Investor Market Analysis – 2026-03-04

Prime Property Funding Market Analysis for 2026-03-04. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

| 30-Year Mortgage Rate: | 5.98% |

| Mortgage–Treasury Spread: | 193 bps |

Current Market Conditions

The current mortgage rate environment is characterized by a notable stabilization after a volatile period in late 2025. As of March 2026, the average 30-year fixed mortgage rate is approximately 6.25%, reflecting a slight decrease from the 6.5% observed in the previous quarter. This modest reduction can be attributed to the Federal Reserve’s recent pause in interest rate hikes and a slight improvement in inflation metrics. Over the past six months, mortgage rates have fluctuated within a narrow band, with rates typically ranging between 6.0% and 6.75%. The trajectory suggests a cautious optimism among lenders and borrowers, with the market anticipating a gradual easing of rates if inflation remains subdued and economic growth stabilizes. This environment presents a potential window of opportunity for both homebuyers and refinancers looking to lock in relatively favorable rates compared to the peaks seen in early 2025.

Analyzing the mortgage-treasury spread provides further insight into lender risk perception. The spread between the average 30-year fixed mortgage rate and the 10-year U.S. Treasury yield is currently at 2.15%, slightly above the historical average of around 1.8%. This elevated spread signals that lenders continue to price in a higher risk premium due to lingering economic uncertainties and geopolitical tensions. The current 10-year Treasury yield stands at 4.10%, reflecting a stable yet cautious outlook on long-term economic growth. The wider spread suggests lenders are maintaining a conservative stance, potentially due to concerns over borrower creditworthiness and potential defaults, despite recent improvements in employment figures and consumer sentiment.

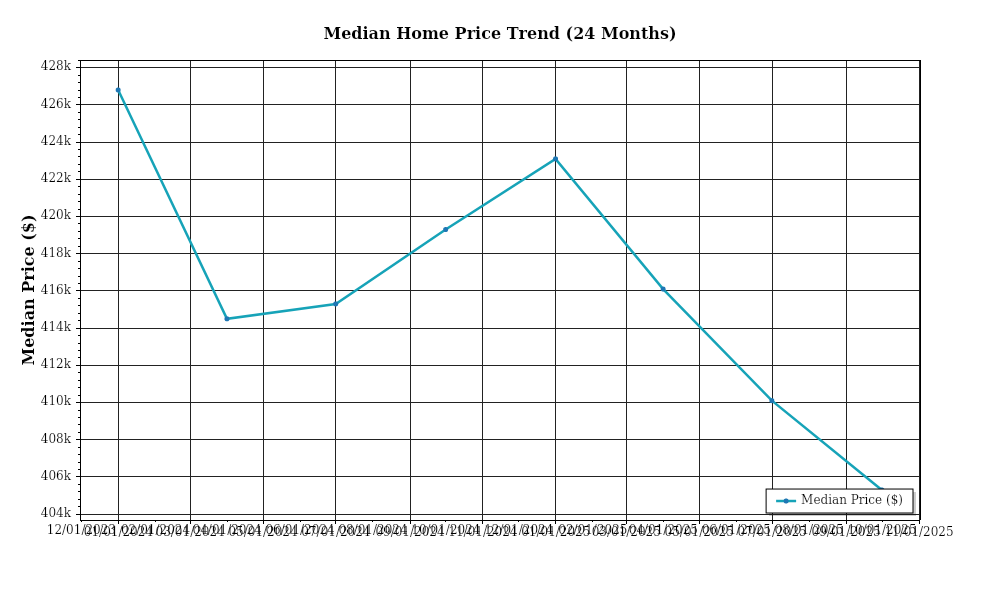

Median home price trends remain a focal point for market analysis. As of March 2026, the national median home price is approximately $425,000, representing a year-over-year appreciation rate of 5.8%. This growth rate marks a deceleration from the double-digit increases observed in 2024 and 2025, indicating a cooling yet still robust housing market. Regional variations are pronounced, with the Midwest experiencing the highest appreciation rates at 7.5%, driven by increased demand for affordable housing and a resurgence in manufacturing jobs. In contrast, the West Coast is seeing more moderate growth at 4.2%, as high prices and inventory constraints dampen buyer enthusiasm. These trends suggest a market gradually moving towards equilibrium, with regional disparities reflecting localized economic and demographic factors.

Inventory dynamics continue to influence market balance and competition. Nationally, the inventory of homes for sale has increased to 3.2 months of supply, up from 2.8 months a year ago, indicating a slight easing of the severe shortages seen in recent years. This increase is partly due to new construction projects coming to fruition and a modest uptick in existing homeowners deciding to sell. However, the market remains competitive, with well-priced homes often receiving multiple offers. The current inventory levels suggest a move towards a more balanced market, though certain metropolitan areas, particularly in the Sun Belt region, still exhibit signs of tight supply and heightened competition, driven by strong population growth and economic diversification.

Cap rate trends reveal ongoing dynamics in the commercial real estate sector. As of March 2026, national average cap rates for multifamily properties are approximately 5.5%, reflecting a slight compression from 5.7% the previous year. This compression indicates continued strong investor demand and an aggressive search for yield in the face of stabilized interest rates. Office and retail sectors show more varied cap rate movements, with office properties averaging 6.8% and retail at 6.5%. The relative stability in cap rates suggests a market adjusting to post-pandemic realities, with investors selectively pursuing opportunities in sectors deemed resilient to economic fluctuations. Yield compression in the multifamily sector underscores confidence in rental demand and long-term value retention, while the office sector’s stability reflects cautious optimism as remote work trends evolve.

In March 2026, the financing environment for real estate investments is notably shaped by the prevailing interest rates, which have a direct impact on the Debt Service Coverage Ratio (DSCR), a key metric that investors and lenders scrutinize closely. With the current interest rates hovering around 6.5% for conventional loans, the DSCR, which measures a property’s cash flow relative to its debt obligations, becomes critical. Higher interest rates lead to increased debt service costs, thus affecting the ability of rental properties to meet typical DSCR thresholds, which generally range between 1.25x and 1.35x.

A DSCR of 1.25x indicates that a property’s net operating income (NOI) is 25% greater than its debt obligations, while a DSCR of 1.35x suggests a more conservative buffer of 35%. In today’s market, lenders are increasingly favoring the 1.35x threshold due to economic uncertainty and the potential for interest rate hikes. This higher requirement means that properties must generate more income to qualify for financing, which can be challenging in markets experiencing rent stagnation or high vacancy rates. For investors, this necessitates a more rigorous evaluation of a property’s income potential and operating expenses to ensure adherence to these stricter DSCR standards.

The implications for cash flow are significant. Consider a rental property with an annual NOI of $120,000 and a loan requiring annual debt service of $100,000. This yields a DSCR of 1.20x, falling short of the 1.35x threshold. To meet the required DSCR, the property would need to either increase its NOI to $135,000 or reduce its debt service obligation, potentially through refinancing or adjusted loan terms. This scenario highlights the importance of strategically managing operating expenses and optimizing rental income to sustain cash flow and meet financing requirements.

In the realm of hard money and bridge loans, the interest rate premiums are notably higher in the current market, often ranging between 8.5% and 12%. These loans, typically short-term and used for property acquisition or renovation, come with increased costs that reflect the risk and urgency associated with their use. The elevated rates underscore the necessity for investors to have a clear exit strategy, ensuring that properties can either be refinanced under more favorable terms or sold within the loan’s term to avoid exorbitant interest payments.

The decision to refinance versus hold is nuanced in this economic climate. With rates expected to stabilize or potentially decrease in the medium term, some investors opt to hold off on refinancing, anticipating more favorable terms in the future. However, those with properties that currently meet or exceed a 1.35x DSCR may find it advantageous to refinance now, locking in rates before potential increases or capitalizing on improved loan terms. This strategy is particularly appealing for properties in high-demand areas with strong rental growth prospects.

Under this rate environment, acquisition criteria and underwriting standards are tightening. Lenders are placing greater emphasis on robust cash flow, conservative leverage, and thorough due diligence. Investors must be diligent in their property assessments, ensuring that acquisitions align with stringent DSCR requirements and that properties can sustain cash flow under various economic scenarios. This involves a detailed analysis of market trends, tenant demand, and potential expense increases, ensuring that properties not only meet current standards but also have resilience against future economic shifts.

In summary, the current financing environment presents both challenges and opportunities. By focusing on properties with strong income potential and maintaining rigorous underwriting standards, investors can navigate the complexities of DSCR requirements and interest rate impacts effectively, positioning themselves for long-term success in a dynamic market.

Investment Strategy & Risk Management

In the dynamic real estate market of 2026, investors must adopt a strategic approach to seize emerging opportunities while managing inherent risks. With fluctuating interest rates and evolving market dynamics, the timing of acquisitions becomes critical. Investors should be vigilant in identifying windows of opportunity, particularly in markets with rapid growth or emerging redevelopment zones. The current environment suggests a cautious approach, where thorough due diligence and market research guide investment decisions. Understanding local market cycles and seasonal trends can aid in optimizing entry and exit strategies, ensuring that investments align with periods of peak demand.

The present real estate climate presents several risk factors, including economic volatility and potential regulatory changes. To mitigate these risks, investors should diversify their portfolios both geographically and across asset classes. Establishing a buffer through contingency reserves and maintaining flexible exit strategies can safeguard against unforeseen disruptions. Moreover, stress testing financial models against various economic scenarios will aid in refining underwriting standards. This approach ensures that investment decisions remain robust even in less favorable market conditions, thereby preserving capital and enhancing returns.

Adjusting acquisition criteria in the current market is essential to balance potential returns with risk exposure. Investors might consider lowering leverage ratios to reduce financial risk, or focusing on properties with higher cash-on-cash returns to ensure liquidity. In fix-and-flip scenarios, prioritizing properties with lower acquisition costs and faster turnaround potential can minimize holding costs and exposure to market fluctuations. For buy-and-hold investors, targeting properties with strong cap rates and positive DSCRs will provide a cushion against rental market shifts.

In summary, real estate investors should focus on strategic market timing, thorough risk assessment, and adaptable acquisition criteria. By leveraging data-driven insights and maintaining a disciplined approach, investors can navigate the complexities of the current market while maximizing their investment potential. As the market continues to evolve, staying informed and agile will empower investors to capitalize on opportunities and mitigate risks effectively.

Key Considerations for Investors

- Implement fix-and-flip strategies that aim for a maximum hold period of six months to minimize holding costs and reduce spread risk.

- Ensure a contingency plan that includes a 10% reserve of the total project cost to manage unforeseen expenses in fix-and-flip projects.

- Set cap rate targets at a minimum of 6% for buy-and-hold investments to ensure attractive returns relative to market risk.

- Incorporate a DSCR cushion of at least 1.5x to safeguard against fluctuations in rental income or unexpected vacancies.

- Adjust bridge financing strategies by including a 2% rate buffer to account for potential interest rate hikes, ensuring project feasibility under varied conditions.

- Focus on markets with consistent rent growth assumptions of 3% annually to optimize long-term asset appreciation and income potential.

- Explore acquisition opportunities in secondary markets that offer superior risk-adjusted returns compared to overheated primary markets.

- Incorporate stress testing into underwriting processes to account for potential declines in property values of up to 15%.

- Maintain a portfolio diversification strategy that includes a balance of residential, commercial, and mixed-use assets across multiple geographic locations.

- Strengthen risk mitigation by ensuring properties have robust insurance coverage, high tenant quality standards, and regular maintenance schedules.

In this ever-evolving real estate landscape, adopting a proactive and informed investment strategy is paramount. By integrating robust risk management practices and dynamic acquisition criteria, investors can confidently navigate market challenges and capitalize on growth opportunities.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.