Investor Market Analysis – 2026-02-27

Prime Property Funding Market Analysis for 2026-02-27. Current market conditions analyzed through the lens of financing costs, inventory dynamics, and return potential.

📊 Investor Snapshot – February 2026

| 30-Year Mortgage Rate: | 5.98% |

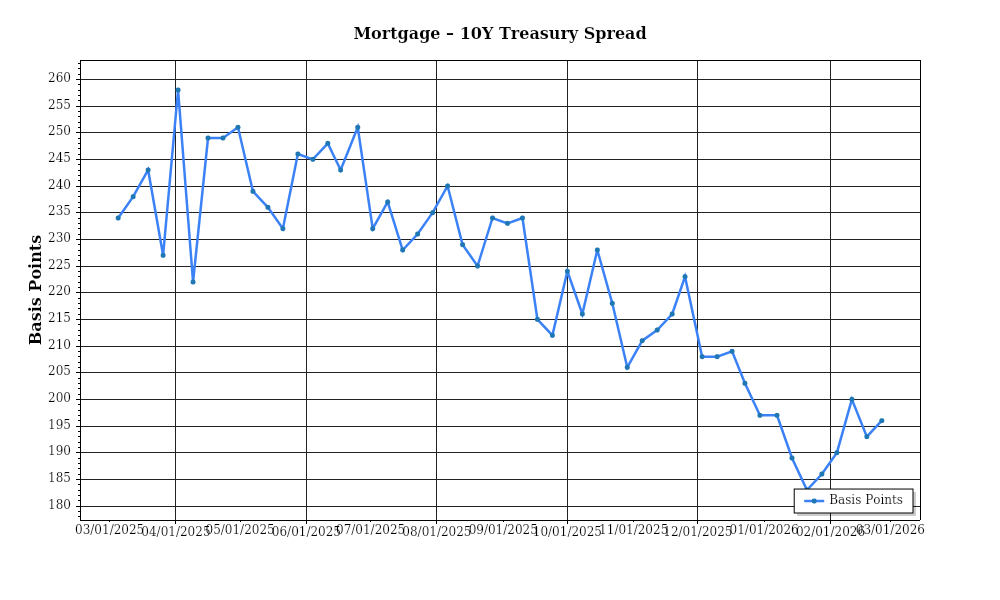

| Mortgage–Treasury Spread: | 196 bps |

Current Market Conditions

The mortgage rate environment as of February 2026 remains characterized by a cautious stability following a period of volatility in the previous year. The average 30-year fixed mortgage rate is currently at 6.15%, showing a slight decrease from the 6.35% seen in December 2025. This decline marks a stabilization phase after rates peaked at 6.75% in mid-2025. The Federal Reserve’s decision to maintain the federal funds rate at 4.75% has contributed to this moderation, following a series of aggressive hikes intended to curb inflation. The trajectory for mortgage rates in 2026 suggests a plateau, as market sentiment and Fed policy signals indicate a pause in rate adjustments barring unexpected economic changes. This stability offers potential buyers and investors a more predictable environment for financial planning and decision-making.

The mortgage-treasury spread, a critical measure of lender risk perception, currently stands at 1.75%, slightly above the historical average of 1.50%. This spread, calculated as the difference between the mortgage rate and the 10-year Treasury yield, which is now 4.40%, has been influenced by continued concerns over economic stability and borrower creditworthiness. The elevated spread suggests that lenders are pricing in additional risk, reflecting uncertainties such as geopolitical tensions and potential economic slowdowns. In practical terms, this means that while mortgage rates have stabilized, lenders are cautiously guarding against defaults by maintaining a higher risk premium. Investors should note that this environment may lead to tighter lending standards and selective credit issuance.

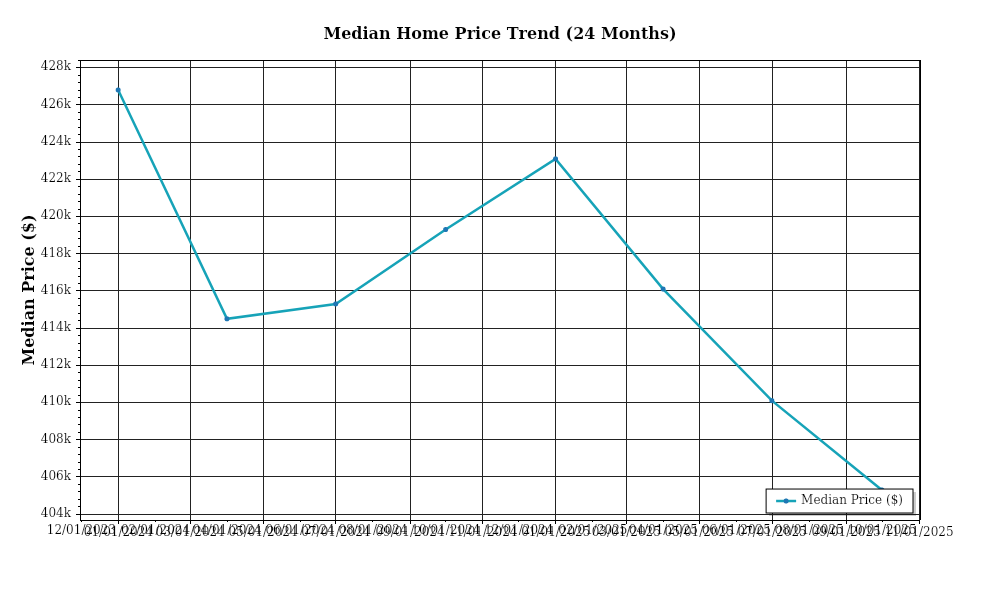

Median home prices continue to exhibit upward momentum, with the national median price now at $410,000, representing a year-over-year increase of 7.5%3-4%, has moderated from the double-digit growth observed in 2024 and early 2025. Regional variations remain significant, with the South and West experiencing the highest gains, at 9.2% and 8.6% respectively, driven by robust economic activity and population growth. Conversely, the Midwest shows more modest increases of 4.3%, reflecting its more balanced supply-demand dynamics. For investors, these trends suggest continued opportunities for capital gains, especially in high-growth areas, though with a caveat of increased entry costs.

Inventory dynamics reveal persistent supply constraints, with nationwide housing inventory levels at approximately 2.1 months of supply, well below the balanced market threshold of 6 months. This tight supply is perpetuated by factors such as labor shortages in construction and zoning restrictions that limit new developments. The competition for acquisitions remains fierce, particularly in metropolitan areas where demand outstrips supply. This imbalance continues to fuel price growth and bidding wars, making it challenging for new entrants to secure properties at favorable prices. However, for existing property holders, this environment supports continued value appreciation and potential for rental income growth.

Cap rate trends have shown a slight expansion recently, with average cap rates for multifamily properties rising to 5.3% from 5.1% in mid-2025. This expansion indicates a mild easing of yield compression that was prevalent over the past few years, driven by rising interest rates and investor demand for higher returns. The current cap rate environment reflects a recalibration, where investors are adjusting expectations amid a more stabilized interest rate context and ongoing economic uncertainties. For real estate investors, this suggests potential opportunities to acquire properties at more attractive yields, though it also signals heightened scrutiny on asset performance and location-specific fundamentals.

In summary, the current market conditions present a complex interplay of stabilizing mortgage rates, cautious lender risk assessments, dynamic median price growth with regional disparities, constrained inventory levels, and evolving cap rate trends. These factors collectively shape a real estate landscape that demands strategic navigation and astute decision-making for investors looking to optimize returns in 2026.

Financing Environment & DSCR Analysis

In February 2026, the lending landscape is heavily influenced by the current interest rate environment, which is characterized by relatively high levels compared to recent historical standards. This scenario has a significant impact on the Debt Service Coverage Ratio (DSCR), a critical measure used by lenders to determine the viability of financing rental properties. With average interest rates for commercial real estate loans hovering around 6% to 7%, borrowers face heightened debt service obligations. This increase in debt servicing costs directly affects the DSCR, as the need to maintain or improve this ratio becomes more challenging. Investors must ensure that their rental properties generate enough net operating income (NOI) to cover these increased costs. In this environment, maintaining a DSCR of at least 1.25x is becoming the new norm, while more conservative lenders might require ratios closer to 1.35x for additional security.

The typical DSCR requirement of 1.25x means that a property’s NOI must be at least 25% greater than its debt obligations. In practical terms, for a property with annual debt service payments of $100,000, the property must generate at least $125,000 in NOI to meet these requirements. In contrast, a 1.35x DSCR requirement would necessitate $135,000 in NOI for the same debt service. This increase in DSCR requirements is a direct response to the increased risk associated with higher interest rates. As a result, investors need to be more diligent in projecting rental income, controlling expenses, and implementing rent increases to enhance cash flow.

The cash flow implications for rental properties under the current interest rate environment can be profound. For example, consider a multifamily property with an NOI of $200,000 and a current loan requiring annual payments of $150,000. With a DSCR of 1.33x, the property is comfortably above the 1.25x threshold. However, if refinancing or acquisition is considered under the new interest rate conditions, debt service could potentially increase by 15%, raising annual payments to $172,500. This would lower the DSCR to 1.16x, below the acceptable threshold, necessitating either a reduction in loan amount or an increase in NOI through rent adjustments or operational efficiencies.

In the current market, hard money and bridge loan rates carry significant premiums due to their short-term nature and higher risk profiles. Rates for these types of loans can range from 8% to 12%, substantially above traditional loan rates. These premiums make hard money loans a less attractive option for long-term holds, but they remain a viable solution for investors aiming to quickly reposition or renovate properties to increase value and stabilize cash flows before transitioning to more favorable long-term financing.

Given the current rate environment, the decision to refinance versus holding existing debt becomes increasingly complex. Investors must carefully analyze the potential for interest rate reductions in the near term against the certainty of current higher rates. If rates are expected to decline, holding existing debt with lower interest rates might be preferable. Conversely, if rates are anticipated to rise further, refinancing now to lock in existing rates, despite being higher than historical averages, might be prudent to avoid future increases.

The impact of these dynamics on acquisition criteria and underwriting standards is significant. Lenders are adopting more stringent underwriting standards, focusing on properties with stable cash flows and demonstrating robust tenant demand. Acquisition criteria are also evolving, with investors prioritizing properties that offer potential for rent increases or operational improvements to enhance cash flow and meet stricter DSCR requirements. This environment necessitates a more cautious approach to acquisitions, emphasizing thorough due diligence and robust financial projections to ensure compliance with lender requirements and safeguard investments against potential interest rate volatility.

Investment Strategy & Risk Management

In the current real estate market, characterized by rising interest rates and volatile economic conditions, effective market timing and opportunity identification are paramount for successful investment. Investors need to be vigilant and strategic, leveraging data-driven insights to navigate the complexities of the market. Identifying opportunities in emerging markets or distressed properties can yield substantial returns, especially when paired with a strong exit strategy. Timing acquisitions to coincide with market dips or seasonal slowdowns can also provide cost advantages, while maintaining flexibility to capitalize on unforeseen opportunities is crucial.

Risk factors in the current environment include fluctuating interest rates, potential economic downturns, and varying regional real estate trends. To mitigate these risks, investors should employ robust stress-testing models that account for interest rate hikes and economic contractions. Diversifying portfolios to include a mix of asset classes and geographic locations can also buffer against localized downturns. Additionally, maintaining liquidity through contingency reserves and securing favorable loan terms, such as fixed-rate financing, can protect against financial instability.

Adjusting acquisition criteria and underwriting standards is essential in managing risk and ensuring profitability. Investors should focus on properties with higher cap rates to offset increased financing costs, and prioritize markets with strong, sustained rental demand. Underwriting should incorporate conservative assumptions, such as lower rent growth projections and higher vacancy rates, to account for potential market fluctuations. Emphasizing properties with strong cash-on-cash return potential ensures resilient income streams, even in uncertain times.

Overall, investors must maintain a proactive approach, continuously monitoring market conditions and adjusting strategies accordingly. By embracing a disciplined investment strategy and implementing robust risk management practices, investors can navigate the current market landscape with confidence, positioning themselves for long-term success.

Key Considerations for Investors

- Fix-and-flip strategies: Target properties with a minimum potential spread of 25% to account for unexpected costs and market shifts. Incorporate a contingency planning buffer of at least 10% of total project costs to manage unforeseen expenses.

- Buy-and-hold tactics: Aim for a cap rate of at least 6% to ensure viable returns in the face of rising interest rates. Use conservative rent growth assumptions of no more than 3% annually to account for economic fluctuations.

- Bridge financing: Opt for draw schedules that align with project milestones, minimizing interest accrual. Establish contingency reserves equal to 6 months of debt service to safeguard against delays or market downturns.

- Market timing: Prioritize acquisitions during the off-peak season when competition and prices may be lower, but ensure holding costs do not exceed 5% of the property’s projected value to maintain profitability.

- Geographic focus: Concentrate on markets with a projected 5-year rent growth of at least 4% and stable employment sectors to ensure the best risk-adjusted returns.

- Conservative underwriting: Stress test DSCR scenarios at 1.2x to accommodate potential interest rate increases and vacancy spikes.

- Portfolio diversification: Maintain a balanced mix of 60% residential and 40% commercial properties to optimize risk and return profiles.

- Risk mitigation: Keep reserves equivalent to 3 months of operating expenses and prioritize properties with high-quality tenants and minimal deferred maintenance to reduce risk exposure.

By adhering to these strategic recommendations and maintaining a vigilant approach to market dynamics, investors can confidently navigate the current real estate landscape and capitalize on emerging opportunities.

Resources

External References

Disclaimer: This market analysis is for informational purposes only and should not be considered financial or investment advice. Market conditions can change rapidly. Consult with a qualified financial or lending professional before making any decisions.