confidently navigate the complexities of the current market while optimizing their investment outcomes.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.