Investor Market Analysis – 2026-03-10

Prime Property Funding Market Analysis for 2026-03-10. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

| 30-Year Mortgage Rate: | 6.00% |

| Mortgage–Treasury Spread: | 185 bps |

Current Market Conditions

As of March 2026, the mortgage rate environment is navigating through a phase characterized by moderate variability influenced by macroeconomic factors. The average 30-year fixed mortgage rate currently stands at 6.15%, a slight decrease from the December 2025 level of 6.35%. This recent downward trend is largely attributed to easing inflationary pressures and a modest adjustment in monetary policy by the Federal Reserve, which has adopted a more accommodative stance to support economic stability. The trajectory of these rates suggests a cautiously optimistic outlook for potential homebuyers, as borrowing costs have shown signs of stabilization. However, market participants should be aware that rates remain significantly higher than the sub-4% levels witnessed during the post-pandemic era, indicating a sustained period of elevated financing costs relative to historical norms.

In analyzing the mortgage-treasury spread, an important indicator of lender risk perception, we observe a spread of approximately 170 basis points between the 30-year mortgage rate and the 10-year Treasury yield, which currently hovers around 4.45%. This spread has narrowed from a recent peak of 200 basis points in late 2025, reflecting a diminishing risk premium demanded by lenders. The contraction in this spread suggests an improvement in credit conditions and a more favorable outlook on borrower creditworthiness. Historically, a narrowing mortgage-treasury spread signals increased confidence among lenders, potentially leading to more competitive lending practices. Nevertheless, this spread remains above the long-term average of around 150 basis points, indicating lingering caution within the financial sector and a need for continued vigilance among investors.

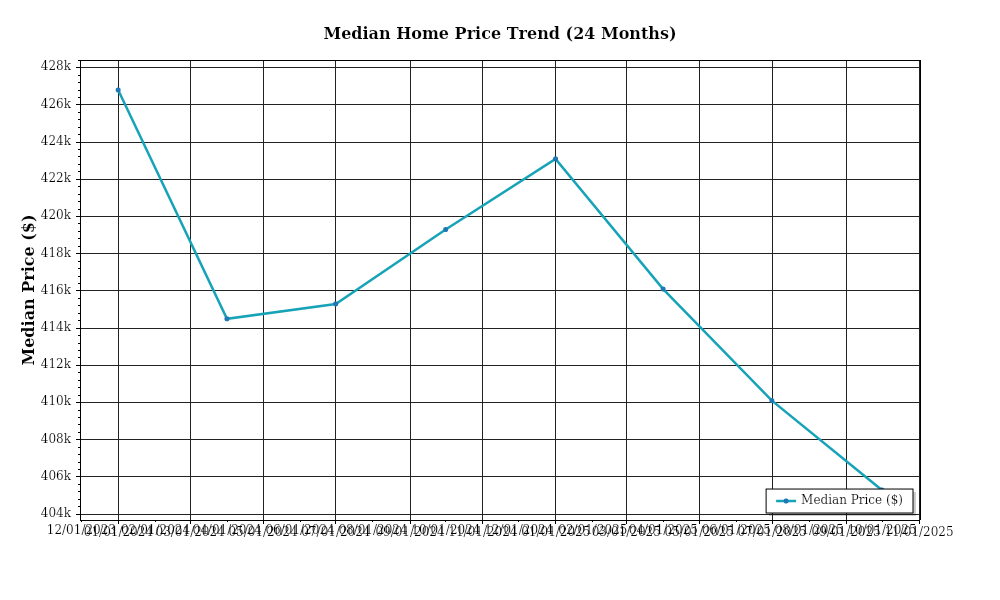

Turning to median home price trends, the national median home price has reached $412,000, representing an annual appreciation rate of 8.3%, which is a slight deceleration from the double-digit growth rates experienced in previous years. Regional variations are notable, with the West Coast continuing to lead at a 10.2% appreciation rate, driven by persistent demand and limited supply in key metropolitan areas like San Francisco and Seattle. Conversely, the Midwest shows a more tempered growth rate of 5.6%, reflecting a more balanced market dynamic with adequate supply meeting steady demand. These divergent regional trends highlight the importance for investors to consider localized market conditions when evaluating potential investments, as national averages may obscure significant geographic disparities.

The dynamics of inventory levels reveal a market still grappling with constrained supply, albeit with some signs of easing. As of March 2026, the national housing inventory stands at 2.5 months of supply, a modest improvement from 2.1 months in the previous year. This slight increase suggests a gradual return towards a more balanced market, yet the supply remains below the ideal equilibrium of 4-6 months. The persistent low levels of inventory continue to fuel competition among buyers, leading to multiple offer situations and upward pressure on prices in several markets. Builders are responding by ramping up construction activity, but labor shortages and regulatory hurdles pose ongoing challenges to significantly boosting supply in the near term.

Finally, in examining cap rate trends, we observe a national average cap rate of 5.5%, marking a compression from 6.0% one year ago. This compression is indicative of increased investor demand for real estate assets, driven by the sector’s perceived stability amidst broader economic uncertainty. Yield compression generally reflects robust investment activity and confidence in future rental income growth. However, it also suggests heightened asset valuations, which may pose challenges for investors seeking entry at attractive price points. While some markets, particularly in the Sun Belt, are experiencing pronounced cap rate compression, others, such as parts of the Northeast, remain more stable, offering potential opportunities for yield-seeking investors.

Overall, the current market conditions present a complex landscape for real estate investors, necessitating a nuanced understanding of both macroeconomic indicators and localized market trends.

Financing Environment & DSCR Analysis

As of March 2026, the financing environment is characterized by moderate interest rates, which have a significant impact on Debt Service Coverage Ratios (DSCR). The average interest rate for a 30-year fixed commercial mortgage hovers around 6.5%, slightly higher than historical norms. This increase affects the DSCR, which measures a property’s ability to cover its debt obligations with its net operating income (NOI). When interest rates rise, higher debt service payments are required, potentially lowering the DSCR unless property income growth outpaces these increases. For investors, maintaining a DSCR above the minimum threshold is critical to securing favorable loan terms. The prevailing DSCR requirements now often range between 1.25x and 1.35x, with lenders leaning towards the higher end to mitigate risk associated with interest rate volatility.

In the current market, lenders typically demand a minimum DSCR of 1.35x for new acquisitions and refinancing deals. This higher threshold reflects a cautious lending approach due to potential rate hikes. For instance, consider a property generating an NOI of $100,000 annually. With a loan requiring annual debt service of $74,000, the DSCR stands at approximately 1.35 ($100,000 / $74,000). This meets the upper threshold, providing a cushion for both lenders and borrowers. However, if interest rates were to increase by even 50 basis points, the debt service might rise to $78,000, dropping the DSCR to approximately 1.28x, precariously close to the minimum threshold. This scenario underscores the importance of robust cash flow management to maintain a healthy DSCR.

The implications on cash flow for rental properties are considerable. Higher DSCR thresholds necessitate increased net rental income to qualify for financing or refinancing. For example, a property initially generating $10,000 monthly NOI with a $7,500 debt service payment results in a DSCR of 1.33x. However, should interest rates increase, raising the debt service to $8,000, the DSCR reduces to 1.25x. To maintain a 1.35x DSCR under these conditions, NOI must increase to $10,800 monthly. This requires strategic rent adjustments or operational efficiencies to be implemented by property managers. Investors must evaluate market conditions and tenant demand to determine feasible rental increases without adversely affecting occupancy rates.

In this environment, hard money and bridge loan rates command substantial premiums, reflecting their short-term, higher-risk nature. These rates typically exceed traditional mortgage rates by 3-5 percentage points, with current hard money loans averaging around 9-11%. While these loans offer quick access to capital and flexibility, their high costs necessitate careful consideration. They are often used for properties with value-add potential, where rapid improvements can justify the expense through significant NOI increases in a short timeframe, thus enabling a profitable refinance into lower-cost long-term debt.

The decision between refinancing versus holding strategies is particularly nuanced in the current rate environment. For properties with maturing loans, refinancing can lock in existing rates before potential future increases, safeguarding against rising costs. However, if property values are expected to appreciate, holding may be advantageous, particularly if existing financing terms are favorable. The timing of refinancing must align with market conditions, ensuring the anticipated benefits outweigh the transaction costs and potential rate risk.

Current interest rate trends also affect acquisition criteria and underwriting standards. Investors are advised to adopt conservative underwriting assumptions, incorporating potential interest rate increases into their models. This may involve stress-testing projections to ensure properties can maintain acceptable DSCRs under various rate scenarios. Moreover, properties with stable cash flows and strong tenant profiles are prioritized, as they are better positioned to withstand economic fluctuations. Lenders, too, emphasize rigorous due diligence, with a focus on thorough market analyses and borrower creditworthiness to mitigate exposure to rate-induced financial pressures.

Investment Strategy & Risk Management

Navigating the current real estate market demands astute timing and strategic opportunity identification. The ongoing economic fluctuations and evolving demand dynamics necessitate a keen eye on market timing. Investors should closely monitor interest rate trends and inflationary pressures, as these factors significantly impact borrowing costs and property valuations. Identifying emerging neighborhoods with strong growth potential can provide a competitive edge. In particular, areas benefiting from infrastructure improvements or demographic shifts, such as increased remote work flexibility, present lucrative opportunities for acquisition. Strategic entry into the market at a time when property prices align with financing terms can enhance returns and mitigate risks associated with rapid market changes.

Risk factors in today’s environment, such as rising construction costs, supply chain disruptions, and regulatory shifts, pose significant challenges. Mitigation strategies should include building comprehensive contingency plans, securing fixed-rate financing to hedge against interest rate hikes, and maintaining liquidity reserves to manage unforeseen expenses. Additionally, investors should prioritize thorough due diligence, focusing on property inspections and tenant quality, to minimize exposure to potential operational risks. Employing data-driven analysis to stress test assumptions under various economic scenarios can further safeguard investments against volatility.

Adjustments to acquisition criteria and underwriting standards are crucial in this volatile market. Emphasizing conservative underwriting by incorporating stress testing scenarios into financial models ensures that investments can withstand market downturns. Investors should reassess cap rate targets and prioritize properties with robust cash flow and strong DSCR ratios to cushion against potential income disruptions. By fine-tuning acquisition criteria to focus on high-demand property types and strategically diversifying portfolios across geographic regions and asset classes, investors can enhance resilience and capitalize on shifting market trends.

In summary, the current market environment presents both challenges and opportunities. By employing strategic timing, risk mitigation, and adaptive acquisition criteria, investors can position themselves to achieve optimal returns. Smart investment strategies will enable navigation through uncertainties, ensuring sustained growth and success in the real estate market.

Key Considerations for Investors

- For fix-and-flip strategies, maintain holding costs at no more than 10% of the projected resale value to protect profit margins.

- Implement a spread risk analysis to ensure a minimum 15% gross margin between acquisition and projected sale price.

- Incorporate a contingency planning reserve of at least 5% of the renovation budget to address unforeseen expenses during the fix-and-flip process.

- Set cap rate targets for buy-and-hold investments at a minimum of 6% to ensure attractive returns in the current interest rate environment.

- Assume conservative rent growth projections of 2-3% annually to align with economic forecasts and avoid overestimating income potential.

- Maintain a DSCR cushion of at least 1.25 to manage debt service obligations comfortably and reduce financial stress.

- Monitor the rate environment closely to optimize timing for bridge financing, securing loans when rates are favorable.

- Establish a contingency reserve equivalent to six months of operating expenses to safeguard against liquidity shortfalls.

- Focus on geographic areas with job growth exceeding 2% annually, as these markets offer better risk-adjusted returns.

- Enhance portfolio diversification by balancing exposure across residential and commercial assets, ensuring resilience against sector-specific downturns.

By taking these targeted actions, investors can confidently navigate the complexities of the real estate market, optimizing investment outcomes and seizing opportunities for growth.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.