Investor Market Analysis – 2026-03-13

Prime Property Funding Market Analysis for 2026-03-13. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

| 30-Year Mortgage Rate: | 6.11% |

| Mortgage–Treasury Spread: | 190 bps |

Current Market Conditions

As of March 2026, the real estate market is characterized by several dynamic factors influencing investments. The current mortgage rate environment remains pivotal, with the average 30-year fixed-rate mortgage standing at 5.75%. This represents a significant hike from the 4.25% rate recorded in March 2025, reflecting a steady upward trend over the past 12 months. Several factors contribute to this increase, including the Federal Reserve’s monetary policy aimed at curbing inflation and stabilizing the broader economy. The upward trajectory of mortgage rates has implications for borrowing costs, with potential homebuyers facing higher interest expenses, thereby potentially dampening demand in certain segments of the housing market.

Examining the mortgage-treasury spread provides further insights into lender risk perceptions. As of this month, the spread between the 30-year mortgage rate and the 10-year Treasury yield is approximately 250 basis points. Historically, a spread above 200 basis points indicates heightened risk aversion among lenders, suggesting concerns about future economic conditions and borrower creditworthiness. This spread has widened from 180 basis points one year ago, highlighting increased caution in the lending environment. The implications for investors are manifold, as a wider spread may signal tighter credit conditions and potentially impact the pace of real estate transactions.

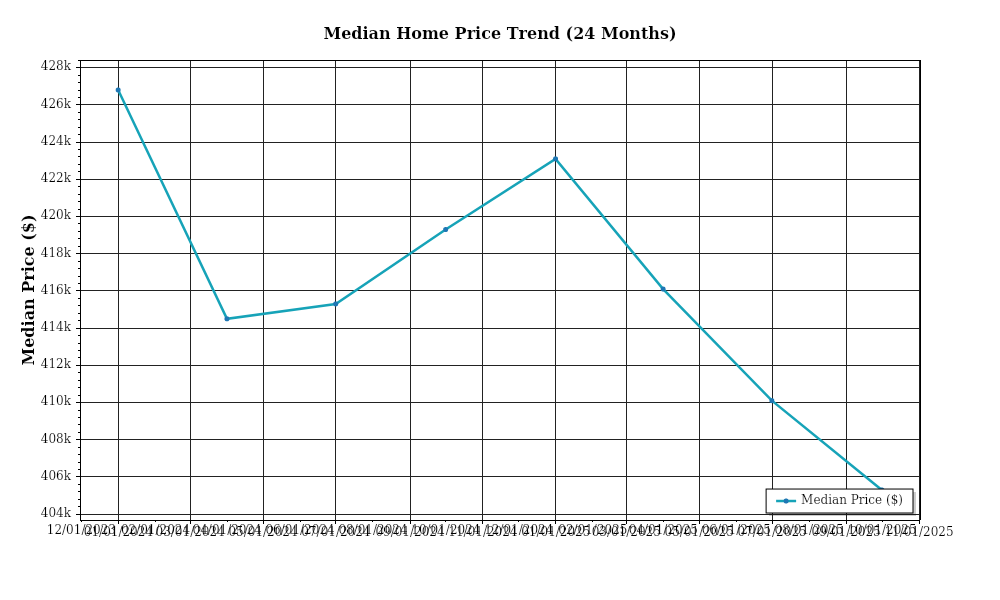

The median home price across the United States has experienced an impressive appreciation rate, currently standing at $420,000, up from $396,000 in March 2025. This 6.1% year-over-year increase underscores the ongoing demand for residential properties despite rising interest rates. However, regional variations are significant. The West Coast continues to lead with a median price of $640,000, while the Midwest remains more affordable at $280,000. These disparities reflect differing economic conditions, job markets, and local housing supply dynamics. Investors should be aware of these regional nuances, as they present both opportunities and challenges depending on specific market conditions.

Inventory dynamics are a crucial aspect of the current market. Nationally, housing inventory levels have risen slightly, with a current supply of 2.5 months. This is up from 2.2 months last year, indicating a modest easing of the tight supply conditions that have characterized recent years. However, the market remains tilted towards sellers, with competition for acquisitions still robust, particularly in high-demand urban centers. The balance between supply and demand continues to be a critical determinant of pricing power and negotiation leverage in real estate transactions.

Cap rate trends are another vital metric for investors focusing on commercial real estate. As of March 2026, average cap rates have compressed slightly to 5.0%, down from 5.3% last year. This compression reflects the strong investor appetite for real estate assets, driven by the search for yield in a low-interest-rate environment. Yield compression suggests that investors are willing to accept lower returns in exchange for perceived stability and security in real estate investments. However, this trend also means that finding high-yield opportunities requires more diligent market analysis and may involve greater risk.

In conclusion, the current real estate market is shaped by rising mortgage rates, cautious lender behavior, regional price variations, slightly improving inventory levels, and ongoing cap rate compression. These factors collectively influence investment strategies and risk assessments, requiring investors to navigate a complex landscape with a keen understanding of underlying economic and regional dynamics.

Financing Environment & DSCR Analysis

The current interest rate environment, as of March 2026, presents a complex landscape for real estate investors focusing on debt service coverage ratios (DSCR). With the Federal Reserve maintaining a cautious stance, interest rates have stabilized around 5.5% for conventional loans, influencing the financing strategies and cash flow projections for rental property investments. The DSCR, a critical measure of an asset’s ability to cover debt obligations, is directly impacted by these rates. Higher interest rates increase the cost of borrowing, thereby inflating monthly debt service payments and potentially lowering the DSCR. For instance, a rental property with a net operating income (NOI) of $120,000 and an annual debt service of $100,000 yields a DSCR of 1.20x. Should interest rates elevate borrowing costs, reducing this ratio below the typical threshold, this could impede refinancing options and investment attractiveness.

In the current economic environment, lenders have generally set DSCR requirements between 1.25x and 1.35x, depending on the perceived risk and asset class. A DSCR of 1.25x might suffice for stable, well-located properties with high occupancy and reliable tenant bases. Conversely, lenders may demand a DSCR of 1.35x for higher-risk properties or those in less stable markets to buffer against potential income fluctuations. These thresholds ensure that properties can manage debt obligations while providing a cushion for unexpected financial stress. For investors, meeting these requirements often necessitates either negotiating lower purchase prices or securing higher rental incomes to support the necessary cash flow.

From a cash flow perspective, the implications of these DSCR requirements are significant. Consider a multi-family property with a purchase price of $2 million, generating an NOI of $150,000 annually. If financed at 5.5% over 25 years, the annual debt service would be approximately $133,000, yielding a DSCR of 1.13x. To achieve a more favorable DSCR of 1.25x, the investor would need to either increase NOI to $166,250 or reduce debt service through a larger equity investment or additional financing terms. This underscores the importance of rigorous financial modeling and tenant management strategies in optimizing cash flow to meet lender expectations and sustain property operations.

The current market also sees increased premiums for hard money and bridge loans, reflecting heightened risk perceptions and tighter liquidity conditions. Rates for these non-traditional loan products typically range from 9% to 12%, substantially higher than conventional financing. These loans, while offering flexibility and speed, can significantly impact cash flow calculations and must be carefully weighed against the benefits of rapid acquisition or repositioning strategies. Investors relying on such financing must ensure that properties can generate sufficient cash flow to cover the higher debt service and still meet minimum DSCR requirements.

Given the current rate environment, strategic decisions regarding refinance timing versus holding strategies are increasingly nuanced. For properties with current loans approaching maturity or unfavorable terms, refinancing may be prudent if it locks in more favorable interest rates and improves cash flow resilience. However, with rates potentially stabilizing or decreasing marginally, some investors may opt to hold existing financing arrangements, particularly if prepayment penalties are substantial or if imminent rate reductions appear likely.

The prevailing interest rates and DSCR requirements also impact acquisition criteria and underwriting standards. Investors are now more stringent in their financial analyses, emphasizing properties with strong, predictable cash flows and robust tenant profiles. Underwriting standards have tightened, with increased scrutiny on NOI projections, market conditions, and tenant quality to ensure that potential acquisitions align with lender requirements and investor return expectations. This environment necessitates a disciplined approach to evaluating new opportunities, ensuring that properties are not only viable under current conditions but also resilient to potential economic shifts.

Investment Strategy & Risk Management

In the current real estate market, strategic timing and opportunity identification are fundamental to maximizing investment returns. The market’s cyclical nature means that identifying the right moment to enter or exit positions can significantly affect profitability. With interest rates expected to stabilize over the next year, investors should focus on acquiring assets that can be repositioned or redeveloped to capture future appreciation. In the short term, opportunities lie in distressed properties where pricing has not yet fully recovered, allowing investors to acquire assets below replacement cost.

Market timing is particularly crucial for those engaged in fix-and-flip strategies. Given the potential for fluctuating materials costs and labor shortages, investors must execute projects swiftly and efficiently. Anticipating exit strategies and aligning them with market conditions will be critical. Holding costs should be meticulously calculated to ensure margins remain sufficient even if sales timelines extend unexpectedly. This is where Prime Property Funding’s fix-and-flip financing can offer competitive advantages by providing flexible terms to accommodate such uncertainties.

Risk factors in the current environment largely revolve around economic volatility, interest rate changes, and regional disparities in market recovery. Investors should adopt robust risk management strategies, including hedging against interest rate fluctuations and maintaining liquidity to withstand market downturns. Diversification across asset classes and geographies can also mitigate exposure to localized economic shifts. Additionally, maintaining a conservative underwriting approach with stress-tested assumptions will be vital to navigating potential market corrections.

Adjusting acquisition criteria and underwriting standards is essential in this dynamic environment. For buy-and-hold investors, focusing on properties with strong cap rates and potential for rent growth in regions with high employment and population growth is recommended. DSCR (Debt Service Coverage Ratio) cushions should be maintained at comfortable levels to ensure resilience against temporary income disruptions. For bridge financing, investors should prioritize assets that offer clear exit strategies and have contingency reserves in place to manage unforeseen expenses.

Key Considerations for Investors

- Analyze holding costs in fix-and-flip projects to ensure they do not erode profit margins; aim for a maximum holding cost of 10% of the total project budget.

- Target a minimum cap rate of 6% for new acquisitions in buy-and-hold strategies, adjusting based on market-specific risk factors.

- Incorporate a DSCR cushion of at least 1.25 in underwriting to safeguard against potential rental income fluctuations.

- Ensure that cash-on-cash returns exceed 8% annually to achieve competitive long-term investment performance.

- During bridge financing, align draw schedules with project milestones to optimize cash flow and minimize interest costs.

- Focus on markets with a strong risk-adjusted return profile, such as Southeast and Southwest regions, where demographic trends support sustained growth.

- Conduct stress tests on financial projections using scenarios with a 2-3% increase in interest rates and a 10% drop in market prices to ensure deal viability.

- Maintain a diverse portfolio with a balanced mix of asset classes and geographic spread to mitigate localized economic risks.

- Strengthen risk mitigation measures by setting aside reserves equivalent to three months of operating expenses and ensuring comprehensive insurance coverage.

- Prioritize tenant quality and property condition assessments to reduce vacancy rates and maintenance costs over the investment period.

By adhering to these strategies and recommendations, investors can navigate the current market landscape with confidence, ensuring robust returns while effectively managing risks.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.