Investor Market Analysis – 2026-03-03

Prime Property Funding Market Analysis for 2026-03-03. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – March 2026

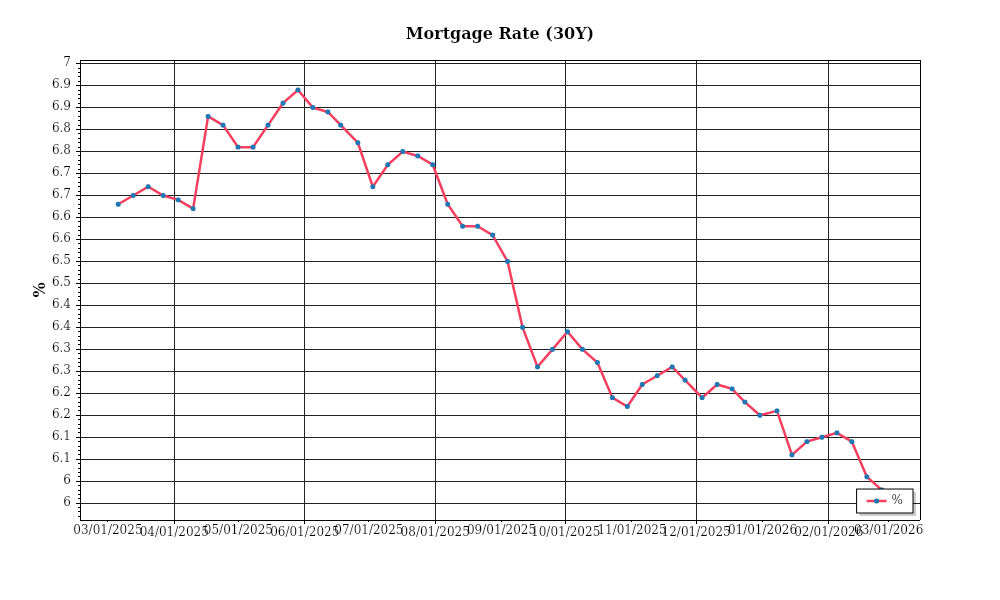

| 30-Year Mortgage Rate: | 5.98% |

| Mortgage–Treasury Spread: | 201 bps |

Current Market Conditions

As of March 2026, the mortgage rate environment remains a critical factor influencing real estate investment decisions. The current average mortgage rate for 30-year fixed loans stands at 6.25%, reflecting a slight increase from the 5.90% average observed in March 2025. This upward trend has been consistent over the past 12 months, driven primarily by the Federal Reserve’s incremental interest rate hikes aimed at combating inflationary pressures. The trajectory suggests a continued moderate rise in mortgage rates, with projections indicating potential stabilization around the 6.5% mark by mid-2026. For investors, these rising rates signal increased borrowing costs, potentially dampening demand for new acquisitions and affecting overall market liquidity. However, for those with existing fixed-rate financing, the impact remains neutral.

The mortgage-treasury spread, a key indicator of lender risk perception, currently hovers around 1.85%. This spread, calculated as the difference between the average mortgage rate and the 10-year Treasury yield, which is currently at 4.40%, reflects lenders’ risk assessment and willingness to extend credit. Over the past quarter, the spread has experienced a slight contraction from 2.00%, suggesting a marginal decrease in perceived lender risk. This contraction indicates a more favorable credit environment, with lenders possibly more optimistic about economic stability and borrower reliability. For investors, a tighter spread could imply more attractive financing conditions, although the absolute level of mortgage rates remains relatively high.

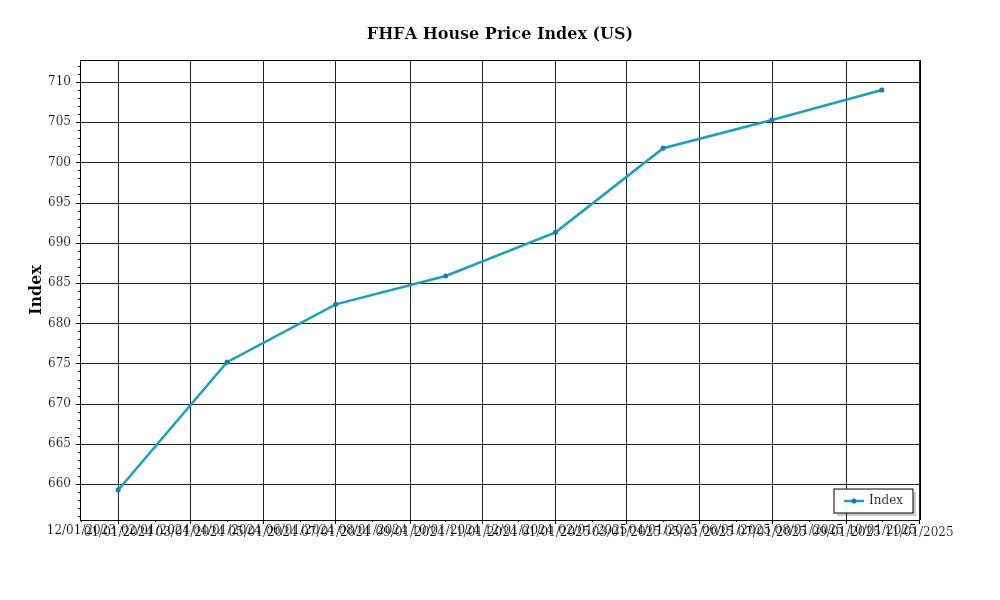

In terms of home price trends, the national median home price is currently at $425,000, representing a year-over-year appreciation rate of 4%. This growth rate marks a deceleration from the 6% year-over-year increase recorded in the previous period, indicating a cooling in the rapid price escalation seen over the past few years. Regional variations are notable, with the Midwest experiencing a modest 3% appreciation, while the Southern markets, buoyed by population inflows and job growth, still see higher rates around 5.5%. For investors, these regional disparities highlight the importance of market-specific strategies, as the slowing national appreciation may affect potential resale values and equity gains.

Inventory dynamics are another crucial aspect of the current market conditions. Nationwide, housing supply levels have moderated slightly, with the total inventory of homes for sale now standing at 1.8 million units, up from 1.6 million units a year ago. This increase corresponds to a months’ supply of 3.2 months, edging towards a more balanced market compared to the 2.8 months recorded last March. The competition for acquisitions remains robust, particularly in urban and suburban markets where demand pressures persist. This modest increase in supply is a positive sign for potential buyers, suggesting slightly reduced competition and potentially more negotiating power in transactions. However, the overall inventory remains below the six-month benchmark that typically signals a balanced market, indicating continued upward pressure on prices.

Finally, cap rate trends provide insights into the investment yield landscape. The average cap rate across major property types currently stands at 5.8%, reflecting a slight expansion from the 5.6% average recorded last year. This expansion can be attributed to the increasing interest rates, which have begun to compress yields, making property investments slightly less attractive relative to other asset classes. The expansion of cap rates indicates that property values are not appreciating at the same rate as rental incomes, leading to a potential re-evaluation of investment strategies. For investors, this suggests the necessity of recalibrating return expectations and possibly shifting focus towards value-add opportunities or markets with higher growth potential to maintain desired yield levels.

Financing Environment & DSCR Analysis

As of March 2026, the financing environment for real estate investments is characterized by relatively high interest rates, which have a significant impact on debt service coverage ratios (DSCR). Currently, interest rates have stabilized at around 6.5% for conventional commercial loans, which poses challenges for maintaining desirable DSCR levels. The DSCR is a critical metric used by lenders to assess a property’s ability to cover its debt obligations from its net operating income (NOI). Higher interest rates increase monthly debt service costs, thereby affecting the DSCR negatively. For instance, if a property generates a monthly NOI of $10,000, a loan at a 6.5% interest rate might require a debt service of around $8,000, yielding a DSCR of 1.25x. Such a scenario makes it challenging to meet more stringent lender requirements, particularly when some lenders demand a DSCR of 1.35x or higher.

In this environment, typical DSCR requirements fluctuate between 1.25x to 1.35x. Lenders have become more conservative, often requiring higher DSCRs to mitigate the increased risk associated with higher interest rates. For instance, a property needing to meet a 1.35x DSCR must have a NOI of $10,800 to support the same $8,000 monthly debt service. This places pressure on property owners to either increase rental income or reduce operating expenses to meet these thresholds. Properties unable to achieve a 1.35x DSCR may face higher interest rates or reduced loan amounts, which can hinder acquisition efforts and refinancing options.

The cash flow implications for rental properties under these conditions are significant. Higher debt service requirements reduce available cash flow, impacting the investor’s ability to reinvest profits or distribute income to stakeholders. For example, a property generating $120,000 annually with a debt service of $96,000 yields a cash flow of $24,000. However, if the DSCR requirement increases, necessitating a higher NOI, the owner might need to adjust rental rates or reduce operating costs to maintain profitability. In a competitive rental market, this could lead to increased tenant turnover if rent hikes are not aligned with market conditions, ultimately affecting cash flow stability.

The current market also sees a rise in hard money and bridge loan rates, with premiums over traditional financing reaching 2-3 percentage points higher. Investors seeking quick capital for acquisitions or renovations might face rates ranging from 8.5% to 9.5%. These elevated rates further stress cash flows and can significantly affect short-term investment returns. Investors must weigh the higher cost of capital against the potential for value-add improvements and expedited project timelines. In many cases, the increased cost of hard money loans requires a clear, profitable exit strategy to justify their use.

Given the rate environment, refinance timing versus hold strategies is a critical consideration for investors. Refinancing can lock in current rates and improve cash flow if it results in a lower interest rate or extended terms. However, with rates likely to remain elevated in the short term, refinancing decisions require careful analysis of future rate trends and property income potential. Conversely, a hold strategy allows investors to wait for more favorable rate conditions, albeit with the risk of market fluctuations impacting property values and rental income. Investors must balance the immediate benefits of refinancing with the potential for improved financial conditions in the future.

Finally, the current interest rate climate influences acquisition criteria and underwriting standards. Investors must adapt by tightening their criteria, focusing on properties that can achieve higher NOI, or are in markets with strong rental demand and low vacancy rates. Underwriting standards have also tightened, with lenders scrutinizing income stability, tenant quality, and market conditions more closely. This environment necessitates a thorough due diligence process, ensuring that properties can not only meet current DSCR requirements but also withstand potential economic shifts. As such, investment strategies must be rooted in realistic projections and a comprehensive understanding of market dynamics.

Investment Strategy & Risk Management

In the current real estate climate of March 2026, strategic market timing and opportunity identification are pivotal for investors aiming to maximize returns while minimizing risks. The real estate market is showing signs of stabilization after a period of volatility, making it crucial to identify sub-markets and property types that promise the best risk-adjusted returns. As interest rates remain moderately elevated, identifying properties that can be acquired at a discount due to market conditions or distressed situations presents a lucrative opportunity. Investors should focus on properties with a strong potential for appreciation and those that can sustain high occupancy levels, especially in well-performing neighborhoods with robust economic indicators.

Risk factors in the current environment include potential interest rate hikes, fluctuating construction costs, and evolving tenant preferences. To mitigate these risks, investors should adopt a conservative approach, focusing on properties with strong cash flows and resilience against economic downturns. Stress testing against various economic scenarios can ensure that properties remain viable investments even under adverse conditions. Additionally, diversifying across different asset classes and geographic locations can help in spreading risk and tapping into multiple growth markets.

Adjusting acquisition criteria and underwriting standards is essential in this environment. Investors need to be cautious about over-leveraging and ensure that properties meet stricter debt service coverage ratios (DSCR) and cap rate thresholds. A focus on cash-on-cash returns and ensuring a healthy cushion over mortgage obligations will safeguard against potential market downturns. Given the unpredictability of market conditions, incorporating flexible exit strategies and maintaining contingency reserves are prudent approaches.

Prime Property Funding can leverage its expertise in hard money loans and DSCR loans to support investors in this environment. By offering competitive rates and terms, especially for fix-and-flip and buy-and-hold strategies, the firm can help clients capitalize on emerging opportunities while effectively managing risks. The emphasis should be on conservative lending practices, ensuring sound underwriting standards that align with the current market dynamics.

Key Considerations for Investors

- Implement fix-and-flip strategies with a focus on minimizing holding costs by targeting properties that require low to moderate renovations, ensuring faster turnaround.

- Maintain a spread risk threshold of at least 20% between acquisition cost and sale price to buffer against market fluctuations.

- Factor in a contingency plan for exit timing by allowing an additional 3-6 months beyond expected timelines to account for market delays.

- For buy-and-hold investments, aim for a minimum cap rate of 6% and ensure rent growth assumptions do not exceed 3% per annum to remain conservative.

- Maintain a DSCR cushion of at least 1.25 to provide a safety net against potential rent fluctuations or increased operating expenses.

- Adapt bridge financing strategies by assessing current rate environments and securing fixed rates where possible to mitigate interest rate volatility.

- Ensure draw schedules are aligned with construction milestones to optimize cash flow management during renovations.

- Identify geographic markets such as secondary cities with high growth potential and favorable economic indicators for best risk-adjusted returns.

- Develop a conservative underwriting approach by stress-testing rent and expense assumptions under various economic scenarios to ensure robustness.

- Enhance portfolio diversification by balancing investments across asset classes, such as residential and commercial, and spreading geographic exposure to mitigate localized risks.

By embracing these strategies and maintaining a vigilant approach, investors can navigate the current market landscape with confidence, ensuring resilience and profitability in their real estate endeavors.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.