Investor Market Analysis – 2026-03-05

Prime Property Funding Market Analysis for 2026-03-05. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

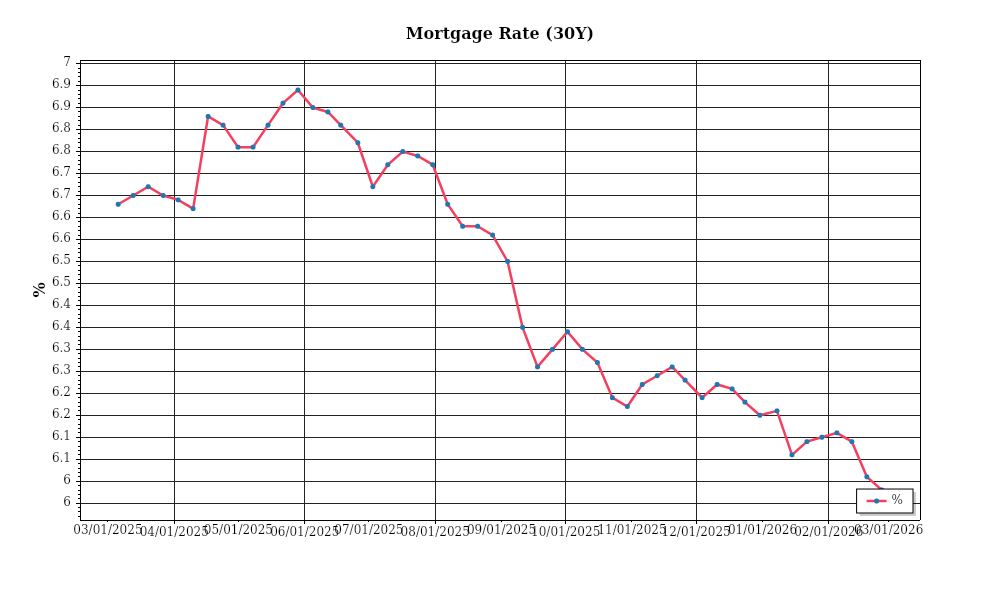

| 30-Year Mortgage Rate: | 5.98% |

| Mortgage–Treasury Spread: | 192 bps |

Current Market Conditions

As of March 2026, the mortgage rate environment continues to be a focal point for investors. The average 30-year fixed mortgage rate currently stands at 5.75%, a significant increase from the 3.25% level seen in early 2023. This rise reflects broader macroeconomic trends, including persistent inflationary pressures and subsequent rate hikes by the Federal Reserve. Over the last 12 months, there has been a steady upward trajectory, with rates climbing approximately 150 basis points. This increase has led to higher borrowing costs, which, in turn, are influencing buying power and demand in the housing market. Mortgage rates are expected to remain elevated throughout 2026 as the Federal Reserve maintains a cautious stance against inflation.

The mortgage-treasury spread, a critical indicator of lender risk perception, has widened significantly. Currently, the spread between the 30-year mortgage and the 10-year Treasury yield is approximately 200 basis points, compared to the historical average of 170 basis points. This widening suggests that lenders perceive increased risks in the housing market, possibly anticipating higher default rates or market volatility. The broader spread also indicates a more cautious lending environment, where lenders demand higher premiums to compensate for perceived risks. This environment could potentially constrain mortgage availability, further impacting homebuyers’ ability to finance new purchases.

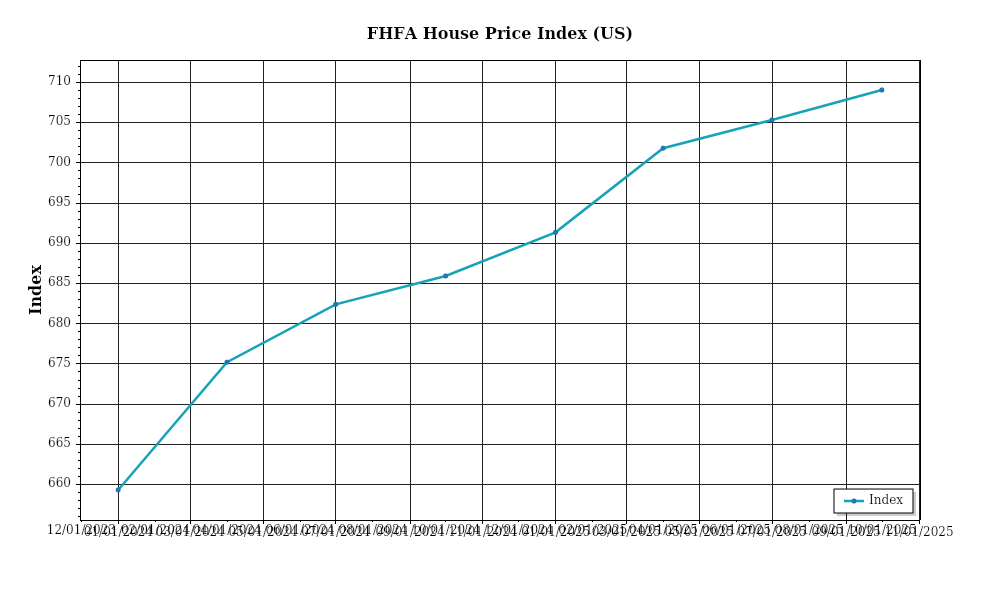

Median home prices continue to exhibit upward momentum, albeit at a moderated pace compared to the rapid appreciation seen in previous years. As of March 2026, the national median home price is approximately $420,000, reflecting a 5% year-over-year increase. This appreciation rate marks a slowdown from the double-digit increases witnessed during the pandemic years. Regional variations are notable, with markets such as the Northeast and West Coast experiencing slower growth rates due to higher base prices and affordability challenges. Conversely, areas in the Midwest and Southeast are still seeing robust appreciation, driven by relative affordability and ongoing migration trends.

Inventory levels remain a critical component of market dynamics, with current supply levels registering at 3.5 months of inventory, down from 4.2 months a year ago. This contraction highlights the ongoing supply-demand imbalance, where demand continues to outpace available housing stock. The competitive landscape for acquisitions remains intense, with many homes receiving multiple offers within days of listing. This heightened competition is exacerbated by limited new construction, as builders face challenges such as labor shortages and high material costs. The tight inventory conditions suggest that any significant market balance is unlikely in the near term, maintaining pressure on home prices.

Cap rate trends in the real estate market are also indicative of broader economic conditions. The average cap rate for multifamily properties currently hovers around 4.5%, reflecting a slight expansion from previous lows of 4.2%. This expansion signals a shift in investor sentiment, where the potential for higher returns is being weighed against increased economic uncertainty and rising interest rates. Yield compression, a hallmark of prior years driven by low interest rates and aggressive capital flows into real estate, appears to be reversing. This trend suggests that investors are recalibrating their expectations for risk and return, potentially leading to a more cautious investment approach in the coming months.

Overall, the current market conditions reflect a complex interplay of factors, including high mortgage rates, constrained inventory, and regional price variations, all set against a backdrop of changing economic expectations. These elements are reshaping the real estate landscape, influencing both current operations and future investment strategies.

Financing Environment & DSCR Analysis

As of March 2026, the financing environment remains a critical factor influencing real estate investment decisions, with interest rates hovering around 5.5% for 30-year fixed residential mortgages and approximately 6.75% for commercial loans. These rates directly impact the Debt Service Coverage Ratios (DSCR), a key metric for assessing a property’s ability to cover its debt obligations. Higher interest rates typically lead to increased monthly debt service payments, thereby pressuring DSCR calculations. For instance, a property with annual net operating income (NOI) of $120,000 and a debt service of $100,000 would have a DSCR of 1.2x. If interest rates increase and elevate the debt service to $110,000, the DSCR drops to 1.09x, potentially failing to meet standard lending requirements.

In the current environment, lenders are generally requiring a DSCR of at least 1.25x, although a more conservative 1.35x is often preferred, especially for riskier investments or properties with less predictable cash flows. This threshold acts as a buffer, ensuring that properties generate enough cash flow to cover debt obligations even when market conditions fluctuate. For a real estate investor, meeting a 1.35x DSCR on a property with an NOI of $135,000 would necessitate ensuring that the debt service does not exceed $100,000 annually. The increased requirement means that investors need to either find properties with higher NOI or negotiate lower purchase prices to maintain favorable DSCRs.

The cash flow implications for rental properties are substantial under these conditions. Take, for example, a multifamily property acquired at $1.5 million with a 75% loan-to-value (LTV) ratio, leading to a loan amount of $1.125 million. Assuming an interest rate of 6.75% on a 20-year amortization, the annual debt service would be approximately $99,000. To achieve a DSCR of 1.35x, the property must generate an NOI of at least $133,650 annually. If the property only yields $120,000 in NOI, the investor either needs to increase the income through rent hikes or find operational efficiencies to meet lender criteria.

The current rate environment also impacts hard money and bridge loan rate premiums, which tend to be higher than traditional financing options due to their short-term nature and associated risks. In March 2026, hard money loans are priced at rates between 8% to 12%, while bridge loans hover around 7.5% to 9%. These rates reflect their role in competitive, quick-turnaround investments or transitions where traditional financing is not feasible. Investors using these loans must factor in the higher cost of capital, which can significantly impact short-term cash flow and necessitate faster property improvements or sales to justify the premium.

Refinance timing and hold strategies are increasingly nuanced in this rate climate. Investors considering refinancing must balance the potential reduction in monthly payments against the costs of refinancing and the potential for rates to stabilize or decrease in the future. Holding strategies may be more advantageous if investors anticipate a favorable shift in rates or property values, allowing for refinancing under better terms. However, this requires a strong cash flow position to withstand interim financial pressures without compromising DSCR thresholds.

Lastly, the impact on acquisition criteria and underwriting standards is evident. Investors must exercise greater diligence in property selection, focusing on assets with strong income potential and lower operating costs. Underwriting standards are stricter, with emphasis on comprehensive market analysis, detailed cash flow projections, and contingency plans for interest rate fluctuations. This environment compels investors to adopt a more strategic approach, prioritizing properties with robust financials capable of sustaining higher debt service requirements over time.

Investment Strategy & Risk Management

In the current real estate environment, investors must employ a strategic approach to timing market entries and exits. The ongoing fluctuations in interest rates and shifting consumer preferences necessitate a keen awareness of economic indicators and market cycles. For investors in the fix-and-flip sector, identifying properties with potential for rapid appreciation and minimal renovation costs is crucial. Property acquisitions should be timed to capitalize on seasonal demand peaks, such as spring and summer, when buyer interest traditionally increases. This timing not only maximizes potential sale prices but also minimizes holding periods, reducing overall costs.

Risk factors are pronounced in the present market, with interest rate volatility and economic uncertainties posing significant challenges. Mitigation strategies should include stress-testing financial models to account for varying interest rate scenarios and maintaining a liquidity reserve to manage unexpected expenses or delays. Additionally, diversifying property locations can mitigate geographic-specific risks, while investing in areas with robust economic fundamentals can offer a hedge against broader market downturns.

Adjusting acquisition criteria and underwriting standards is imperative in this climate. Investors should adopt more conservative debt service coverage ratios (DSCRs) to ensure properties can withstand income disruptions. A focus on high-quality tenants and properties with strong cash flow potential remains crucial. Furthermore, incorporating broader economic forecasts into rental growth and cap rate assumptions will refine investment strategies, particularly for buy-and-hold portfolios aiming for stable, long-term returns.

Ultimately, strategic adjustments in acquisition strategies, risk management, and underwriting standards will empower investors to navigate the current market landscape effectively. By maintaining a vigilant and adaptive approach, investors can capitalize on emerging opportunities while safeguarding their portfolios against potential downturns.

Key Considerations for Investors

- Fix-and-flip strategies: Aim for a maximum holding period of 90 days to reduce carrying costs. Ensure a spread of at least 15% between acquisition and resale prices to cover costs and yield profit.

- Buy-and-hold tactics: Target properties with a minimum cap rate of 6% to ensure sufficient cash flow. Assume a conservative rent growth of 2% annually to buffer against economic fluctuations.

- Bridge financing: Prioritize projects with clear exit strategies within 12 to 18 months. Maintain a contingency reserve of at least 10% of the loan amount to cover unexpected costs.

- Market timing: Leverage seasonal demand trends by acquiring properties in Q4 and preparing them for the spring market, maximizing exposure and sale potential.

- Geographic focus: Consider investments in markets such as Austin, Texas, and Raleigh, North Carolina, which offer strong job growth and favorable demographic trends for risk-adjusted returns.

- Conservative underwriting: Stress-test for interest rate increases of up to 2% on current models to ensure continued profitability under adverse conditions.

- Portfolio diversification: Balance portfolios with a 60/40 split between residential and commercial properties to hedge against market-specific risks.

- Risk mitigation: Establish reserves equivalent to three months of operating expenses and implement comprehensive insurance coverage to safeguard against property damage and liability.

- Tenant quality: Prioritize leasing to tenants with credit scores above 650 and stable employment histories to reduce turnover and default risk.

- Property condition: Conduct thorough inspections and prioritize properties requiring less than 20% of acquisition cost in renovations to reduce initial expenditure and increase speed to market.

By adhering to these strategic considerations and actionable recommendations, investors can confidently navigate the real estate market, capitalizing on opportunities while managing risks effectively.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.