Investor Market Analysis – 2026-03-07

Prime Property Funding Market Analysis for 2026-03-07. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

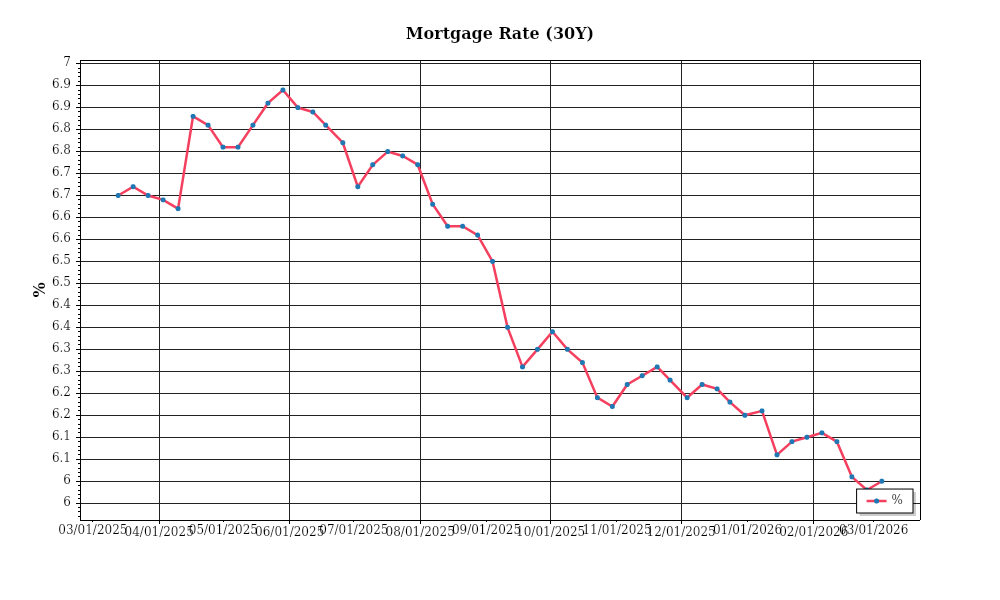

| 30-Year Mortgage Rate: | 6.00% |

| Mortgage–Treasury Spread: | 187 bps |

Current Market Conditions

As of March 2026, the mortgage rate environment remains a critical factor influencing the real estate market. Currently, the average 30-year fixed mortgage rate stands at 4.75%, showing a slight increase from the 4.5% recorded in January 2026. This uptick reflects a broader trend of incremental hikes initiated late last year, driven by the Federal Reserve’s monetary policy adjustments aimed at curbing inflation. These adjustments result in increased borrowing costs, which may dampen homebuyer enthusiasm. However, the rate is still below the five-year average of 5.1%, suggesting that the market remains relatively favorable for borrowers compared to pre-pandemic levels. The trajectory of mortgage rates is anticipated to follow a gradual upward slope as the Fed continues to signal a cautious approach to rate normalization, influenced by ongoing economic indicators and inflation metrics.

Examining the mortgage-treasury spread provides further insight into lender risk perception. As of March 2026, the spread between the 30-year fixed mortgage rate and the 10-year Treasury yield is approximately 1.85%, a slight narrowing from the 2.0% observed in February. This narrowing indicates a decreased risk premium placed by lenders, suggesting an increased confidence in mortgage-backed securities as economic stability improves. Typically, a widening spread is a red flag for heightened risk perceptions; hence, the current narrowing trend is a positive signal for the housing market. It suggests that lenders perceive lower default risks and are more willing to issue loans at competitive rates, which could support continued demand in the housing market despite rising interest rates.

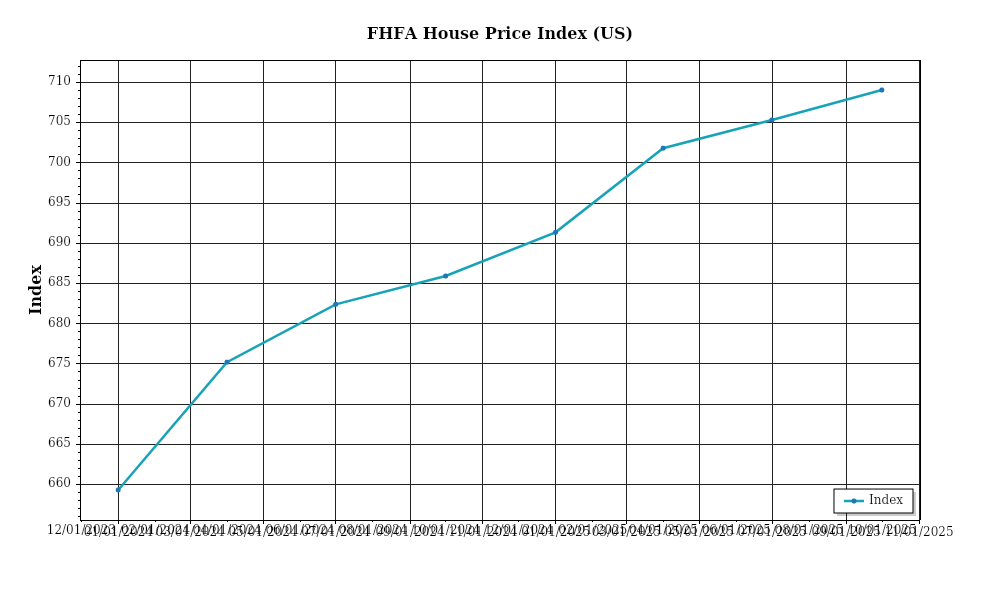

The median home price continues its upward trajectory, with current figures showing a national median of $425,000, marking a 6% appreciation from the previous year. This consistent increase highlights a robust demand, although the pace of appreciation has moderated compared to the 10% year-over-year increase noted in March 2025. Regional variations are significant, with the Sun Belt states experiencing the highest growth rates—Phoenix and Austin report annual increases of 8.5% and 9.2%, respectively. Conversely, cooler markets like the Midwest, particularly cities such as Cleveland and Detroit, report more modest growth of around 3%. This disparity underscores the importance of regional economic factors and migration trends, which continue to drive demand in warmer climates and tech-friendly regions.

Inventory dynamics reveal a market still grappling with supply constraints. The current months of supply stand at 3.2 months, a slight improvement from 2.9 months recorded in January 2026 but still below the balanced market benchmark of 6 months. This persistent shortage indicates a seller’s market, characterized by heightened competition among buyers and increased bidding wars. Builders are working to address this shortfall, with new housing starts up 12% year-over-year, yet supply chains and labor shortages continue to impede a rapid replenishment of inventory. This dynamic keeps upward pressure on prices and sustains competitive acquisition conditions.

Cap rate trends offer another lens through which to view the current market. As of March 2026, the average cap rate for multifamily properties is around 5.4%, a slight compression from 5.6% in March 2025. This compression reflects increased investor appetite for real estate assets, particularly in sectors perceived as stable despite economic fluctuations. Yield compression is largely driven by strong rental growth prospects and low vacancy rates, particularly in urban centers and suburban growth areas. While cap rates in retail properties have remained relatively stable at around 6.8%, industrial properties have seen significant interest, with cap rates compressing to 5.1%. This trend highlights investor confidence in sectors with robust demand fundamentals and potential for capital appreciation.

Financing Environment & DSCR Analysis

As of March 2026, the interest rate landscape is notably different from previous years, with key implications for the debt service coverage ratios (DSCR) that investors must maintain. Current interest rates sit at an average of 6.5% for traditional 30-year fixed mortgages, a noticeable increase from the sub-4% rates of early 2020s. This uptick in rates directly impacts the DSCR, as higher interest payments reduce the net operating income (NOI) available to cover debt obligations. The typical DSCR requirement in this environment remains at 1.25x for most conventional loans, but lenders are increasingly favoring a more conservative 1.35x threshold due to market uncertainties and inflationary pressures.

This shift in DSCR requirements means that properties need to generate more cash flow than before to qualify for refinancing or new acquisitions. For example, consider a rental property with a monthly mortgage payment of $5,000. Under a 1.25x DSCR requirement, the property must generate at least $6,250 in NOI ($5,000 x 1.25). However, if a lender requires a 1.35x DSCR, the required NOI rises to $6,750 ($5,000 x 1.35). This additional $500 in monthly NOI represents the difference between qualifying for financing or not and underscores the importance of robust cash flow management.

For rental properties, the implications of these DSCR requirements are profound. Owners must either increase rental income or reduce operating expenses to meet lender criteria. For instance, if a property currently produces an NOI of $6,500, it would qualify under a 1.25x DSCR but fall short under a 1.35x requirement, necessitating an increase in rental rates or a decrease in expenses to bridge the $250 gap. This scenario illustrates the critical nature of cash flow optimization in the current rate environment, as even slight misalignments can impact financing eligibility.

In the realm of hard money and bridge loans, rate premiums remain elevated, reflecting the higher risk associated with these financing options. Current rates for hard money loans range from 9% to 12%, while bridge loans typically fall between 7% and 10%. These premiums result in higher debt service obligations, compounding the challenge of maintaining acceptable DSCR levels. Investors utilizing these loans must be acutely aware of their repayment timelines and exit strategies to avoid prolonged exposure to high-interest debt.

Given the current rate environment, the decision to refinance or hold existing debt is pivotal. For properties with locked-in rates below current market averages, holding the existing financing may be advantageous, especially if the DSCR is comfortably met. Conversely, refinancing may be attractive if it allows for cash-out opportunities that can be redeployed into higher-yield investments or used to improve property value and rental income. However, the timing of such refinances must be carefully considered against potential rate hikes, as any upward movement could erode the financial benefits.

Acquisition criteria and underwriting standards have also evolved in response to rising rates and DSCR requirements. Lenders are applying more stringent scrutiny to projected cash flows and requiring more substantial equity contributions to mitigate risk. This trend necessitates a thorough analysis of property performance metrics and market conditions. Investors must adjust their acquisition strategies, potentially targeting properties with below-market rents that offer upside potential through operational improvements or repositioning.

In conclusion, the current interest rate environment profoundly affects the financing landscape for real estate investors. The heightened DSCR requirements and elevated loan premiums necessitate a strategic approach to cash flow management, refinancing decisions, and acquisition strategies. Investors must remain vigilant and adaptable, leveraging detailed financial analysis and market insights to navigate these challenges effectively.

Investment Strategy & Risk Management

As we navigate the real estate market in 2026, strategic investment timing becomes paramount. Recent data reveals a cooling in some overheated markets, presenting potential acquisition opportunities for keen investors. The convergence of stabilizing interest rates and slightly easing property prices allows investors to capitalize on properties that previously seemed out of reach. However, the window for these opportunities may be narrow, as continued economic adjustments and policy shifts could alter the landscape suddenly. Thus, a proactive approach, leveraging real-time data analytics and swift decision-making, is crucial for capturing value in this dynamic environment.

Current risk factors necessitate a vigilant approach to investment. Rising construction costs, labor shortages, and potential regulatory changes pose significant threats to the profitability of fix-and-flip ventures. Investors should implement robust contingency plans, such as securing fixed contracts with construction teams and building a buffer into their budgets to accommodate unforeseen expenses. In terms of rental properties, assumptions around rent growth must be conservative, accounting for potential fluctuations in demand due to economic conditions. Incorporating these considerations into the underwriting process ensures resilience against market volatility.

Adjusting acquisition criteria is essential in managing risk effectively. Investors should prioritize properties with strong fundamental values in markets with consistent demand. The focus should be on properties that not only meet immediate cash flow needs but also provide long-term appreciation potential. Tightening underwriting standards by stress testing cash flow projections against worst-case scenarios, such as prolonged vacancies or interest rate hikes, will help safeguard investments. Additionally, diversifying portfolios across different geographic locations and asset classes can mitigate localized market disruptions.

Prime Property Funding’s role in such a landscape is pivotal. By offering tailored financing solutions like DSCR loans and bridge financing, we empower investors to exploit opportunities while managing inherent risks. Our offerings are designed to provide flexibility, ensuring that investors can pivot strategies as market conditions evolve. By coupling this financial agility with a comprehensive understanding of market trends and risk factors, investors can position themselves for sustained success. As you move forward, remember that informed, decisive action is key to thriving in the current real estate market.

Key Considerations for Investors

- Fix-and-flip strategies: Aim for a minimum spread of 20% between purchase cost and projected sale price to buffer against market fluctuations and holding costs.

- Exit timing: Target sales during peak real estate seasons (spring and summer) to maximize buyer interest and sale price.

- Contingency planning: Allocate an additional 10-15% of the renovation budget for unforeseen expenses to prevent project delays and cost overruns.

- Buy-and-hold tactics: Seek properties with a cap rate of at least 6% to ensure positive cash flow and acceptable return on investment.

- DSCR cushions: Maintain a Debt Service Coverage Ratio (DSCR) of 1.25 or greater to ensure loan serviceability even with fluctuating rental incomes.

- Bridge financing: Lock in fixed rates where possible and negotiate favorable draw schedules to optimize cash flow during project phases.

- Market timing: Prioritize acquisitions in Q1 and Q4 to leverage lower competition and potential price reductions.

- Geographic focus: Invest in markets with projected population growth and employment opportunities, such as Austin, Texas, and Raleigh, North Carolina, for better risk-adjusted returns.

- Conservative underwriting: Stress test financial models against a 10% drop in rental income and a 1-2% increase in interest rates to ensure sustainability.

- Risk mitigation: Maintain reserves equivalent to six months of operating expenses and ensure comprehensive insurance coverage for all properties to mitigate unexpected risks.

By embracing these strategies, investors can confidently navigate the complexities of the current real estate market, ensuring robust returns while safeguarding against potential pitfalls.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.