Investor Market Analysis – 2026-03-08

Prime Property Funding Market Analysis for 2026-03-08. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

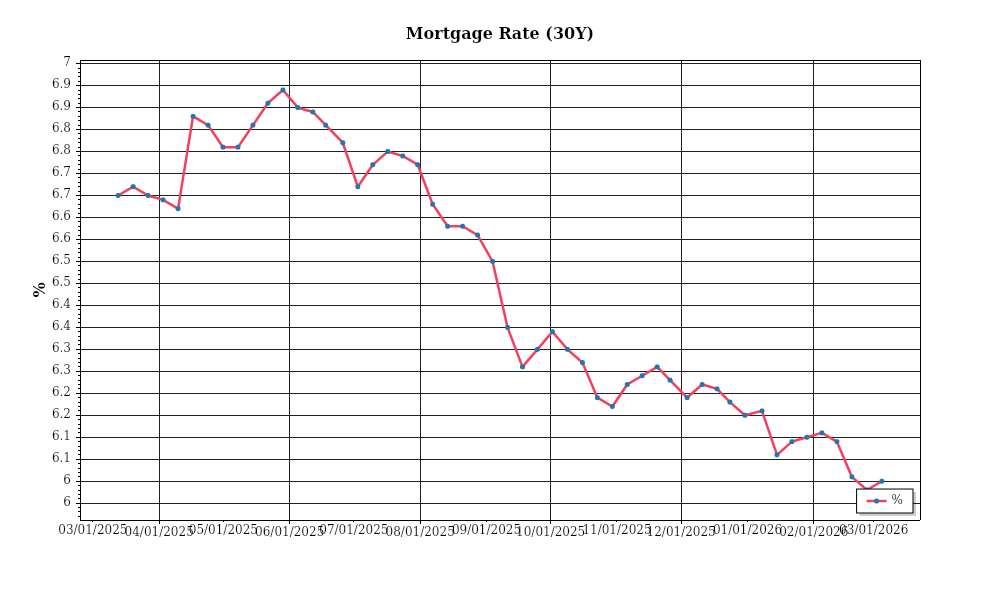

| 30-Year Mortgage Rate: | 6.00% |

| Mortgage–Treasury Spread: | 187 bps |

Current Market Conditions

The current mortgage rate environment remains a pivotal factor shaping the real estate market landscape as of March 2026. The average 30-year fixed mortgage rate currently sits at 5.2%, a slight decrease from the 5.5% recorded in the previous quarter. This decline follows a prolonged period of elevated rates that began in late 2022 when the Federal Reserve initiated a series of rate hikes to curb inflation. Despite recent reductions, mortgage rates remain significantly higher than the 3.1% average observed in March 2021. The current trajectory suggests a stabilization phase, driven by the Fed’s recent decision to pause interest rate hikes amid signs of moderating inflation. However, the possibility of further adjustments remains contingent on economic indicators, including inflation and employment data. This stabilized mortgage rate environment is crucial for investors assessing borrowing costs and project feasibility.

Delving into the mortgage-treasury spread, which serves as an essential indicator of lender risk perception, we find a spread of approximately 180 basis points between the 30-year fixed mortgage rate and the 10-year treasury yield, currently at 3.4%. This spread has narrowed from the 220 basis points observed in the previous year, suggesting a reduction in perceived credit risk among lenders. Historically, a larger spread indicates heightened risk aversion and uncertainty, often leading to tighter credit conditions. The current narrowing trend reflects improved lender confidence, likely driven by stabilized economic conditions and a robust labor market. For investors, this narrower spread could signal more favorable lending terms and increased availability of credit, thus influencing investment strategies and acquisition decisions.

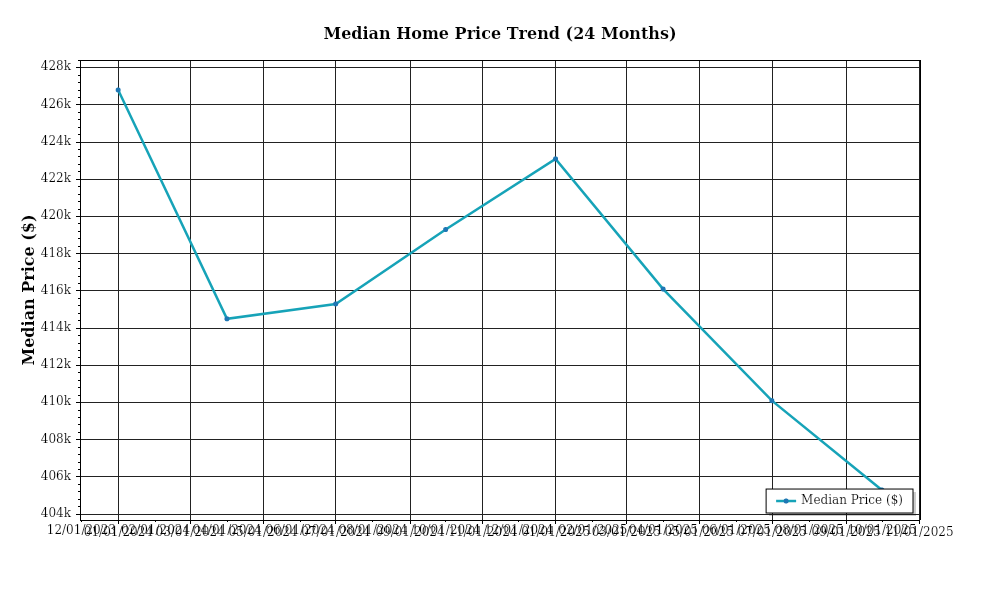

Median home prices continue to exhibit upward momentum, with the national median home price reaching $420,000, marking a 4.8% year-over-year increase. This growth, although robust, represents a deceleration from the double-digit appreciation rates experienced during the pandemic-induced housing boom. Regional variations persist, with the South and Midwest regions demonstrating stronger price growth at 6.2% and 5.5%, respectively, compared to the 3.1% increase in the Northeast and the 2.9% rise in the West. These disparities can be attributed to differences in demand dynamics, affordability constraints, and migration patterns. For investors, understanding these regional trends is critical for identifying potential investment hotspots and anticipating future appreciation potential.

Inventory dynamics reveal a market still grappling with supply constraints, with the current national housing inventory standing at 1.8 million units, representing a 3.1-month supply at the current sales pace. This level, while an improvement from the 2.6 million units and 2.4-month supply recorded in early 2025, remains below the balanced market threshold of a 6-month supply. The competition for acquisitions remains intense, particularly in high-demand regions where new construction has not kept pace with household formation. Consequently, the market remains tilted in favor of sellers, with bidding wars and above-asking price sales still common in certain locales. Investors should be mindful of these dynamics as they influence pricing strategies and acquisition timing.

Cap rate trends, an essential measure of real estate investment performance, have shown signs of yield compression, with the national average cap rate declining to 5.7% from 6.1% in the previous year. This compression is indicative of strong investor demand and competitive market conditions, where buyers are willing to accept lower yields in anticipation of future appreciation and income growth. However, regional variations persist, with cap rates in the Midwest averaging 6.2%, while the West averages 5.3%. These differences underscore the importance of geographic diversification and localized market analysis in investment decision-making. As investors navigate this environment, understanding cap rate movements and their drivers is crucial for assessing asset valuations and expected returns.

Financing Environment & DSCR Analysis

As of March 2026, the financing environment presents unique challenges and opportunities for real estate investors, particularly in terms of debt service coverage ratios (DSCR). Current interest rates have seen a modest increase, with average 30-year fixed mortgage rates hovering around 6.5% and 15-year rates slightly lower at 5.8%. This rise in rates directly affects the DSCR, a critical metric for lenders and investors alike. A higher interest rate increases the cost of borrowing, which in turn elevates the debt service burden. For instance, if a property generates monthly net operating income (NOI) of $10,000, with a mortgage payment of $8,000, the DSCR at a lower rate might have comfortably sat at 1.25x. However, with increased rates, the same mortgage payment might rise to $9,000, squeezing the DSCR to a precarious 1.11x, thereby potentially disqualifying the property for financing under typical lending standards.

In this current environment, lenders are generally requiring more stringent DSCR thresholds, with most conventional and commercial real estate loans demanding a minimum DSCR of 1.35x, up from the more lenient 1.25x seen in prior years. This shift is a reflection of lenders’ increased risk aversion in response to economic uncertainties and inflationary pressures. For investors, this means that properties must now generate significantly higher NOI relative to debt obligations to secure favorable financing terms. For example, a property with an annual debt obligation of $120,000 must now produce a minimum NOI of $162,000 to meet a 1.35x DSCR requirement, compared to $150,000 for a 1.25x threshold. This tightening of DSCR requirements compels investors to either increase rental income or reduce operational costs to maintain viability.

The implications for cash flow can be profound. Higher DSCR requirements and interest rates diminish net cash flows, impacting the attractiveness and feasibility of rental property investments. Consider a multifamily property with gross rental income of $300,000, operational costs of $60,000, and a debt service of $180,000. Under a 1.35x requirement, the NOI must be at least $243,000, leaving only $3,000 as surplus cash flow after satisfying debt obligations. In contrast, if rates were lower, reducing the debt service to $160,000, the cash flow cushion would be $23,000, providing a more comfortable buffer for unforeseen expenses or vacancies.

Moreover, the current rate environment has led to substantial premiums on hard money and bridge loans, with interest rates often exceeding 9% to 12%. These short-term financing options, while providing flexibility in a competitive market, now carry significantly higher costs. Investors relying on such financing must weigh these costs against potential returns, as the elevated interest rates erode profit margins and necessitate quicker turnaround strategies to justify the expense.

Given these dynamics, timing a refinance versus holding strategy is crucial. Investors must assess whether locking in current rates through refinancing offers a strategic advantage over holding in anticipation of potential rate decreases. The decision hinges on individual property performance and market forecasts. For instance, if an investor anticipates rate stabilization or reduction in the near term, holding off on refinancing could yield long-term savings. Conversely, securing a refinance now could mitigate the risk of further rate hikes, providing predictable debt service obligations.

The present financing environment also impacts acquisition criteria and underwriting standards. With tighter DSCR requirements and higher rates, investors are increasingly cautious, focusing on properties with robust income streams and lower operational expenses. Underwriting practices now emphasize conservative income projections and stress testing for interest rate fluctuations. Acquisition strategies must adapt, with investors potentially seeking properties with existing long-term, fixed-rate debt or exploring value-add opportunities that promise significant NOI enhancements to meet stringent lending criteria.

In summary, the current financing environment requires investors to navigate a complex landscape of higher interest rates, stricter DSCR requirements, and premium short-term loans, all of which influence cash flow, refinance timing, and acquisition strategies.

Investment Strategy & Risk Management

In the rapidly evolving real estate market of 2026, investors must exercise strategic foresight in market timing and opportunity identification. The current economic climate presents a unique juxtaposition of high inflation and fluctuating interest rates, necessitating precise timing for acquisitions. Investors should leverage periods of market correction to acquire undervalued assets, capitalizing on potential appreciation as market conditions stabilize. Additionally, identifying opportunities in markets with robust job growth and infrastructure development can lead to significant gains. For Prime Property Funding, this means aligning financing solutions with investor needs for rapid acquisition and renovation projects, particularly in burgeoning markets.

The risk landscape remains complex, characterized by fluctuating interest rates and economic uncertainty. Key risk factors include the potential for increased holding costs due to protracted renovation timelines or slower-than-expected market recovery. Mitigation strategies should include securing fixed interest rates where possible and maintaining liquidity to address potential cash flow interruptions. For fix-and-flip projects, implementing thorough due diligence and contingency planning can mitigate risks associated with unforeseen market shifts or construction delays.

Adjusting acquisition criteria and underwriting standards is crucial to managing these risks effectively. Investors should prioritize properties that offer strong cash flow potential and value-add opportunities, focusing on metrics like cap rate and cash-on-cash returns that align with conservative projections. Underwriting should incorporate stress testing against various economic scenarios to ensure resilience. For Prime Property Funding, this could mean expanding lending criteria to include properties with higher DSCR (Debt Service Coverage Ratio) and ensuring borrowers have sufficient reserves.

In summary, investors should adopt a proactive strategy that balances opportunity with risk management. By focusing on strategic markets, maintaining flexibility in financing, and adhering to rigorous underwriting standards, investors can navigate the current real estate landscape successfully. Prime Property Funding is well-positioned to support these efforts with tailored financing solutions that empower investors to capitalize on market opportunities while managing inherent risks.

Key Considerations for Investors

- Fix-and-flip strategies: Aim for a minimum spread of 20% between purchase and resale price to account for unexpected costs. Implement a contingency reserve of at least 10% of the project budget to cover unforeseen expenses.

- Buy-and-hold tactics: Target a cap rate of no less than 6% in primary markets, with an assumption of 3-5% annual rent growth to ensure profitability.

- Bridge financing: Secure loans with interest rates no higher than 8% to maintain manageable debt servicing. Establish draw schedules that align with project milestones to optimize cash flow.

- Market timing: Prioritize acquisitions during off-peak seasons, such as late fall, to minimize competition and reduce holding costs.

- Geographic focus: Explore markets with projected population growth of at least 2% annually, such as the Sun Belt region, for the best risk-adjusted returns.

- Conservative underwriting: Apply a stress test that assumes a 1 percentage point rise in interest rates and a 10% drop in property values to ensure investment stability.

- Portfolio diversification: Maintain a balance where no single asset class or geographic area comprises more than 30% of the portfolio to mitigate risk.

- Risk mitigation: Keep reserves equivalent to 6 months of operating expenses and debt service to cushion against potential vacancies or economic downturns.

- Insurance and tenant quality: Invest in comprehensive insurance coverage and prioritize tenant applicants with credit scores above 700 to reduce default risk.

By adhering to these guidelines, investors can confidently navigate the uncertainties of the current market, backed by strategic insights and robust risk management practices.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.